United States CPI (Consumer Price Index)

In September, the US CPI rose by 3.7%, higher than the expected 3.6%. The core CPI rebounded, increasing by 4.1% year-on-year, lower than the previous value of 4.3%, both in line with expectations. Rent is a major factor in the inflation rise. After the September data was released, the CME Fed Watch tool showed that the probability of a rate hike in November is less than 5%, and the possibility of a December rate hike has risen to double digits. The market’s expectations on the Fed’s rate hike may be based on several considerations:

- The international situation in October and November is more complex, and international oil prices may be unpredictable under the Israel-Palestine conflict.

- US two-year and ten-year bond yields have put constraints on the economy after a round of increases. If the rate hike stops in November but retains the long-term expectation of a December hike, the yield curve can still be controlled, further limiting economic expansion.

- Global capital markets are in a plateau period. From the speeches of Fed officials, they also don’t want to see a significant decline in the US capital market, causing unnecessary risks. Overall, this CPI data is not as good as expected. However, as mentioned earlier, once the CPI falls below 4%, the decline process is very slow. This indicates that the US economy has indeed entered a hovering stage before landing, where various factors may alternately disturb investors’ nerves. Currently, the global capital market is in a plateau phase, fluctuating within a narrow range. The relatively high risk-free yield in the US has indeed imposed constraints on the economy. After this CPI report was released, the variables in the global capital market trajectory are still determined by crude oil prices. Whether the Israel-Palestine conflict will lead to a surge in oil prices due to risk spillover is a risk factor. If this risk is effectively controlled in the next 2-3 weeks, the global capital market may stabilize.

In addition, the US CPI has indeed entered a plateau phase. Although its core CPI is gradually declining, it remains high. It is difficult to determine whether the core CPI can successfully fall back to 2%, especially with strikes in the US automotive and healthcare industries leading to a new round of wage and price increases. But overall, the US economy still maintains a very strong demand-side expansion, which fundamentally supports the global capital market.

Next, focus on the trends of the US dollar and gold. Currently, the gold market seems to show an upward trend, suggesting uncertainty about its future price trajectory. Gold can be considered a risk-free alternative to the US currency. Although gold prices fluctuate, they are relatively small compared to the stock market. For global asset allocation, after money flows into US currency, the remaining funds flow into gold, showing strength, leading to situations where both the dollar and gold rise.

China

China released monetary and price data this week, among which, the stock of social financing remained flat year-on-year, M2 grew by 10.3% year-on-year, down 0.3% from last month, and CPI remained flat, maintaining 0.1%. This data report reflects the prominent feature of the economic cycle – transitioning from a decline to stabilization. As for how long the bottom will last, the biggest uncertainty is still the liquidity issue of the real estate market. However, this price and money report is not bad news for China’s capital market. Clearly, the Chinese economy is in a phase of struggling against deflation. According to China’s unique economic-political cycle, it’s mid-October now. If major reform policies are postponed due to economic conditions and the third plenary session is delayed, the most important upcoming event will be the Central Economic Work Conference in mid to late December. In the next two months, the economy should be in the phase of continued implementation of previous policies and may not see major increases. Furthermore, there are no major holidays in the next two months, and considering external rate hike situations, the capital market might be in a challenging period.

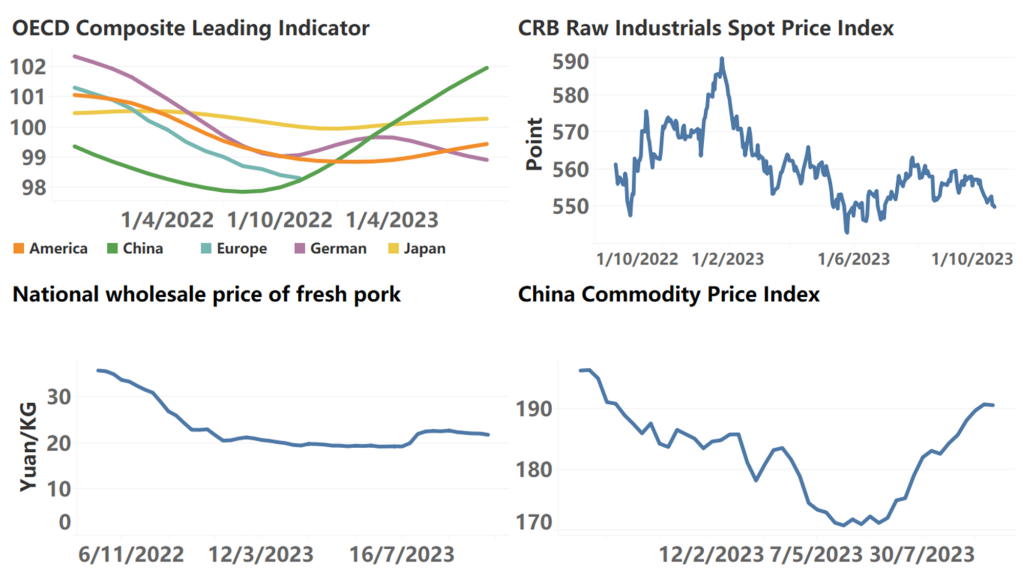

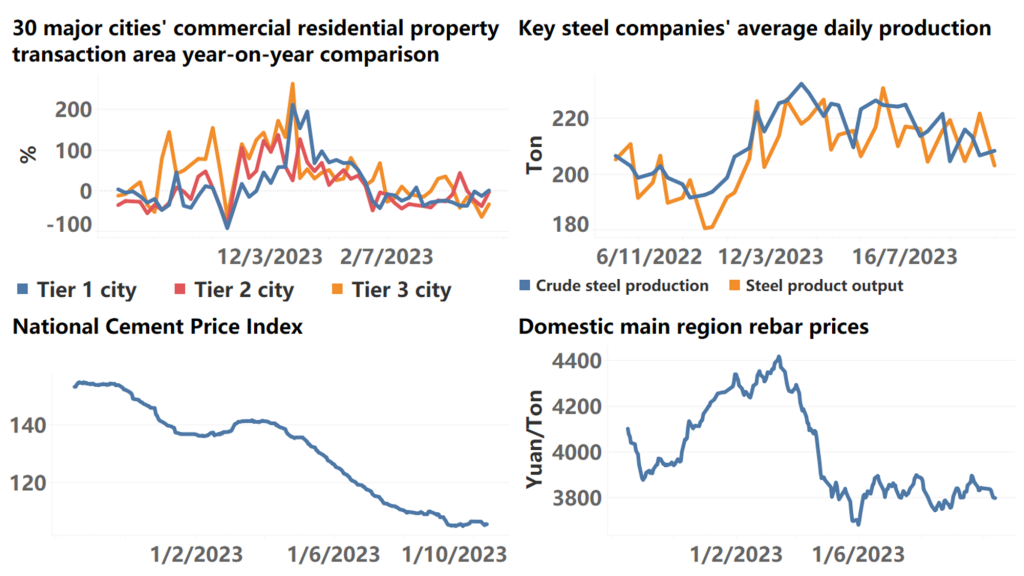

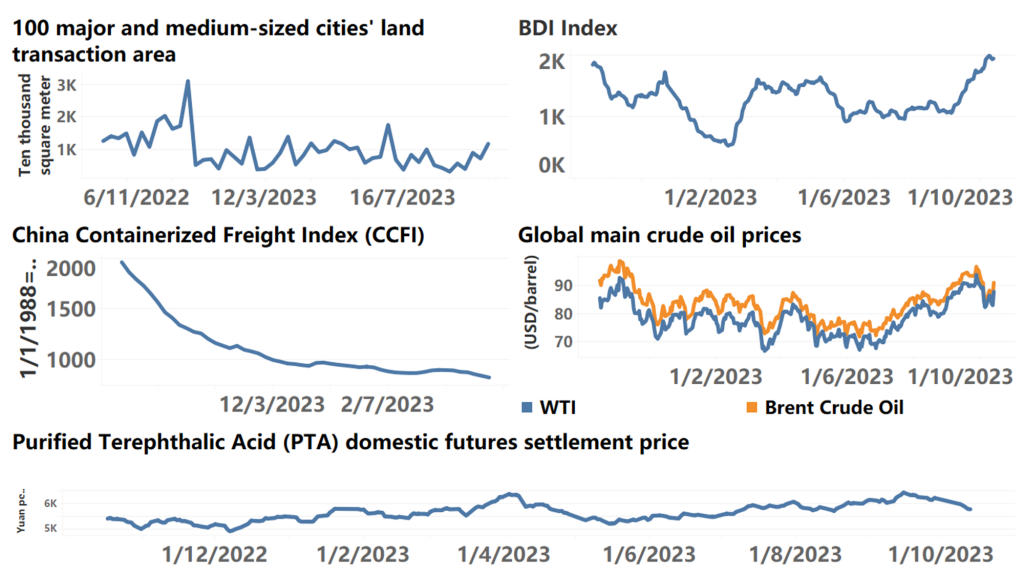

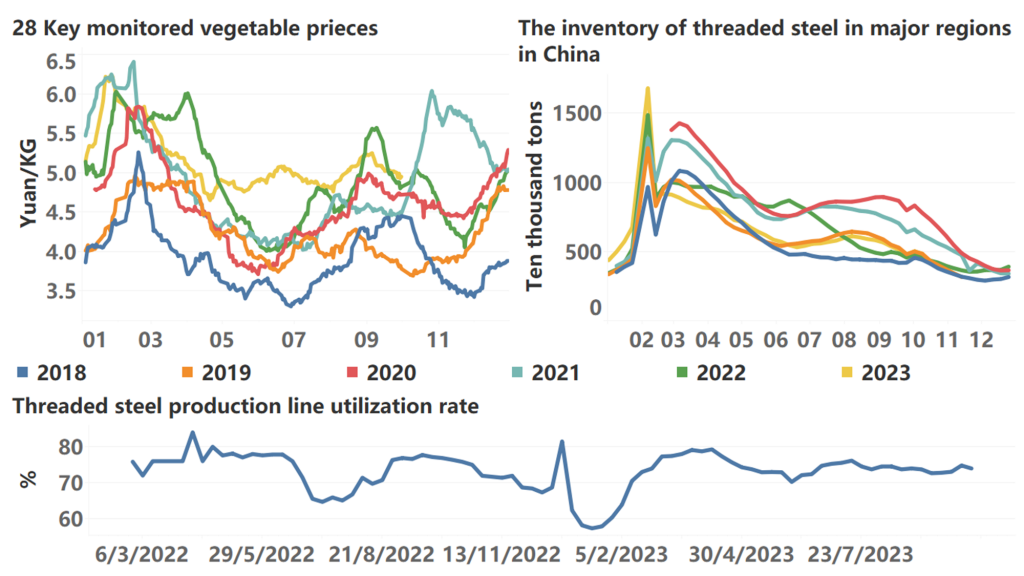

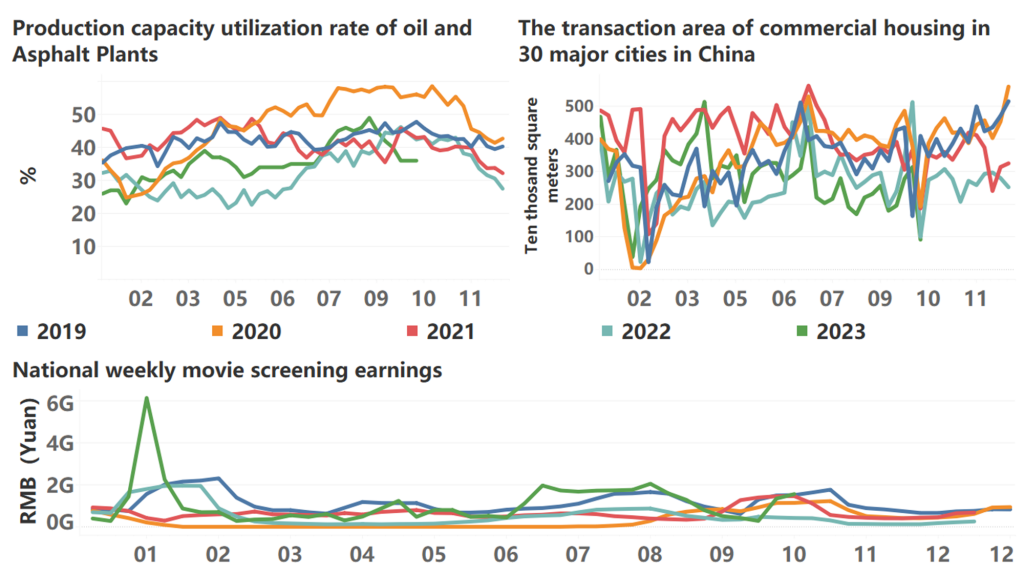

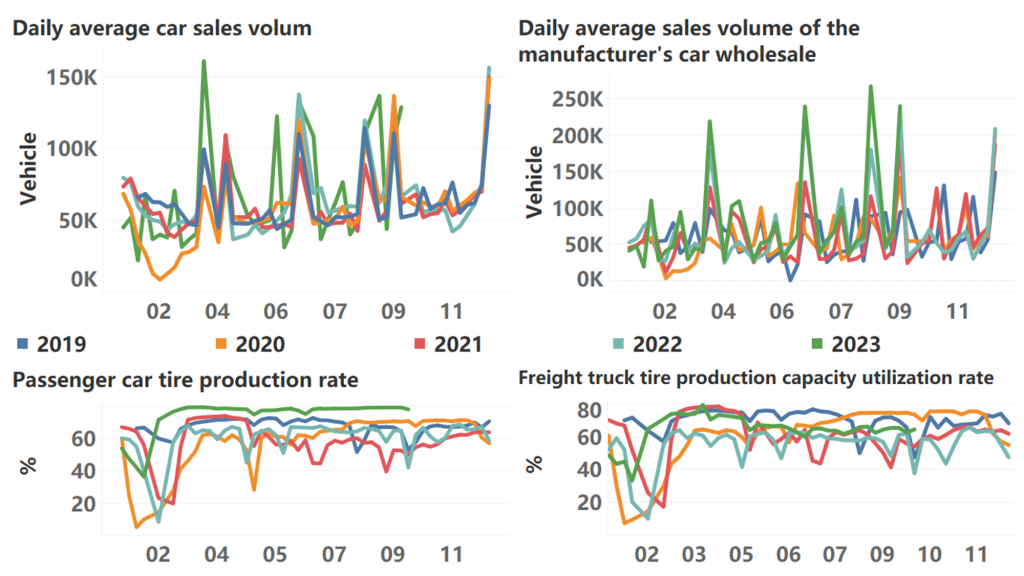

The following are high-frequency data for this week:

*Translated by ChatGPT