Since the beginning of this week, the dollar index has hovered around 103.5. The Dow Jones has basically bottomed out this week, and the NASDAQ has risen more than three percentage points this week. There are several scenarios for the future of the dollar index:

- Narrow fluctuation around 103.

- Continues to rise, touching the previous highs of 104 and 105.

- Falls to touch the previous low of 99.

As of now, the third possibility is unlikely. From mid-July to mid-August, the dollar index has risen all the way. During this process, gold prices have relatively fallen, oil prices have remained stable, and the ongoing rate hikes by the US and the relative strength of the US economy might be the reasons for the rise of the dollar index. Currently, there are two main risks:

Firstly, rating agencies like Fitch are considering downgrading US commercial banks. US regulators are also asking US commercial banks to increase their capital ratios. This will significantly suppress the expansion of credit by US commercial banks and reflects the accumulation of US debt problems, which is not supportive of further rate hikes.

Secondly, US CPI rose in July. Core CPI has been decreasing very slowly. Global energy and food prices have risen noticeably. If US CPI continues to rise in August and September, it will support the Federal Reserve’s decision to raise rates again in November. At present, the influence of rating agencies like Fitch seems to be dominant. For the dollar index to turn downwards, there needs to be a significant decline in the CPI for August and September. Before the US CPI announcement in August, the likelihood of a decline in the dollar index is minimal.

The second possibility is a continued rise. If the CPI in August goes up, then the dollar index is likely to touch a high of 104. Gold, oil, and global securities markets would respond.

The first possibility is fluctuation around 103. Without new factors and with no further deterioration in US inflation and some alleviation of debt risks, 103 might be a short-term equilibrium.

The impact on the global capital market under three scenarios:

- If the dollar index fluctuates narrowly around 103, the global capital market will resume its upward trend, surpassing its previous high and reaching the next plateau.

- If the dollar index rises, the global capital market will continue to fall.

- If the dollar index falls, the global capital market will overshoot upwards.

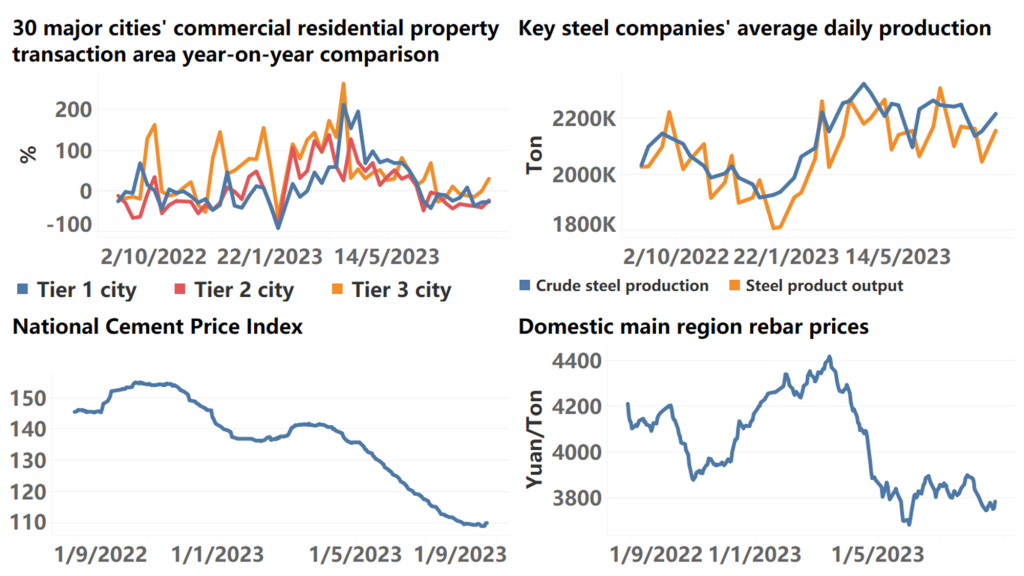

China: Rising prices in the black commodity sector From a macro perspective, the demand for the “black commodity” sector (like steel, coal) remains very weak domestically. The main factor for the current price increase is still driven by exchange rates. This Thursday, the securities prices related to infrastructure plunged, and risk factors erupted.

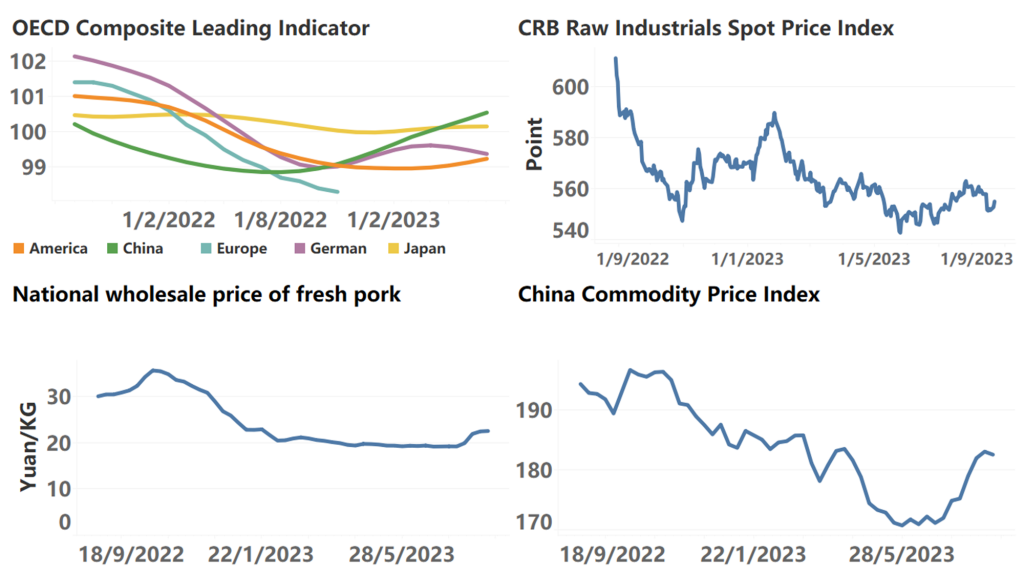

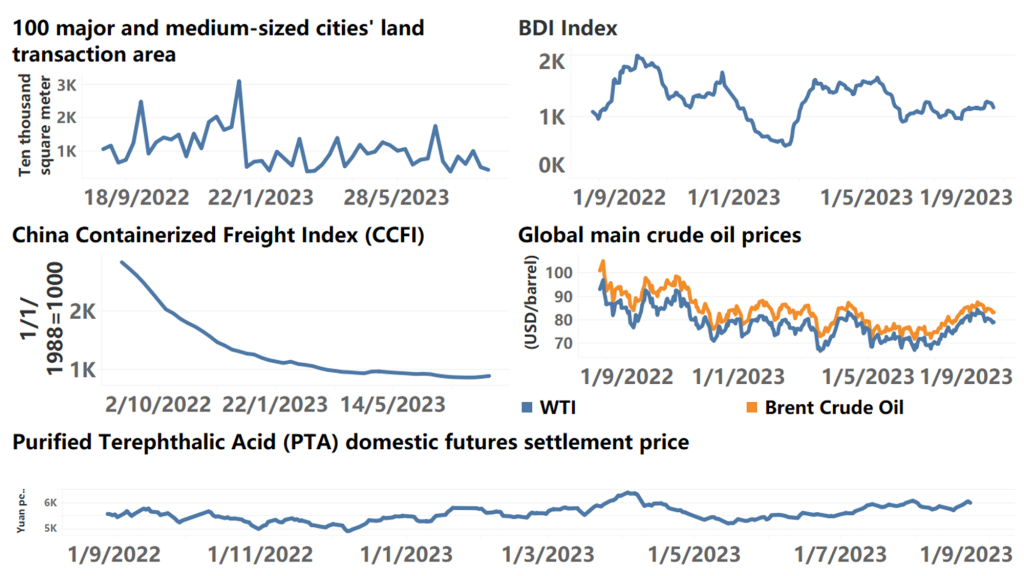

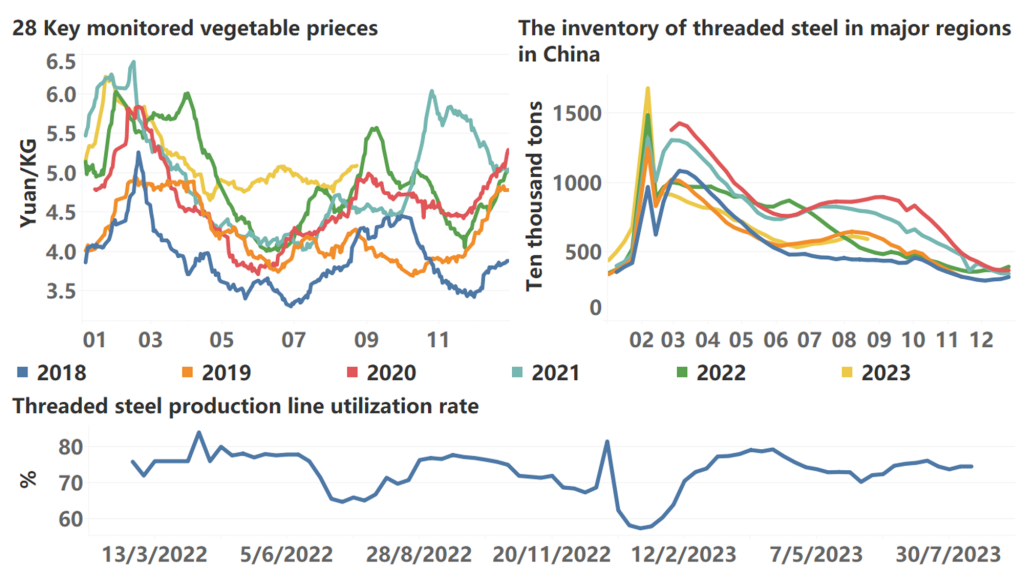

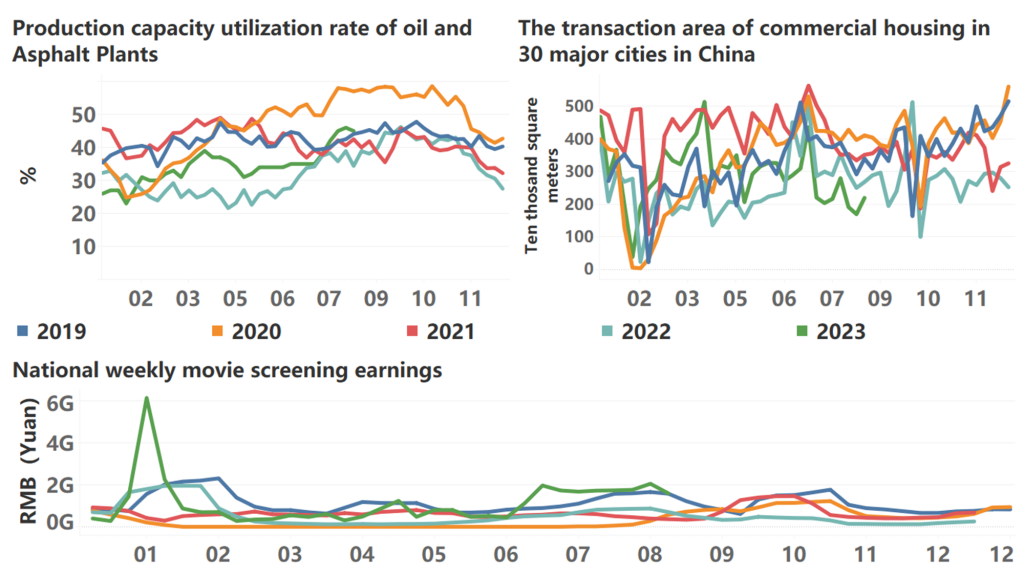

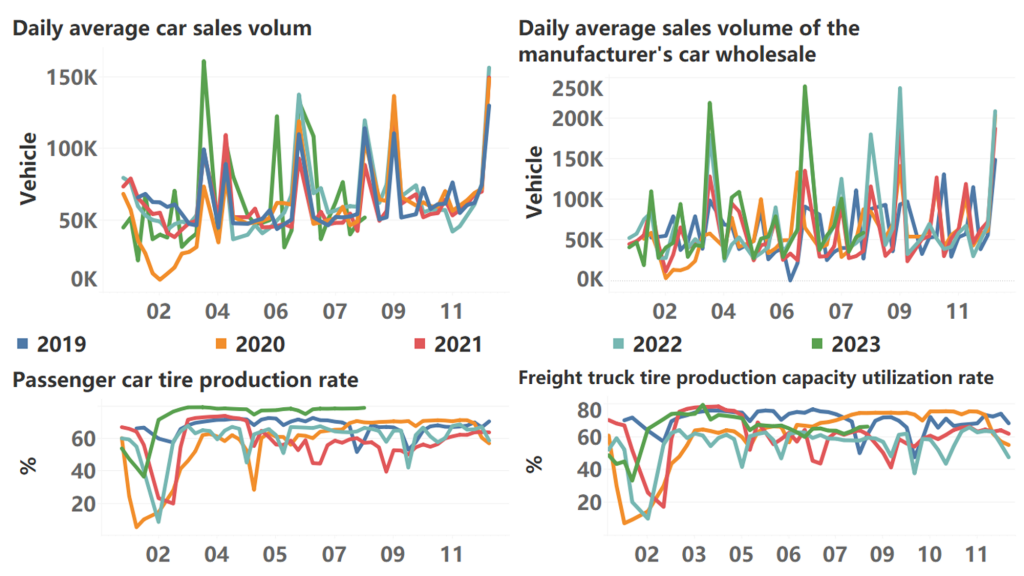

The following are high-frequency data for this week:

*Translated by ChatGPT