The GDP in the second quarter increased by 6.3% year-on-year, with a compound growth of 3.3% over two years. The consumer sector, real estate, and exports were noticeably dragging, with infrastructure and high-end manufacturing investments providing support. The GDP in the first half of the year increased by 5.5% year-on-year, higher than the annual growth rate of 3.0% in 2022, reflecting a continued recovery trend following the easing of economic activities. Excluding base effects, the economy was high in the first half of the year and low in the second; the two-year compound growth rates of GDP in the first and second quarters were 4.6% and 3.3% respectively.

After the release of the second-quarter data, major institutions have downgraded their expectations for China’s economic growth in 2023, but overall they maintain a judgement of 5% or more. In our view, a growth rate of 5% for the whole of 2023 should be a bottom line. Next, we can calculate the possible performance of consumption, investment, and imports and exports under the target of a 5% annual growth rate from the demand side.

First, we look back at the growth rates of consumption, investment, and imports and exports in 2022. In the second half of 2022, consumption began to rise from October due to a low base. If we take the basic situation of a two-year moving average of 3.1% in June 2023, in the second half of 2023, if retail sales meet this recovery situation, then the retail sales growth from July to December would be approximately 3.5%, 0.8%, 3.7%, 6.7%, 12.1%, and 8%, making the average growth rate in the second half of the year 5.8%. If retail sales growth can maintain the current recovery status, it won’t drag down the overall target.

In the second half of 2022, investment year-on-year cumulative growth rate gradually fell from 6.1% in January-June to 5.1% in January-December, falling by 1 percentage point over 6 months. In 2023, the investment year-on-year cumulative growth rate was 3.8% from January to June. If it can maintain the investment year-on-year cumulative growth rate in the second half of 2022, then the full-year cumulative year-on-year growth rate should be around 2.8%. Currently, the investment growth rate poses a significant challenge to the macroeconomic growth rate in the second half of the year. In this regard, it is necessary to consider the situation where the PPI is negative, i.e., when the investment level index is negative, it can support a certain actual growth rate. As of June 2023, the PPI year-on-year has fallen to -5.4%.

From January to June 2023, China’s total imports and exports were $29181.7 billion, a year-on-year decrease of 4.7%. Among them, exports totaled $16634.3 billion, a year-on-year decrease of 3.2%; imports totaled $12547.4 billion, a year-on-year decrease of 6.7%. According to the latest WTO forecast, Asia’s annual export growth rate in 2023 is 2.5%. Based on Asia’s export growth rate of 0.6% in 2022, the two-year average growth rate is approximately 1.55%. China’s cumulative year-on-year export growth rate from January to December 2022 was 7%. At a two-year average growth rate of 1.55%, the cumulative export growth rate from January to December 2023 is approximately -3.9%. Currently, exports from January to June increased by -3.2% compared to the same period last year, which means that the cumulative year-on-year will decrease by another 0.7 percentage points to -3.9%.

Next, comparing the data for the first and second halves of the year, if the main three items on the demand side all decrease by one percentage point, the total value will also decrease by one percentage point. According to previous estimates, retail sales in the second half of the year will decrease by 2.4 percentage points, investment will decrease by one percentage point, and exports will decrease by 0.7 percentage points. Therefore, the total value will decrease by more than 1.5 percentage points. The economic growth in the second half of the year may be around 4%, and the annual growth rate is around 4.75%. This figure is lower than the expected target. Investment is a significant drag, and it is also a handle for macro policy adjustments, with export uncertainty being quite large. An undisputed fact is that overall economic demand is still relatively weak, and it needs macro policy adjustments to make a difference. We have analyzed how short-term and long-term policies can coordinate in our previous report. Stabilizing retail sales growth and increasing investment in the second half of the year is key to achieving the 5% growth target for the whole year.

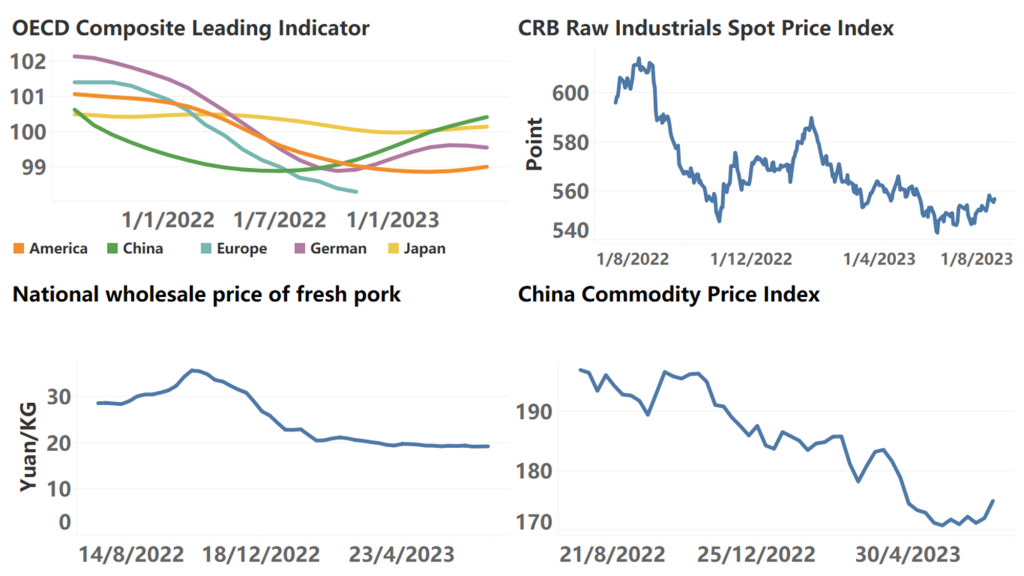

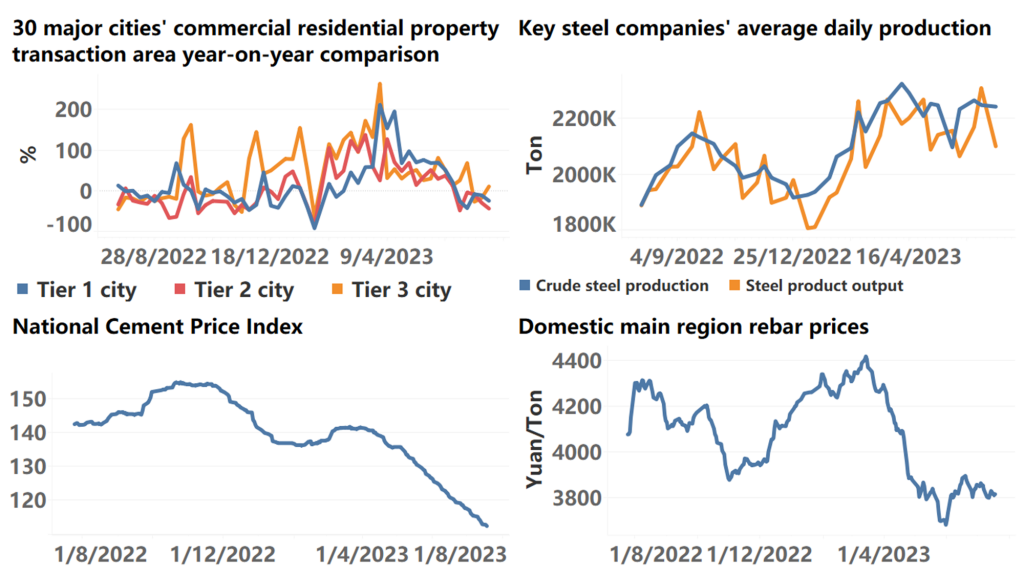

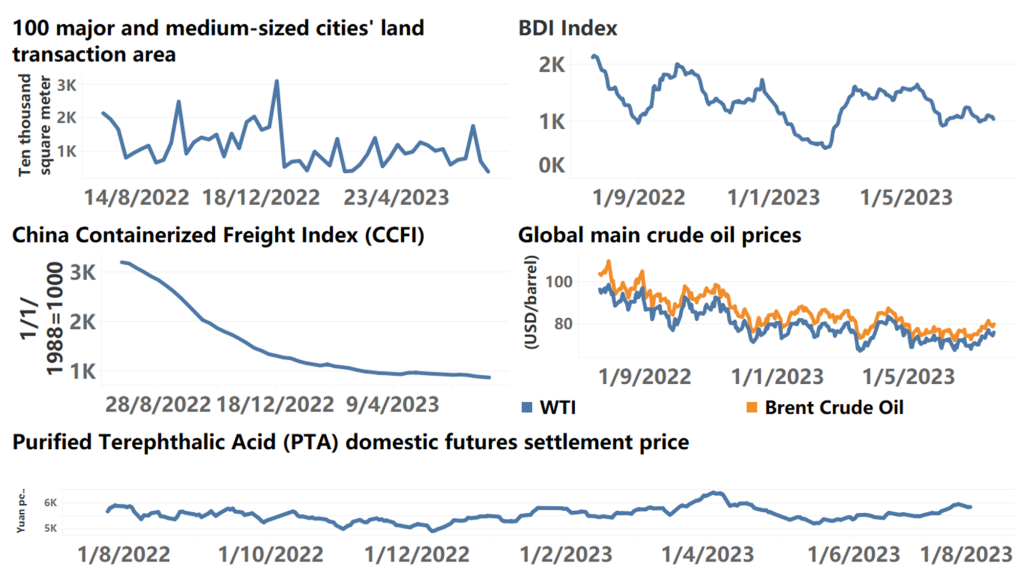

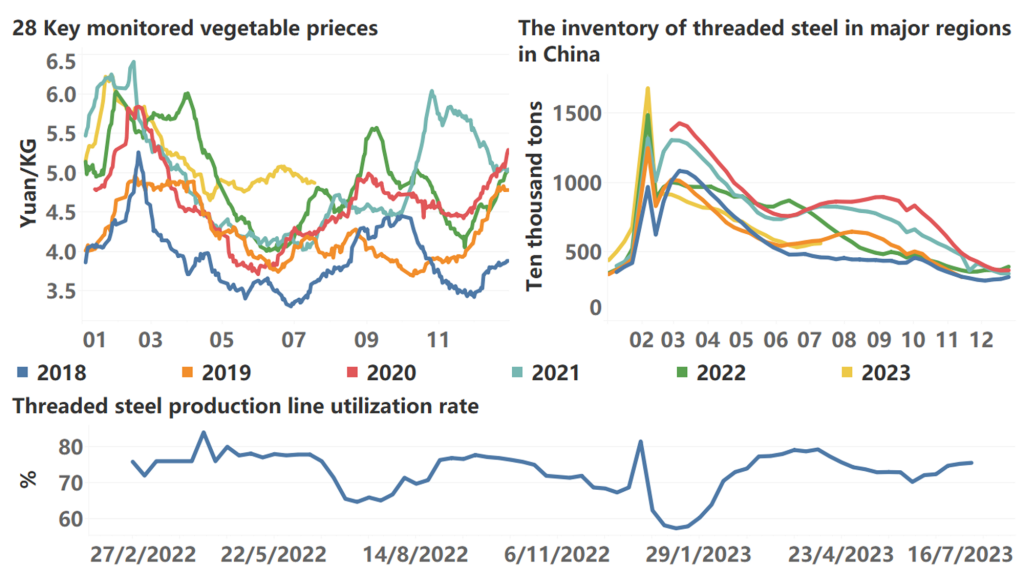

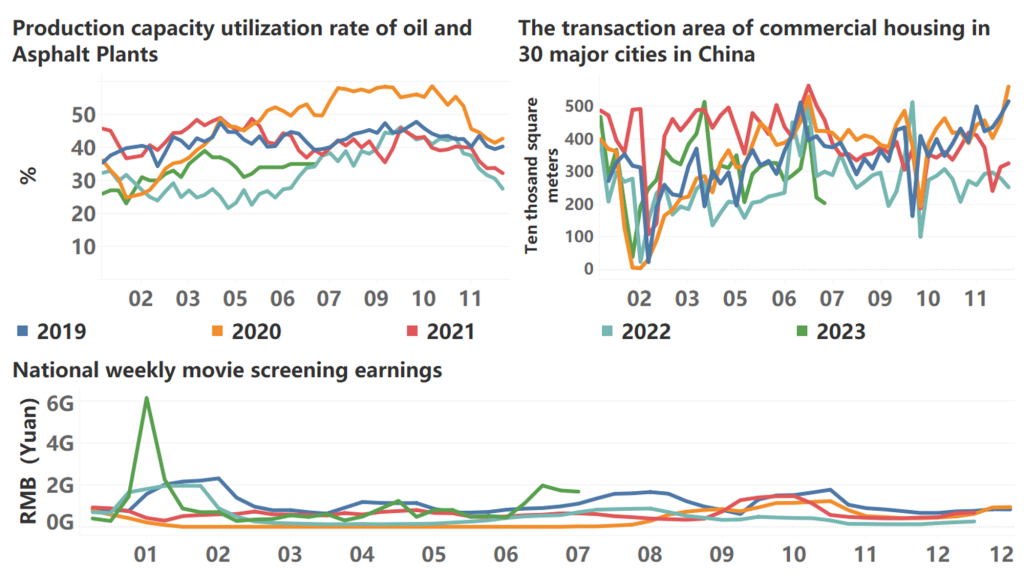

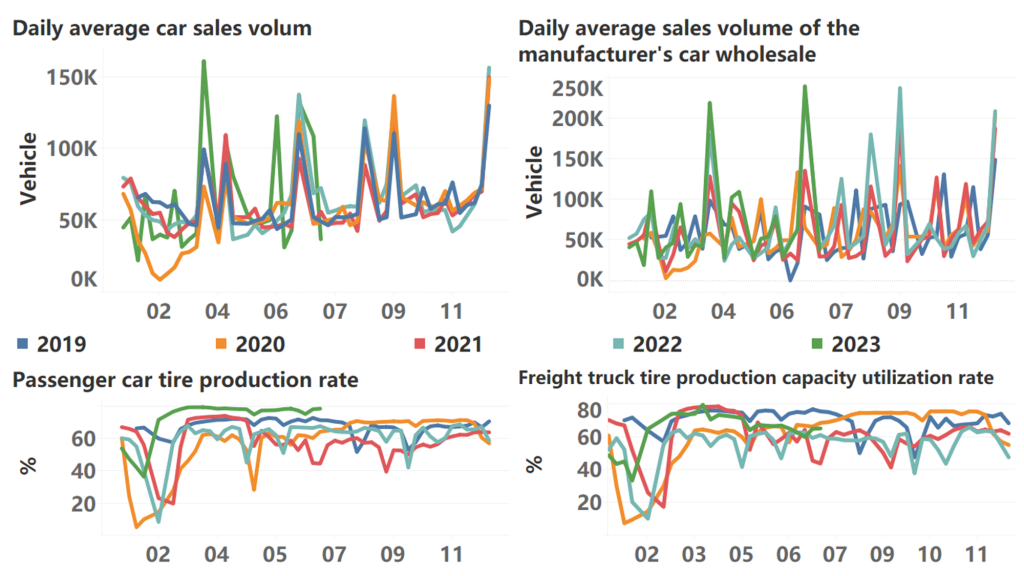

The following are high-frequency data for this week:

*Translated by ChatGPT