United States: Darkest Hour is Over

On July 12th, the U.S. Department of Labor released the June Consumer Price Index (CPI) data. The CPI year-on-year growth rate was 3% (expected 3.1%), with a month-on-month increase of 0.2% (expected 0.3%). The core CPI, which excludes food and energy, had a year-on-year growth rate of 4.8% (expected 5.0%) and a month-on-month increase of 0.2% (expected 0.3%), which was lower than market expectations. While the 3% figure was only 0.1 percentage point lower than expected, it still caused changes in global asset prices within a short period of time. In the following trading days, the U.S. dollar index continued to decline, and the pricing of the U.S. CPI data had a significant impact on global capital markets last week. A mere 0.1 percentage point difference from the expected value led to an overall adjustment in global asset prices, indicating that the market’s expectations for the decline in U.S. CPI were relatively conservative.

In our previous report, we presented two viewpoints: 1) Long Nasdaq; 2) Overvaluation of the U.S. dollar. The Nasdaq represents primarily technology companies with relatively light balance sheets. Once the market outlook turns pessimistic, they can reduce costs through layoffs, which is also a significant reason for the massive layoffs in the platform economy within the U.S. This information can be interpreted as the flexibility of the platform economy. As the economy emerges from the shadow of stagflation, the platform economy may be the most active group in terms of expansion. The overall performance of the Nasdaq index indicates that it has considerable investment value. Following the disclosure of U.S. CPI data, the Nasdaq index surged again, significantly outperforming other asset indices.

From the perspective of the U.S. dollar index, it represents the exchange rate of the U.S. dollar against the currencies of major U.S. trading partners, including the G7 countries. The U.S. dollar index cannot remain strong when expectations for interest rate peaks in the British pound and euro are high. Additionally, as an international reserve currency, the U.S. dollar tends to strengthen when the global economy weakens. The disclosure of U.S. CPI data lagged behind Europe. After the U.S. CPI data was released, it completely changed global expectations for U.S. interest rate peaks and global stagflation risks, ultimately resulting in a weakened U.S. dollar index.

Against the backdrop of the adjustment in key asset prices such as the Nasdaq index and the U.S. dollar index, global asset prices have also adjusted rapidly. Among them, the Nikkei index has shown a slight rebound, and European indices have recorded consecutive gains. As for Japan, we have previously mentioned the risk points of the “new normal” in the Japanese economy, particularly whether Japanese inflation can maintain high levels after intersecting with U.S. inflation. This risk is also reflected in the performance of the Nikkei index, which has shown a significant slowdown compared to European indices.

After this round of asset price adjustments, the major stock indices in the United States, Europe, and Japan seem to have entered a plateau phase. What kind of events will ignite an upward or downward trend? One of the important factors will be the statements of Federal Reserve Chairman Powell after the upcoming Fed meeting. It can be anticipated that Powell is likely to take a hawkish stance given that core inflation remains relatively high. In addition, factors such as U.S.-China relations, the APEC summit, the Russia-Ukraine conflict, and the prospect of a European recession are also worth considering. Currently, we still maintain the recommendation not to go short.

China: Urgent Need for Demand Boost

In June, China’s exports (denominated in U.S. dollars) decreased by 12.4% year-on-year, while imports decreased by 6.8%. The trade surplus stood at $70.62 billion. China’s CPI for June remained unchanged compared to the previous year, with an expected increase of 0.1% (previous value was 0.2%). The year-on-year Producer Price Index (PPI) was -5.4%, lower than the expected -5.0% (previous value was -4.6%). By the end of June, the broad money supply (M2) balance reached CNY 28.73 trillion, with a year-on-year growth rate of 11.3%, 0.3 and 0.1 percentage points lower than the previous month and the same period last year, respectively.

The June price and financial data indicate that domestic demand in China remains relatively weak, while the significant decline in import and export figures suggests a continued downturn in external demand. How should we approach this issue? What kind of stimulating measures can be implemented in the short term? What are the long-term prospects for the economy? Recently, three topics have been extensively discussed in the market:

- Is Gu Chaoming’s balance sheet theory correct?

- Is China following the path of Japan’s past?

- What caused Japan’s failure back then: external factors or mistakes in internal macroeconomic policies?

Clearly, these three questions revolve around long-term discussions. However, long-term prospects determine the direction of short-term macroeconomic policies. In other words, resolving long-term issues may take precedence. Clarifying long-term problems will guide short-term actions. Currently, three viewpoints exist:

- Gu’s theory emphasizes using fiscal policy as the main tool to address existing debt in the economy.

- Monetary policy should take the lead, with interest rate cuts and even quantitative easing.

- Avoid indiscriminate stimulus and promote structural reforms.

Regarding this issue, we have systematically reviewed the economic cycle histories of over a dozen countries, including China, in our published works such as “Currency Stability, Inequality, and Business Cycles Study” and the upcoming “A Brief History of China’s Business Cycles, 1978-2023”. These studies reveal that after the surge in the cost of living index (DPIL), an economic recession due to insufficient demand often occurs. It appears that China is currently facing a similar problem. However, China has its own budgetary constraints, and based on the spirit of central government documents, the third solution may be a standard scenario. Resolving the significant debt issue in the economy in this standard scenario will likely require higher inflation or new economic driving forces. The question of whether demand can be stimulated is a significant challenge.

In the third solution, real estate may be the biggest obstacle. From the current secondary housing market perspective, prices have continued to decline, while the supply of second-hand housing has been increasing. The overall real estate market inventory, which was previously concealed for speculative purposes, is being released as speculators are eager to sell due to the downward pressure on prices. Regardless of which structural reform approach is adopted, stability in the prices of second-hand housing transactions is an important indicator.

Given the aforementioned standard scenario, it can be expected that monetary policy in the short term should proceed cautiously, while fiscal policy should be implemented gradually, with continued anticipation of structural reform proposals after the Third Plenary Session. If the above predictions hold true, the overall performance of the A-share market will have limited gains. Furthermore, the unemployment rate for the age group of 16-24 reached 20.8% in May, which may deter policymakers from adopting overly expansionary measures.

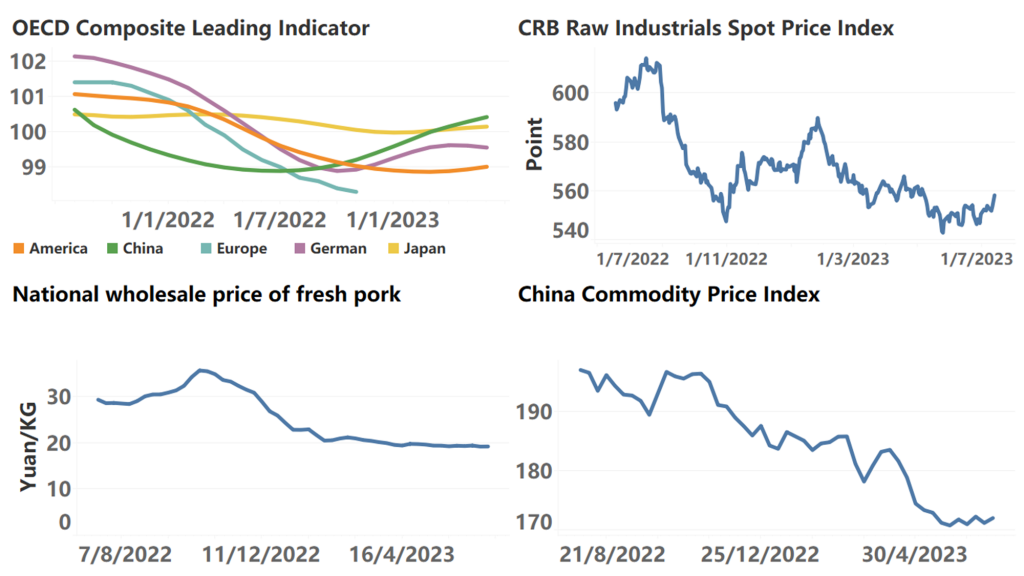

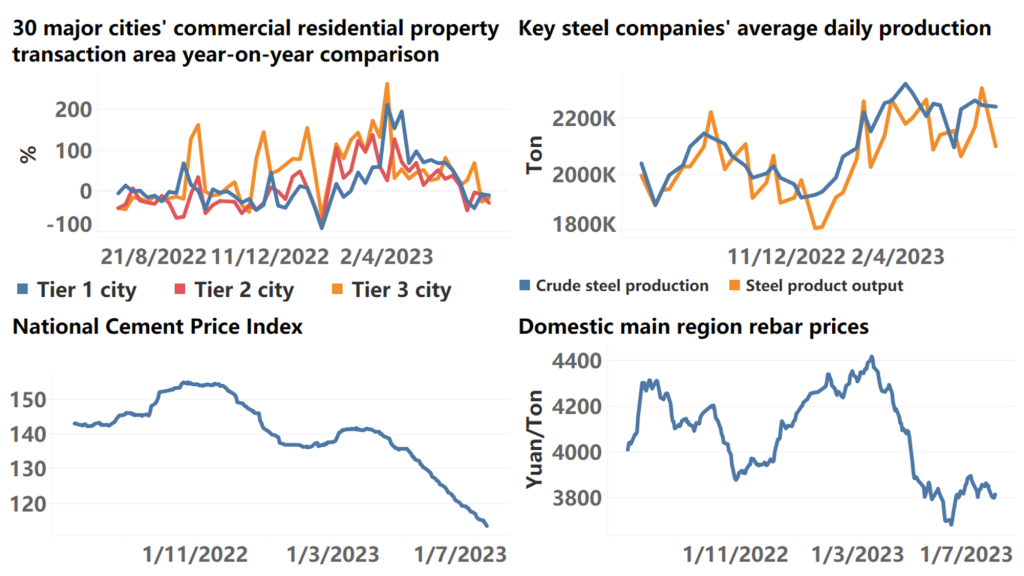

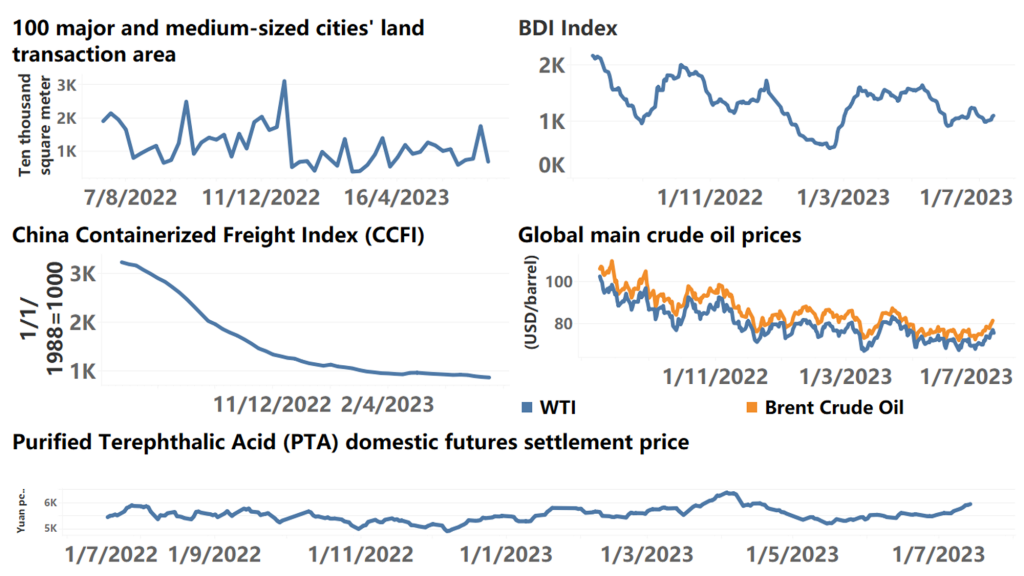

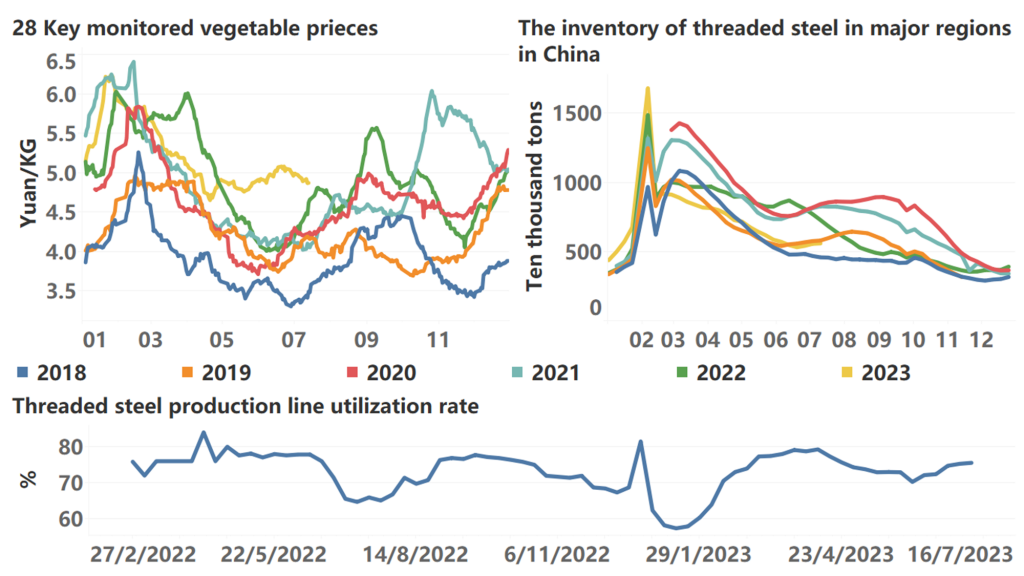

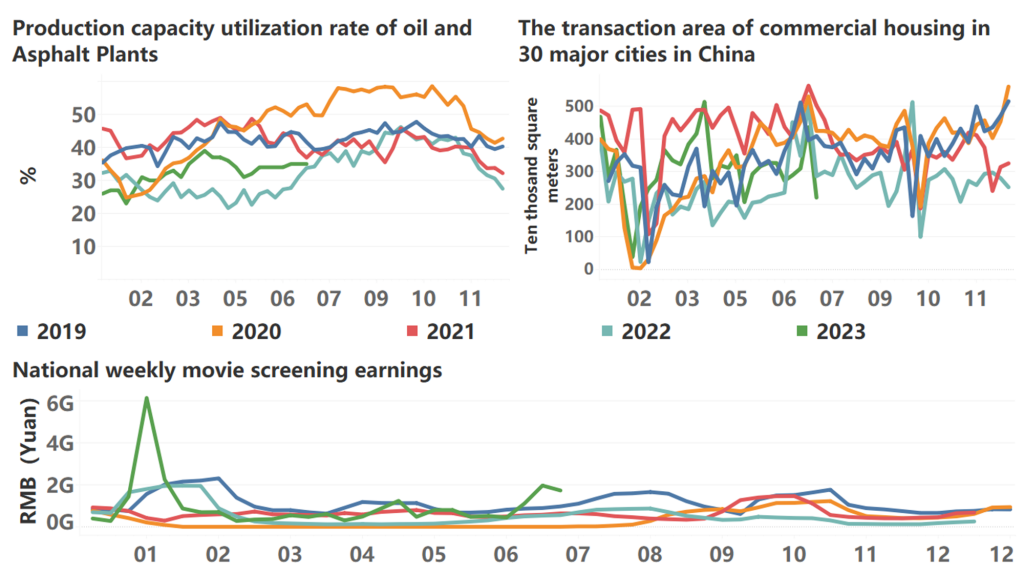

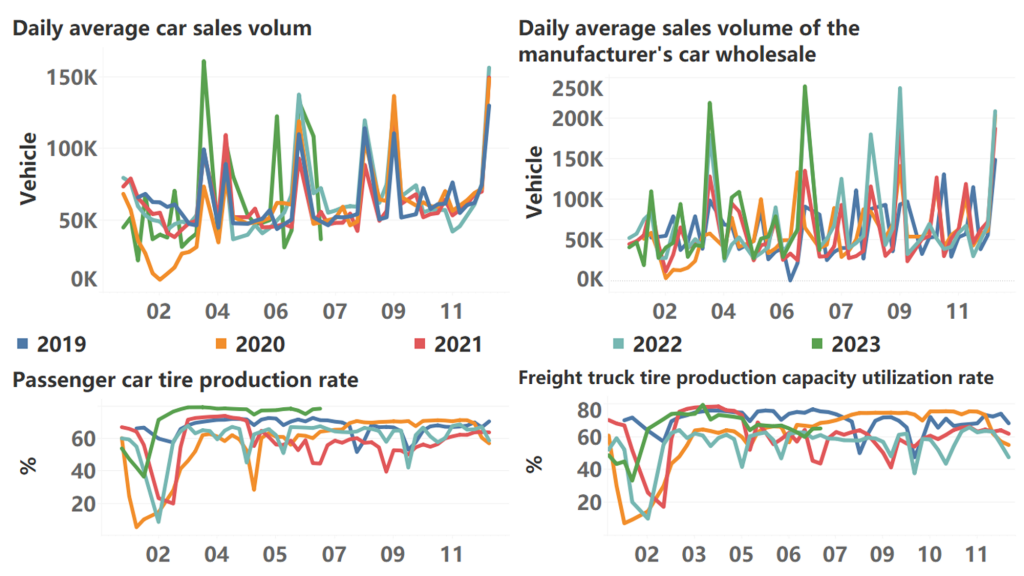

The following are high-frequency data for this week:

*Translated by ChatGPT