Market

In a speech to Congress on June 21 (U.S. time), Jerome Powell mentioned, “Almost all Federal Open Market Committee participants anticipate that it would be appropriate to tighten monetary policy further by the end of the year. However, at last week’s meeting, considering how far and how fast we’ve acted, we believe it’s prudent to keep the target range steady so the Committee can assess more information and its impact on monetary policy. In determining the additional degree of policy tightening that may be appropriate over time to return inflation to 2%, we will take into account the cumulative tightening of monetary policy, the lagging effects of monetary policy on economic activity and inflation, as well as economic and financial developments. We will continue to make decisions at each meeting based on all the data received and its impact on the outlook for economic activity and inflation, as well as the balance of risks. We remain committed to our goal of returning inflation to a 2% target and maintaining a solid anchor for long-term inflation expectations. Reducing inflation may require a period of below-trend growth and some degree of slack in the labor market. Restoring price stability is critical to achieving maximum long-term employment and price stability.”

After Powell’s speech, global stock markets fell collectively. The Nasdaq dropped from a closing price of 13667.29 on June 20 to a closing price of 13492.52 on June 23, with major declines on June 21, 22, and 23; the Dow Jones fell from a closing price of 34053.87 on June 20 to 33727.43 on June 23, mainly on the 21st and 23rd. The Nikkei fell from 33607.49 on the 21st to 32751.1 on the 23rd, with the 23rd being the largest drop. The Hang Seng Index dropped from a closing price of 19607.08 on June 20 to 18889.97 on the 23rd, with the 23rd being the largest drop. The level of panic in this Hang Seng drop is close to that on X-day. Powell’s speech indeed dampened global investor sentiment, and this drop was mostly due to emotional factors. Looking at the trend in the global gold market, prices are gradually declining, and the market’s expectations for a global recession are weakening.

Last week, we released our viewpoint “Continue to Be Bullish”. We believe that this drop, affected by sentiment, is short-term. From a longer time dimension, we still maintain a bullish view, especially on the Nasdaq. Powell also conveyed an optimistic attitude in his speech, showing a clearly optimistic mood about economic risks.

In the current economic and outlook segment, Powell stated: “The U.S. economy slowed significantly last year, and recent indicators show that economic activity continues to expand moderately.” “The labor market remains very tight.” “The inflation rate is still far above our long-term target of 2%.” “Despite the rise in inflation, long-term inflation expectations seem to be well anchored, which is reflected in extensive surveys of households, businesses, and forecasters, as well as measures in the financial market.” The risks ahead for the U.S. economy seem to be diminishing, and there has been no fundamental change in long-term inflation expectations. We need to consider the timing of the Federal Reserve’s next interest rate hike and the peak of the interest rate. The dates of the Fed’s interest rate meetings in the second half of the year are July, September, October, and December. From the perspective of inflation development, it is very likely that there will be no rate hike in December. Interest rate hikes in July and October could be a standard scenario, with two rate hikes of 25BP and 15BP, respectively, and the peak interest rate at 5.65%. If the core CPI drops rapidly in August, September, and October, then the 15BP step in October could be canceled.

The current Federal Reserve policy interest rate is 5-5.25%, and the core CPI is 5.3%, so the real interest rate is still negative. If another 25BP is added, then the policy interest rate reaches 5.25-5.5%. Even if the core CPI drops by 0.1 percentage point each month over the next two months (a conservative estimate), it will fall to about 5%, at which point the real interest rate turns positive, breaking the wage-inflation spiral. If the core CPI data for the next August, September, and October can fall rapidly, then the rate hike in October is likely to stop. By this standard, the global stock market may fluctuate, but overall it should go up, with plenty of cyclical opportunities. Economic growth fundamentals and sentiment are still the two most important factors, and a rapid rise in stock prices may be hit by the hawkish Federal Reserve. From the Federal Reserve’s perspective, it probably does not want the financial environment to ease too quickly.

In addition to the pace of the Fed’s rate hikes, a few data indicators are worth discussing:

- Crude oil prices

- Gold prices

- The exchange rate between the U.S. dollar and the Renminbi

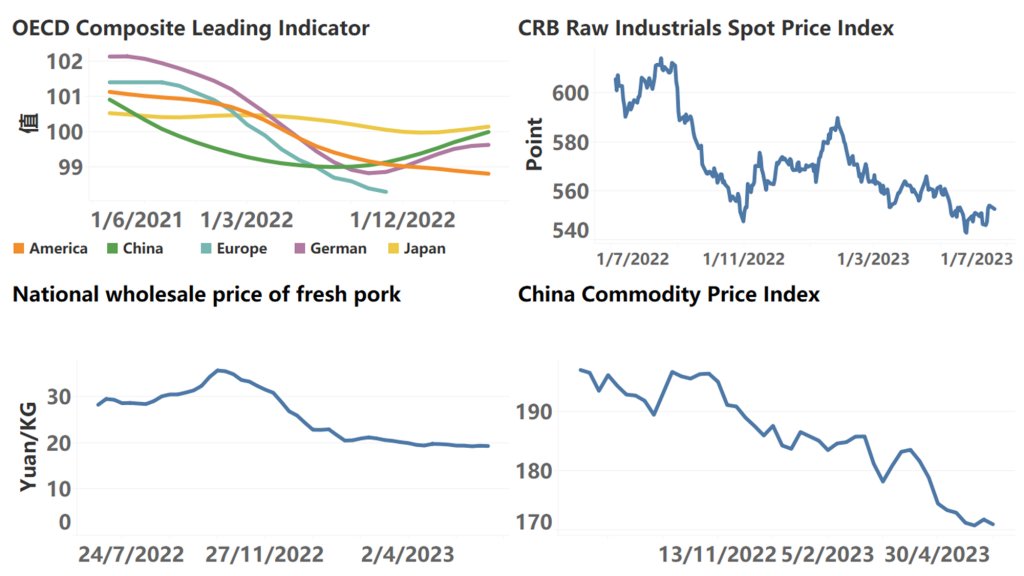

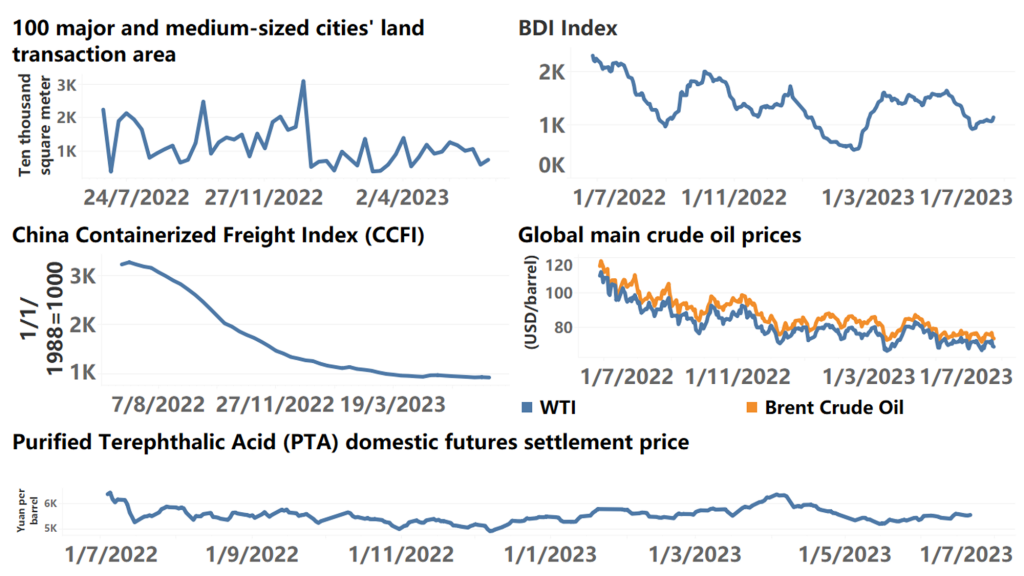

For crude oil prices, the supply and demand fundamentals are the most important factors. After this round of overall inflation in the Western world, if we regard the price of crude oil as the economic interest of the entire OPEC+ world, the price of crude oil should permanently increase compared to before the pandemic. From the perspective of crude oil production profits, the production cost of crude oil is fixed. If the profit of crude oil relatively decreases, then the overall profits of the OPEC+ countries will drop. This will cause a strong reaction from the OPEC+ countries. It is not a wise choice to easily short oil. Recent fluctuations in oil prices have not deviated from the basic level of Brent crude oil at $75/barrel, and it is currently not easy to observe how much impact the global energy transition will have on crude oil demand. Therefore, judging global output levels to be 10% lower than before the pandemic, from the perspective of global oil supply being reduced by about 10%, may not be a particularly good reference.

The COMEX gold price fell from a high point of 1992.8 a month ago (May 23) to 1930.3 on June 23, a significant decline, and it may continue to fall. The price of gold rose in tandem with the global commodity market, and then as inflation fell, global commodity prices gradually declined, but the price of gold as a recessionary indicator did not fall with global commodities, but continued to rise, surging to around the historical high of 2000. At present, after X-day, with the backdrop of the Fed pausing rate hikes, the turning point in gold prices may have already occurred.

The U.S. dollar to Renminbi exchange rate continues to rise, from 7.06 on May 23 to 7.21 on June 23, both the increase and speed are rapid. Some believe that seasonal factors have played an important role: July-August is the peak of Renminbi exchange, profits of listed companies are adjusted outward, and the willingness of trade companies to settle exchanges decreases. However, the level of 7.21 is still relatively high. Although the U.S. dollar index has maintained a high position since it rose from 100 to 102, the speed of Renminbi depreciation is still too fast. The global market’s expectations of Renminbi interest rate cuts may be a major factor. In other words, the space for Renminbi monetary policy seems to be shrinking. From the perspective of a financial price, the basic economic growth and investor sentiment are also the two most important factors. The PMI of China’s manufacturing industry has been below the boom-bust line for two consecutive months, which seems to have disturbed investor sentiment. The fall in Renminbi prices has caused the price of assets denominated in Renminbi to slow significantly relative to the price of global assets. The fundamental aspect of China’s economic growth is still awaiting a breakthrough from China’s structural economic reforms. Since 2015, China’s stock market has been short in bulls and long in bears, possibly also influenced by the real estate market price. But the real estate market has indeed undergone fundamental changes, and the seesaw relationship between the financial market and real estate may change in the future.

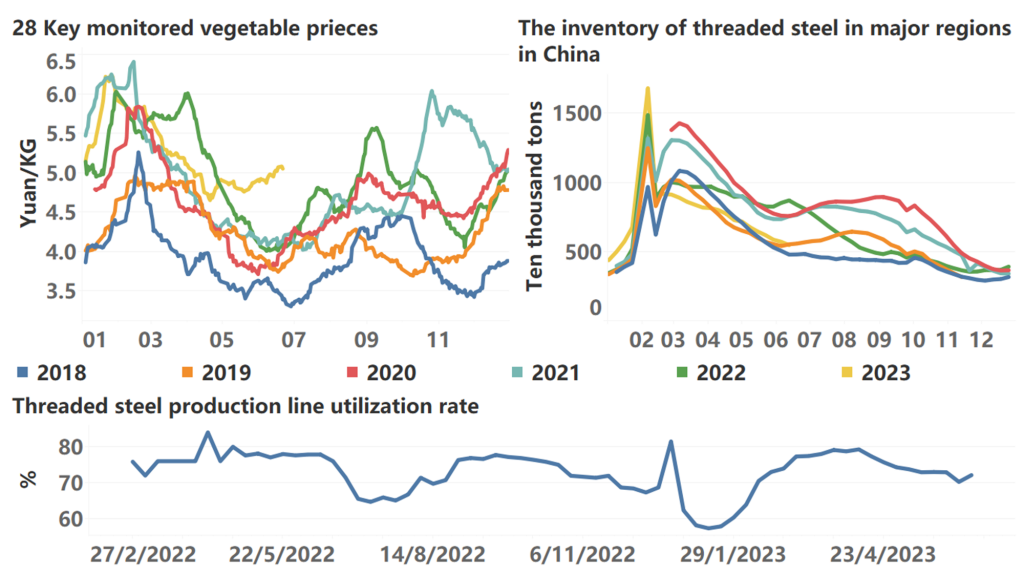

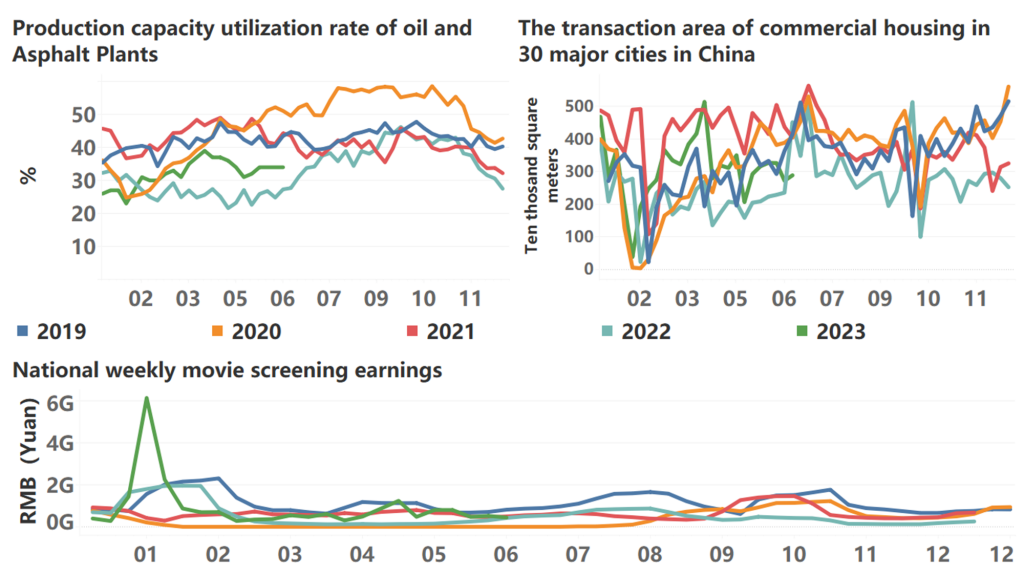

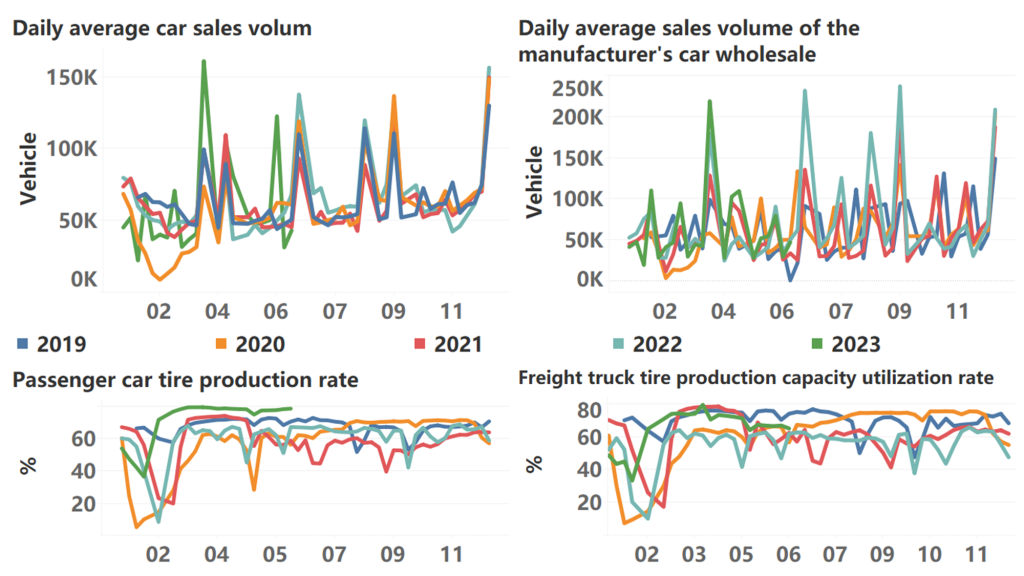

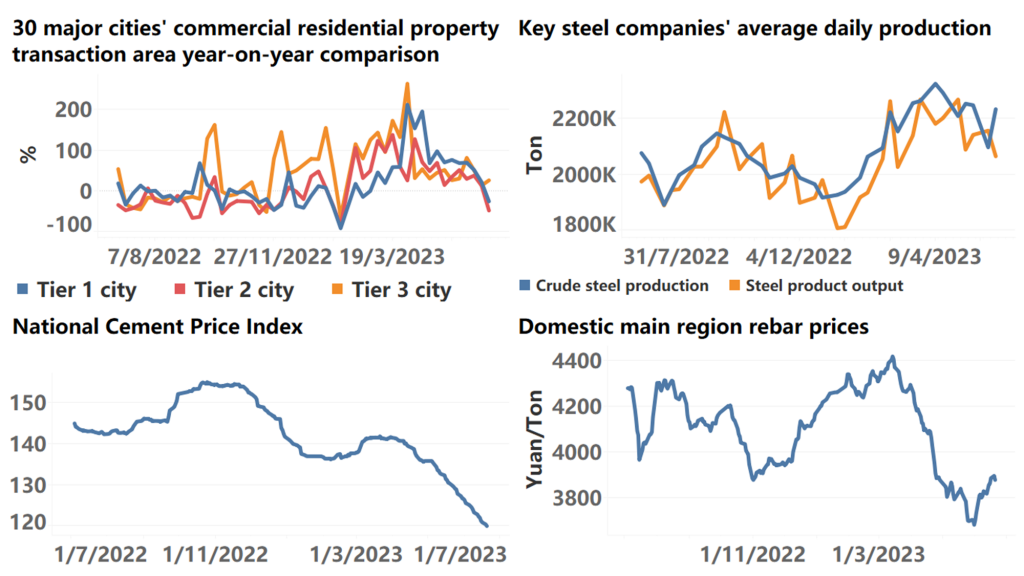

The following are high-frequency data for this week:

*Translated by ChatGPT