This week, global capital markets were mostly on the rise. The Nikkei 225 index rose from 26,945 to 30,808, reaching a historic high. The Nasdaq increased from 12,365 to 12,657, while the Dow Jones went up from 33,348 to 33,426. The Frankfurt index rose from 15,917 to 16,275, while the UK’s FTSE 100 index experienced a slight decline from 7,777 to 7,756. In the domestic market, the Shanghai Composite Index dropped from 3,310 to 3,283, and the Shenzhen Component Index decreased from 11,178 to 11,091. The US Dollar Index rose from 102.43 to 103.20, and the USD/CNY exchange rate in the onshore market increased from 6.958 to 7.014. The NYMEX Gold Futures for 2021 fell to 1,998, and Brent Crude Oil fluctuated slightly from 75.56 to 75.59. Currently, the Nasdaq remains relatively low compared to other indices.

Global Macro

The US Dollar Index and global capital markets are strong.

Scenario 1: When economic growth stagnates, the movement of currencies should be opposite to that of stocks because the return on currencies corresponds to risk-free returns, while stocks correspond to risk returns. When the economy stagnates, the total wealth remains unchanged, making it difficult for both currencies and stocks to increase simultaneously.

Scenario 2: When the economy faces a recession, the contraction of wealth stock does not support the simultaneous rise of both currencies and stocks. Currently, the simultaneous strength of currencies and stocks suggests that there is likely a compromise between a soft landing of the economy and a successful debt ceiling negotiation. The short-term simultaneous rise may be due to a change in market expectations regarding the Fed’s interest rate hike. Firstly, the Fed is unlikely to cut interest rates in the short term, which keeps the return on the US dollar high and advantageous compared to other global assets. Secondly, the resilience of the US economy (with a strong job market) is shaping investors’ expectations of a soft landing, and they continue to be optimistic about the US stock market. Based on the current data, the global market is betting on US economic growth. We still adhere to the previous view that the risk of shorting stocks remains significant, but there are still trading opportunities to short the US dollar index and go long on gold.

Why?

This is essentially the relative relationship between financial stability and economic growth. Looking at US inflation data, the process of going from 4.9% to 2% will be exceptionally difficult and slow, and there may be a scenario of inflation rebound. This presents an opportunity to short the US dollar and go long on gold. However, the stock market is related to financial stability, and currently, almost all banks worldwide have unhealthy balance sheets and cannot withstand sharp fluctuations in the stock market. Central banks around the world will undoubtedly take temporary measures to stabilize the financial markets. Caution should be exercised regarding expectations of a Fed interest rate cut because the entire central bank credit system will not change easily, and they must follow through on their commitments.

Japan Issue

What factors are supporting the significant increase in the Nikkei index beyond the growth level of global assets?

Since the end of March, the Nikkei index has been rising rapidly. The international media attributes the unexpected growth of the Japanese economy (1.6% year-on-year GDP growth in the first quarter) to the full reopening of the Japanese economy, which is closely related to Chinese tourists. However, considering the size of the Japanese economy, it is unlikely that the growth is solely driven by the tourism industry.

According to the information provided by the Japanese Cabinet Office, the current Japanese economy is experiencing a moderate recovery, although some weaknesses exist.

- Private consumption is gradually recovering.

- Business investment is picking up.

- Exports remain weak.

- Industrial production has been sluggish recently.

- Overall corporate profits are improving, although at a moderate pace. The assessment of current business conditions shows a warming trend.

- The employment situation is improving.

- Consumer prices are rising.

In the short-term outlook, under the “new normal” circumstances, the economy is expected to show a recovery trend with the support of policy measures. However, risks to the Japanese economy include a global economic slowdown due to ongoing monetary tightening and other factors. Attention should also be paid to issues such as rising prices, supply-side constraints, and volatility in financial and capital markets.

Regarding policy stance, the government plans to swiftly and steadily implement comprehensive economic measures to address rising prices and revitalize the economy. These measures include supplementary measures prepared by the Ministry of Prices, Wages, and Comprehensive Measures for Living, as well as the additional budget for fiscal year 2022 and the budget for fiscal year 2023. The goal is to achieve a comprehensive recovery of the Japanese economy and put it on a new growth path.

The government will continue to maintain the framework for economic and fiscal management and jointly promote bold monetary policies, flexible fiscal policies, and a growth strategy that encourages private investment. It will flexibly adjust the macroeconomy without hesitation, achieve self-led growth driven by private demand, and overcome deflation.

The government expects the Bank of Japan to achieve the 2% price stability target in a sustainable and stable manner based on economic activity, prices, and financial conditions.

The significant rise in the Nikkei index is essentially pricing in the new normal of the Japanese economy. We have two conjectures about the new normal:

- Inflation has led to wealth redistribution, forming a spiral of inflation-wage increases and driving the economy onto an upward trajectory.

- The temporary increase in the mortality rate of the population has relieved the burden on the overall young population.

How far the Nikkei index can go depends on whether Japan has entered a long-term new normal. There are several important indicators to observe, with GDP growth rate being the most important. Whether the expansion of consumption and investment can push the supply-demand equilibrium point to move outward in the long term and whether the high growth rate of CPI can be stabilized. From the perspective of the overall economic progress of the G7, Japan’s CPI growth rate has not reached the levels of Europe and the United States, indicating room for further increase. However, when Japan’s CPI reaches the same level as the United States, it will be difficult for Japan’s CPI to continue rising and will likely follow the United States in a decline. The key is to see at what level it stabilizes after the decline. Based on the statements from the Federal Reserve, it may decline to 2% by early next year. In that case, where will Japan’s CPI head? When Japan’s CPI reaches the same level as the United States, we should lower our expectations of the Nikkei index relative to other global stock markets.

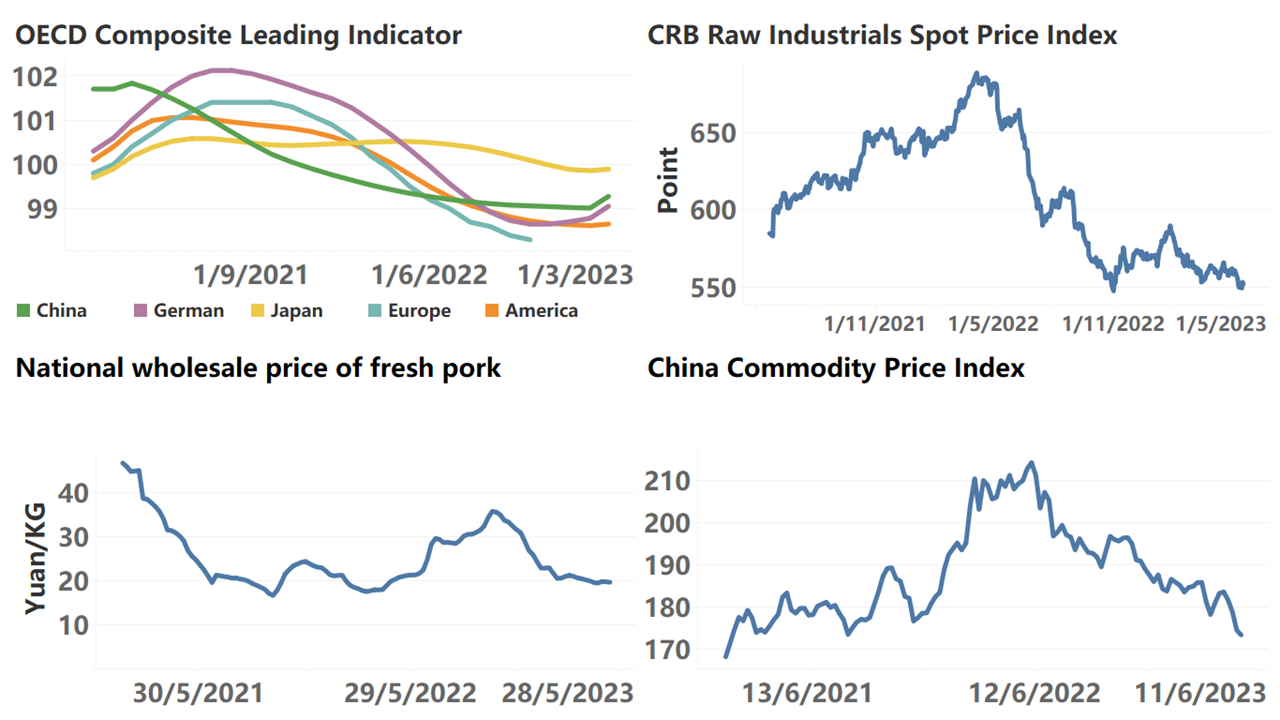

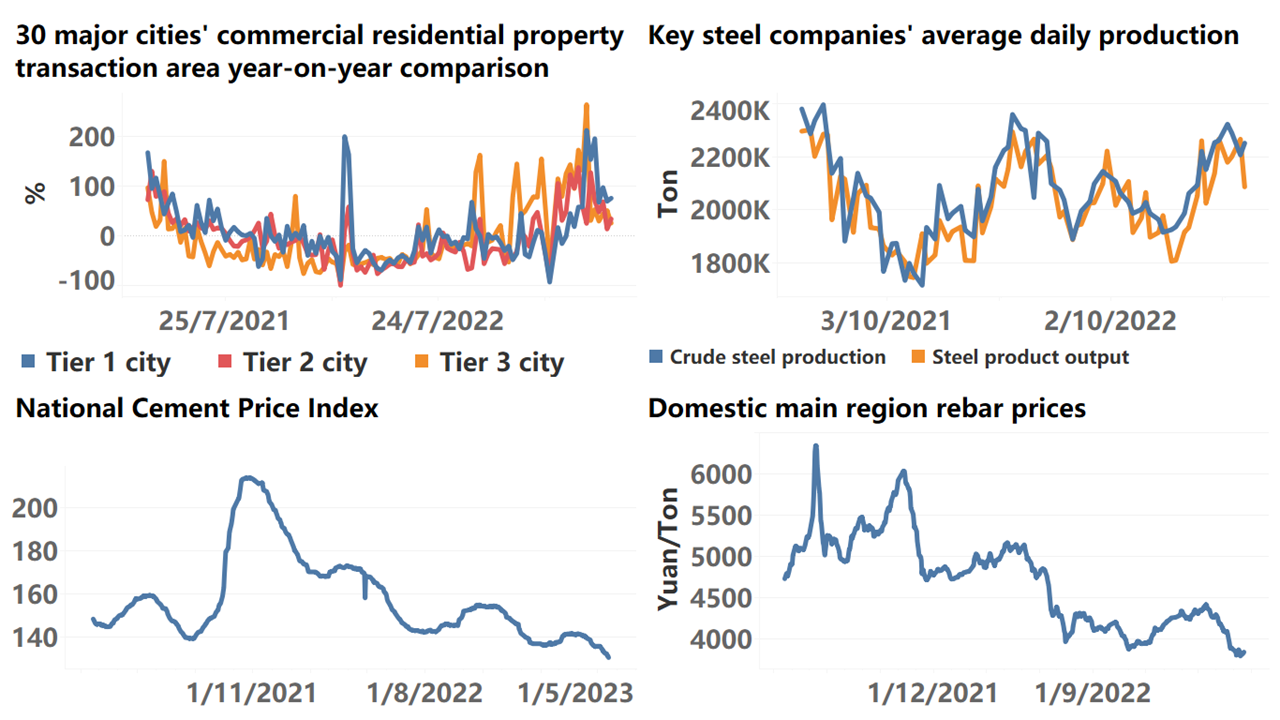

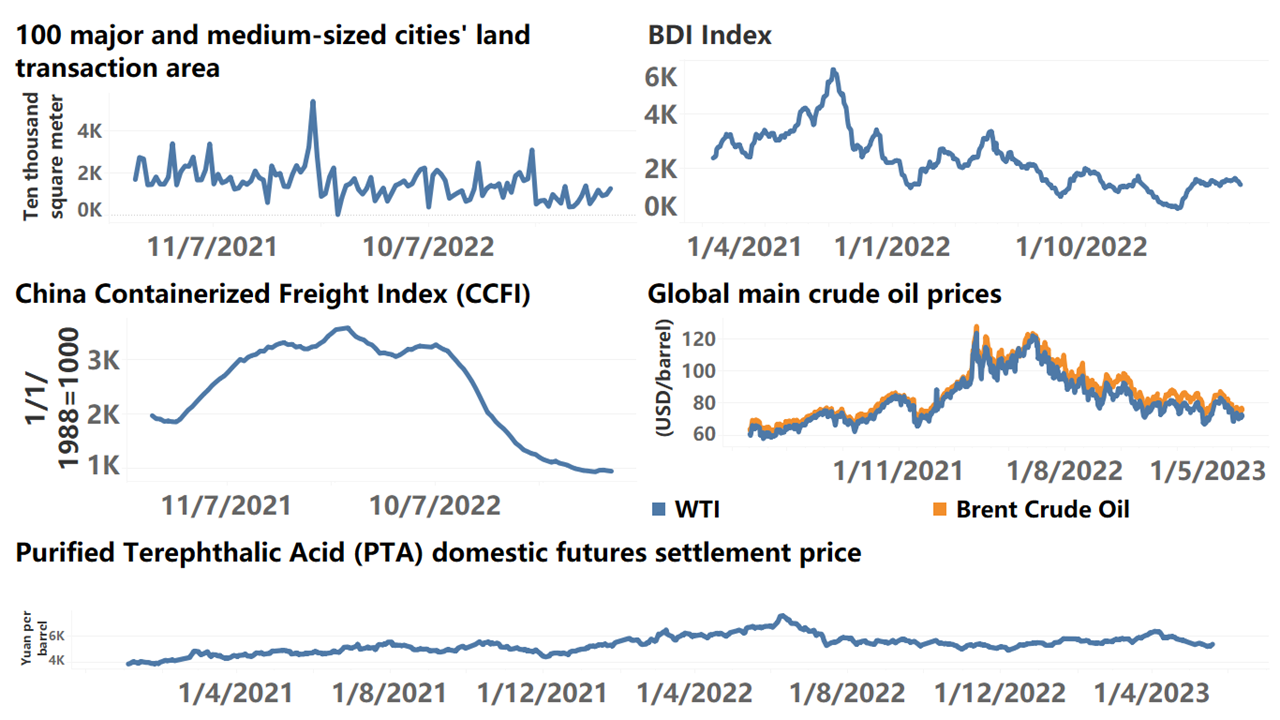

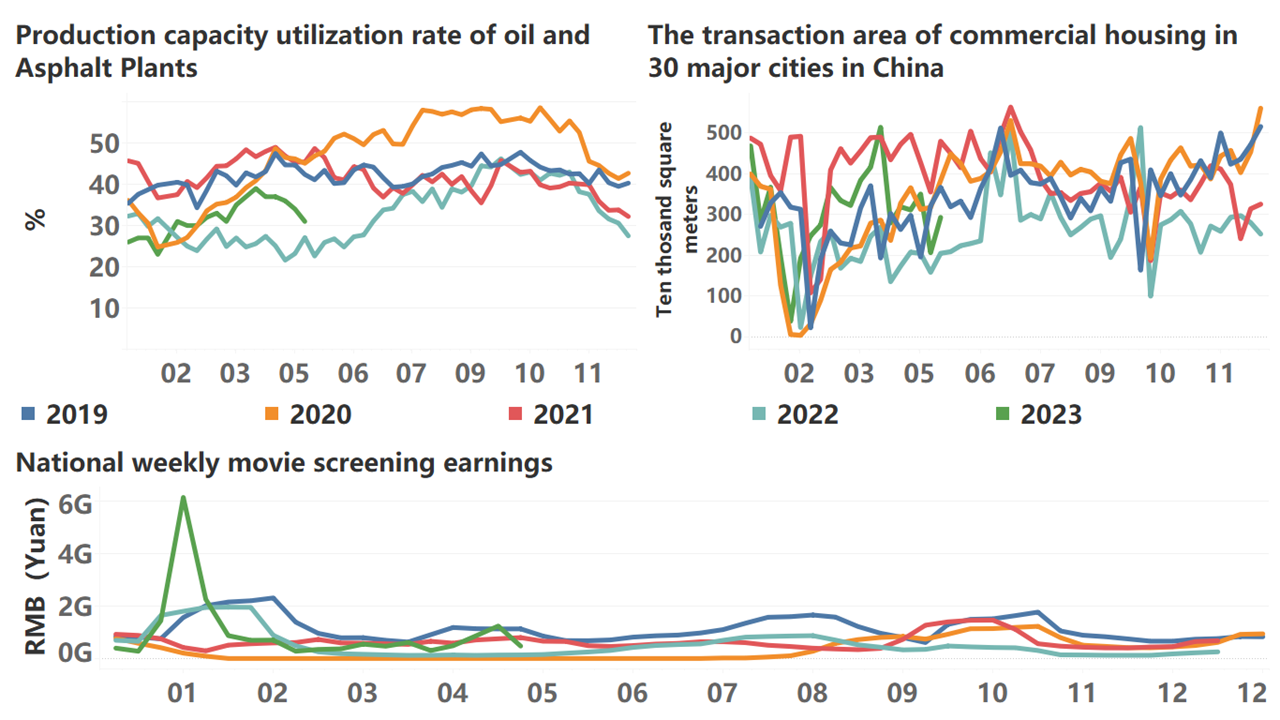

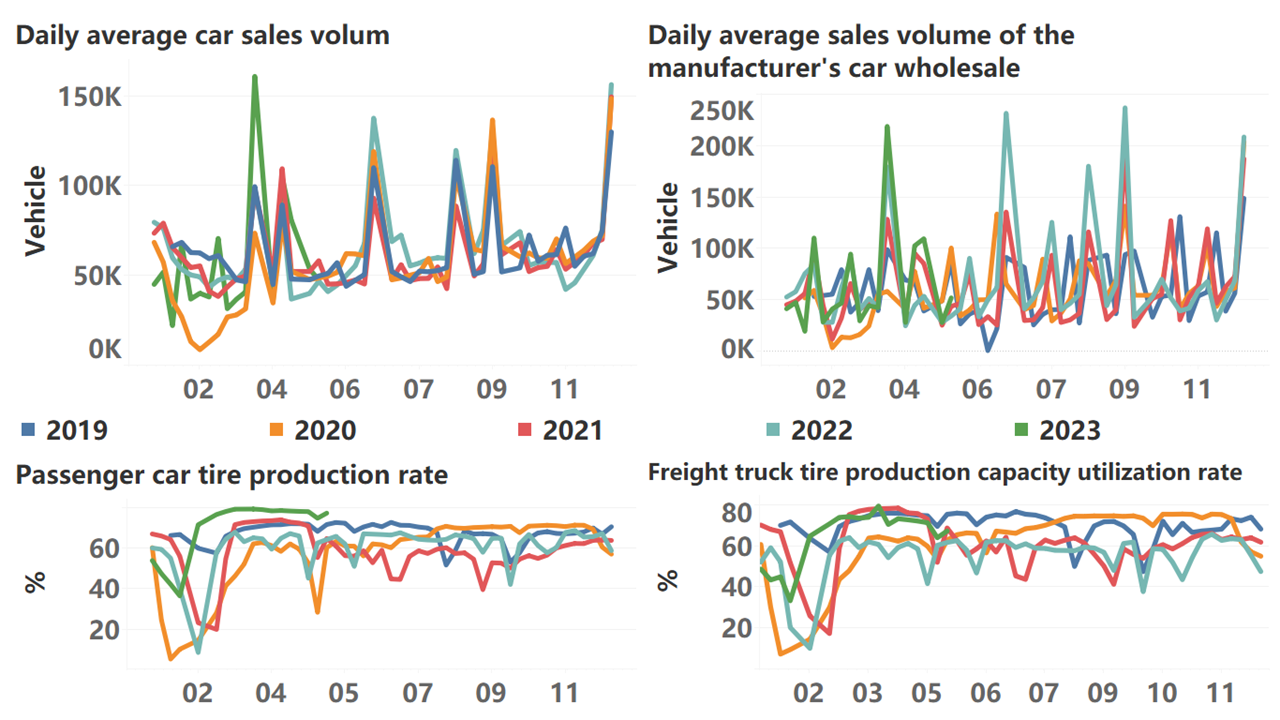

Below are the high-frequency data for this week:

*Translated by ChatGPT