Last week, most markets, excluding China, maintained a bullish trend. The Nasdaq is nearing its July high, and the cryptocurrency market has recently seen a rebound. In contrast, A-shares opened higher after the National Day holiday but then pulled back and remained volatile. Currently, market participants are reaching a consensus on the near-term direction, and the sentiment appears to be tilting toward the bulls. The U.S. CPI data released on Thursday exceeded expectations, while initial jobless claims also came in higher than forecast. Although these factors would typically be seen as bearish, they had little impact on the markets, with the Nasdaq and cryptocurrencies continuing their rally. This can be attributed to two factors: first, the CPI exceeded expectations by just 0.1 percentage points, which is within the market’s tolerance; second, market participants seem to be aligning on a consensus about future trends.

Looking ahead, there are three key themes driving market dynamics: the U.S. economy and presidential election, Middle East conflict risks, and the final strength of China’s economic policies. Each of these factors, individually or in combination, could lead to vastly different outcomes for global asset prices. From the current macro data, a soft landing for the U.S. economy appears increasingly likely. According to Polymarket, the probability of a Trump victory is rising, now at 54.8%, while Harris’ chances have fallen to 44.9%. The market has already factored in the economic policies and governing priorities of both candidates, so the focus now is on who will ultimately win the election.

The risk of conflict in the Middle East remains high, but its market impact seems to be diminishing. When news first broke of tensions between Iran and Israel in April, both cryptocurrencies and U.S. stocks experienced sharp declines. However, the missile attacks in October seem to have had little effect on the markets. It appears that investors are growing weary of this news cycle, and unless there is a significant escalation, the risks associated with the Middle East may gradually fade from the forefront.

Initially, there were high hopes that China would introduce substantial economic stimulus this year. However, Tuesday’s NDRC meeting cooled investor expectations, leading to a halt in the rapid rise of the market. On Saturday, the Ministry of Finance meeting reignited some optimism, though its ambiguous messaging left investors interpreting it through the lens of their positions. Bullish investors viewed the statements as unexpectedly positive, while bearish or sidelined investors remained skeptical. Post-market trading activity in U.S. stocks reflected this sentiment, as YINN (a triple-leveraged ETF tracking the FTSE China A50 Index) surged during after-hours and night sessions. This suggests either widespread optimism or some investors acting on advance information. We believe that, regardless of whether Saturday’s press conference meets or exceeds expectations, it is unlikely to disappoint. As a result, short-term market support is expected, and the battle to defend the 3,000-point level in A-shares will likely not occur soon. We anticipate that the current price levels will form a temporary bottom ahead of the National People’s Congress at the end of October.

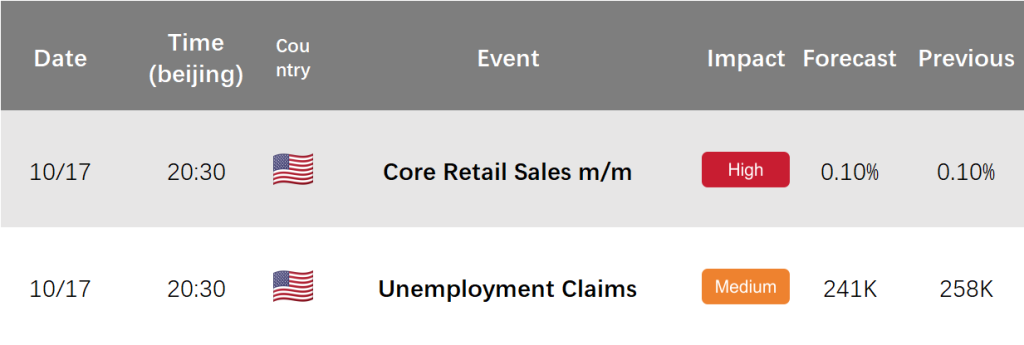

This week is relatively light on macroeconomic data. The most notable release is U.S. retail sales for September, with a forecast of 0.1%, matching the previous month’s figure. This is a key indicator of U.S. economic strength, and we expect it to remain in growth territory, in line with expectations. Unless this data significantly deviates from forecasts, the market is unlikely to revive concerns about recession risks in the U.S. Also of note is the weekly initial jobless claims data, which last week came in well above expectations, indicating a rise in unemployment. If this trend continues, the risk of a U.S. recession may resurface. However, at present, there is no need to turn bearish based on one or two isolated data points, though caution is still warranted.

Overall, the U.S. stock market remains relatively stable, with no clear bearish signals. The U.S. election could lead to structural market impacts due to policy differences between the candidates. Meanwhile, the risk of war appears contained, with any potential escalation likely delayed until after the U.S. election. Chinese assets, having transitioned from an emotional rally to a phase of consolidation, are poised for potential further gains. We remain cautiously bullish on global equity markets.