The past week was relatively uneventful. Both U.S. equities and cryptocurrencies remained in a broad consolidation phase, characterized by alternating gains and losses with rapid directional shifts. Despite numerous data points indicating that the U.S. is not in a recession and that the economy is gradually moving into its long-term potential growth range, equity markets did not show a significant upward trend.

According to the efficient market hypothesis, if the market has not experienced a serious malfunction, it means that the expectations for rate cuts and the absence of a recession have already been priced in. While we continue to hold a bullish stance ahead of the Federal Reserve’s rate cut announcement, it is evident that the market has already priced in a 25 basis point rate cut in September. The recession trade is nearing its end, so last week’s favorable data only managed to keep prices elevated rather than push them higher. For further price appreciation, we would need to see data that exceeds expectations, such as a 50 basis point rate cut in September instead of the anticipated 25 basis points.

Currently, there is significant divergence in market outlooks, with bulls and bears evenly matched and no clear dominant force. Bears have multiple reasons for caution, most notably the severe pullbacks in equity markets around previous rate cuts, such as those in 2020, 2008, and before 2000. Bulls, on the other hand, argue that the macro environment is overwhelmingly positive, leaving little reason for a bearish outlook.

Given the current information, we are siding with the bulls. While it is common to look to history for answers in times of uncertainty, we must be cautious not to rely too heavily on past patterns. History often repeats itself with different nuances. The large pullbacks following previous rate cuts were driven by significant economic recessions or black swan events, neither of which are evident at present. Therefore, there is no compelling reason to adopt a bearish stance, and we remain cautiously optimistic.

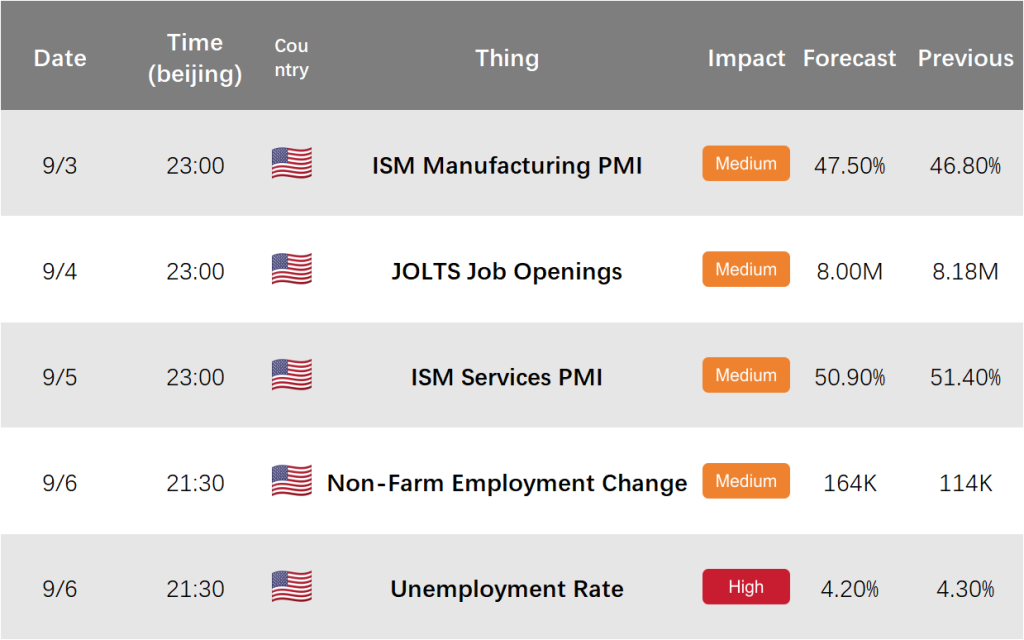

Next week’s data will primarily focus on the state of the economy, with PMI and unemployment figures providing insights into whether there is any underlying recession risk in the U.S. However, given that most of the no-recession scenario has already been priced in by investors, data that either exceeds or falls short of expectations could have a significant impact on the market, especially if it underperforms. Investors are primarily concerned with two issues: recession and rate cuts. This week, five key data points will reflect the current strength of the U.S. economy and warrant close attention.

On September 3 and September 5, the ISM Manufacturing PMI and Non-Manufacturing PMI will be released, respectively. These two sets of data will provide a direct view of the current U.S. economic situation. Based on previous economic data, we believe the U.S. economy continues to exhibit a slowdown in manufacturing and expansion in the service sector. This suggests that the manufacturing PMI may fall short of expectations, while the services PMI may exceed them, thereby offsetting market concerns. Following these are the JOLTs Job Openings and ADP Employment Change data on the evenings of September 4 and September 6, along with the U.S. unemployment rate for August. The market generally expects further improvement in unemployment, with a decline in the unemployment rate, an increase in ADP employment, and a decrease in job openings. We anticipate that the economic data will largely meet expectations, with no significant bearish or bullish surprises.

Overall, there is currently significant divergence in market outlooks. In the coming period, it will be crucial to monitor for any potential black swan events and the outcome of the September FOMC meeting rate decision, which is the most critical factor at this time.