In our shared professional experience, we have been involved in applying deep learning to economic research, fortunate to be among the first in the country to explore this combination. Since the rise of ChatGPT in 2022, the core position of artificial intelligence in the Fourth Industrial Revolution has gradually been recognized. From an economic theory perspective, econometric VAR models and macroeconomic DSGE models effectively address some macroeconomic data issues, but they do not perform well with financial data. Neural networks, however, seem inherently suited for these complex relationships. Exploring neural network architectures compatible with financial data is an intriguing endeavor.

In our actual work, we study macroeconomic data and observe asset price trends, trying to understand the relationship between the two. Macroeconomic data involve various aspects and are influenced by many unexpected events. Sometimes, we even need to rely on asset prices to gauge the impact of events on the macroeconomy. In such cases, it’s impossible to outsmart the market or fully comprehend global macroeconomic trends. Predicting macroeconomic events we have not experienced is very challenging.

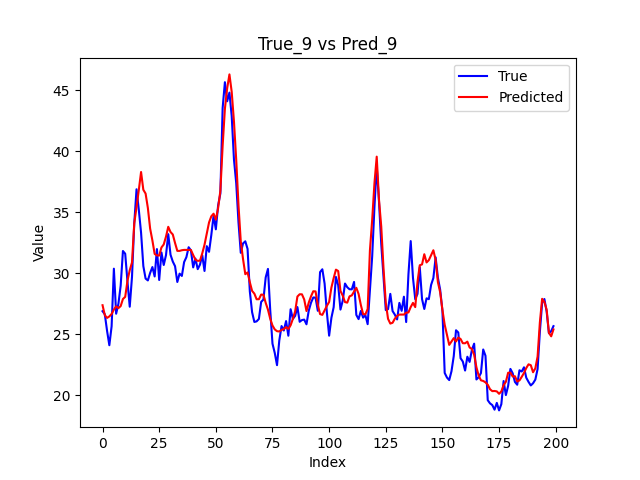

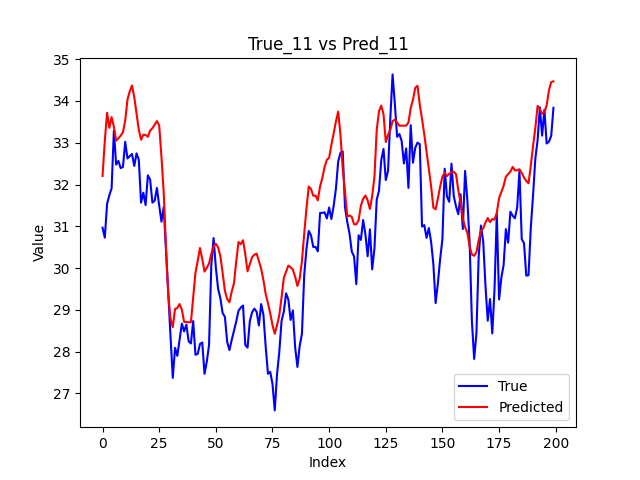

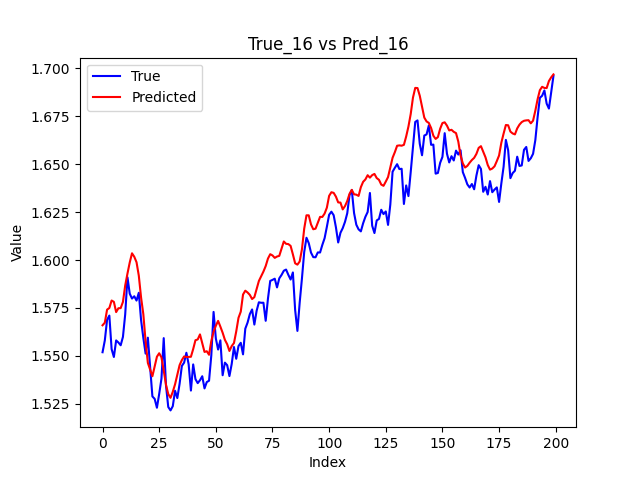

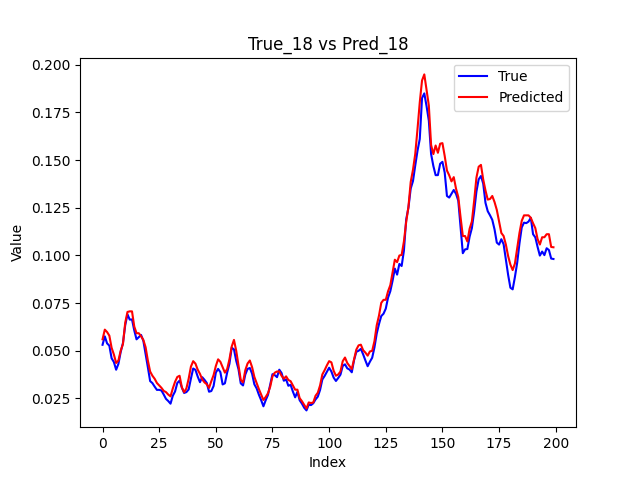

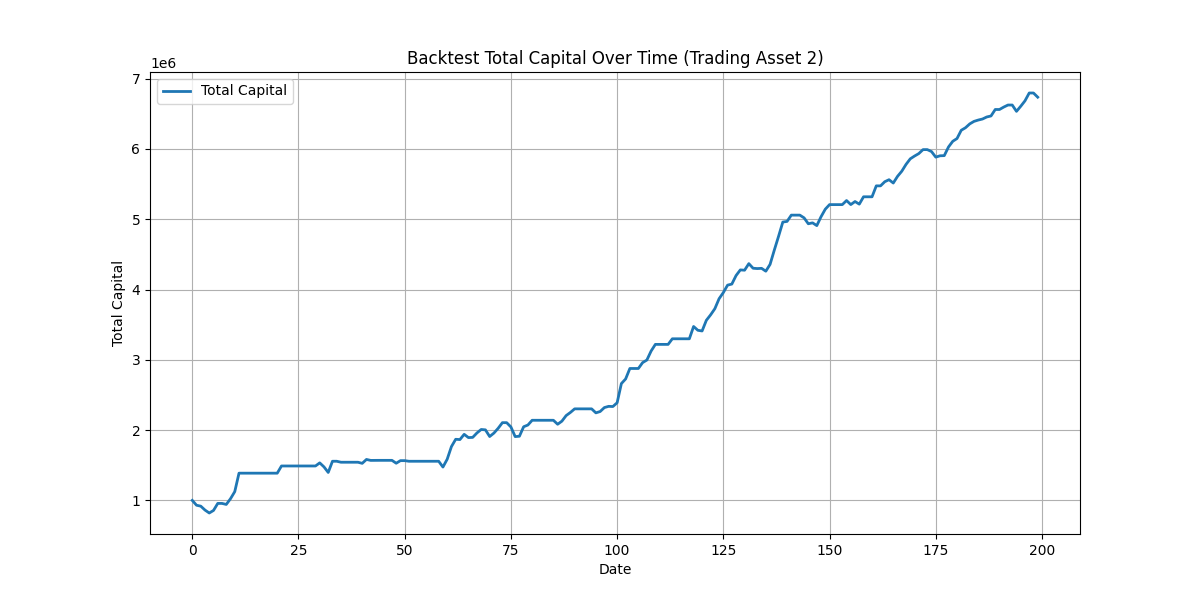

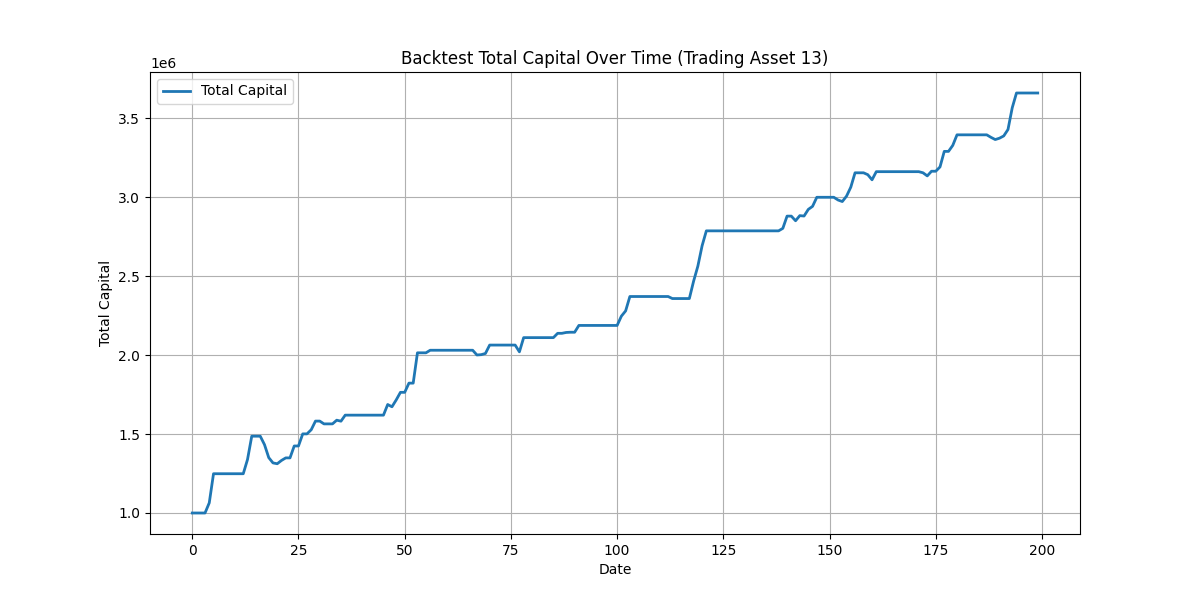

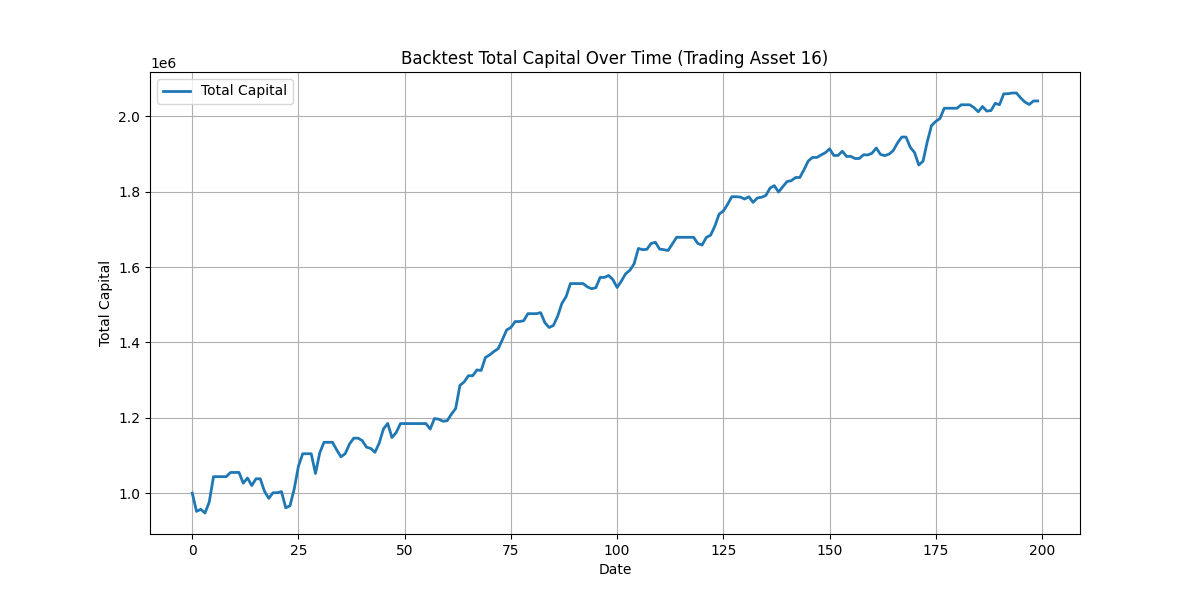

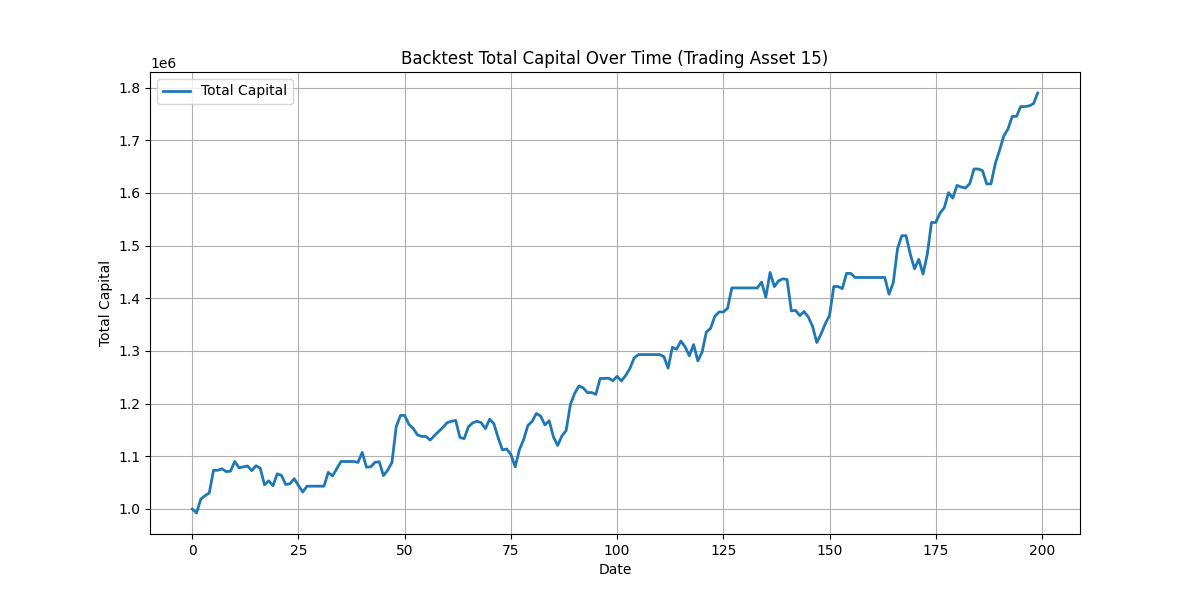

We believe that all information is reflected in prices, and all analysis lags behind prices. Extracting information directly from the prices of 27 major global assets is more efficient and direct. Since early 2023, we have been focusing on deep learning and asset prices, experiencing several iterations, and have achieved some preliminary results. Below are the backtesting curves of some of the 27 assets over 200 trading days and the yield curves under a few simple trading strategies.

Our view on deep learning is that a good architecture can solve many problems. Suitable architecture, lower computational power, and stronger asset inclusivity are crucial for us in making short-term predictions. Whether deep learning can effectively identify sudden events still needs further testing in practice. Moving forward, we will continue to refine the model and, when appropriate, gradually share our model’s perspectives on the future prices of 27 major global assets.