United States

This week, the U.S. October Consumer Price Index (CPI) recorded a 3.2% increase, down 0.5 percentage points from a 3.7% year-on-year increase in September, exceeding market expectations. Following the release of the U.S. CPI data, the probability of the Federal Reserve raising interest rates by 25 basis points in December has become extremely low according to the CME. There is now even a view in the market that interest rates might start decreasing as early as June next year. The expectation is that the interest rate decision has been set and will be maintained for six months. Federal Reserve Chairman Jerome Powell, in a press conference, acknowledged risks to the U.S. economy including a potential government shutdown and the Israel-Palestine conflict, but he clearly stated that these risks are not yet severe enough to have a fatal impact on the U.S. economy. When asked about the possibility of financial institutions facing debt issues in the next six months, Powell expressed confidence that issues like those faced by Silicon Valley Bank are unlikely to recur. Overall, the current economic progress suggests that U.S. interest rates are indeed having a restrictive impact on the economy.

Market reports indicate that Citibank is planning to cut its workforce by 10%. Over the past 15 days, including last week and the week before, the NASDAQ has continuously risen, reaching levels comparable to previous highs. It seems the market has already digested this round of news. Our earlier assessment was that the NASDAQ would fluctuate narrowly, but the volatility in the past month reached 14%. During this period, the entire crude oil market’s prices have been falling steadily, virtually eliminating the risk of imported inflation. The U.S. dollar index has also fallen to around 104, indicating a return of global monetary liquidity. In the Asian market, the Nikkei has followed the NASDAQ, showing strong performance, while the Hang Seng Index has been weak, mainly due to the slow recovery of Mainland China’s economy.

Regarding the NASDAQ, considering the rapid decline in oil prices and a 0.1% month-on-month decrease in October retail sales, we suggest gradually buying into the NASDAQ in small increments. For the Nikkei, the market continues to anticipate an interest rate hike by the Bank of Japan, and Japan’s CPI is still on an upward trend. However, an interest rate hike is unlikely in the next 1-2 months and should at least wait until Japan’s fourth-quarter data is released.

China

This week, overall economic data for October was released, showing insufficient domestic demand. The two-year average growth rate of retail sales was around 3.6%, which is not ideal. Given last year’s low base, data for November and December is expected to remain high, but the importance of the two-year average growth rate should be emphasized. From October’s PMI to CPI data, the figures have shown disappointing trends. During a press conference, the National Bureau of Statistics mentioned that some sub-indexes of the PMI are still in the expansion zone. However, upon close examination, these figures are still not ideal compared to previous years. Especially in October, real estate prices almost universally showed month-on-month declines, marking the end of the traditionally strong September and October sales period. Market information has highlighted that companies like Tencent and Alibaba have net profit margins of 20%, indicating significant workforce optimization. The actual situation of the real economy is quite complex. However, the Chinese stock market performed relatively well this week, with the central bank injecting a large amount of short-term liquidity. But currently, there are no fundamental conditions for a significant rise in the China A-share market.

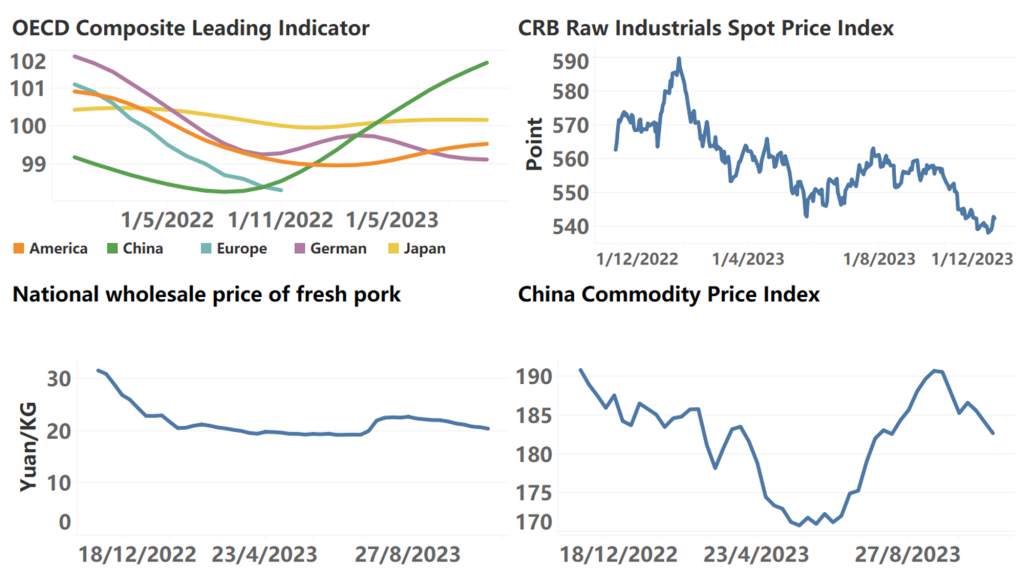

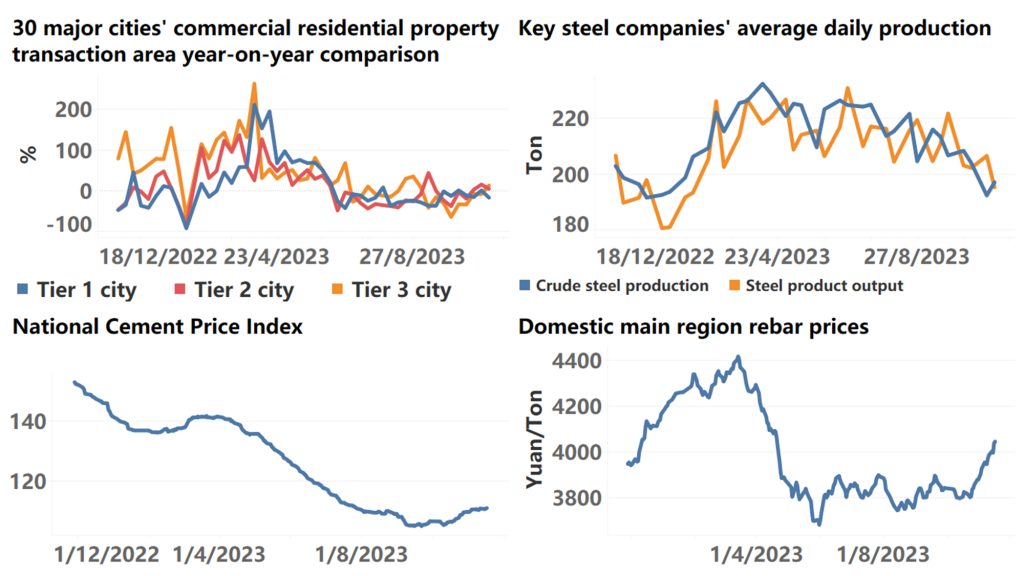

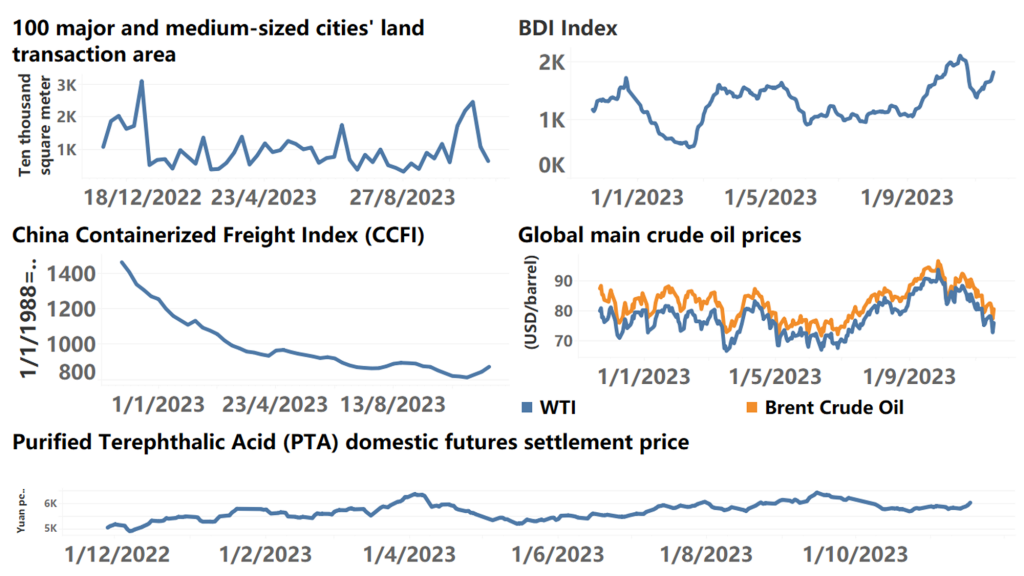

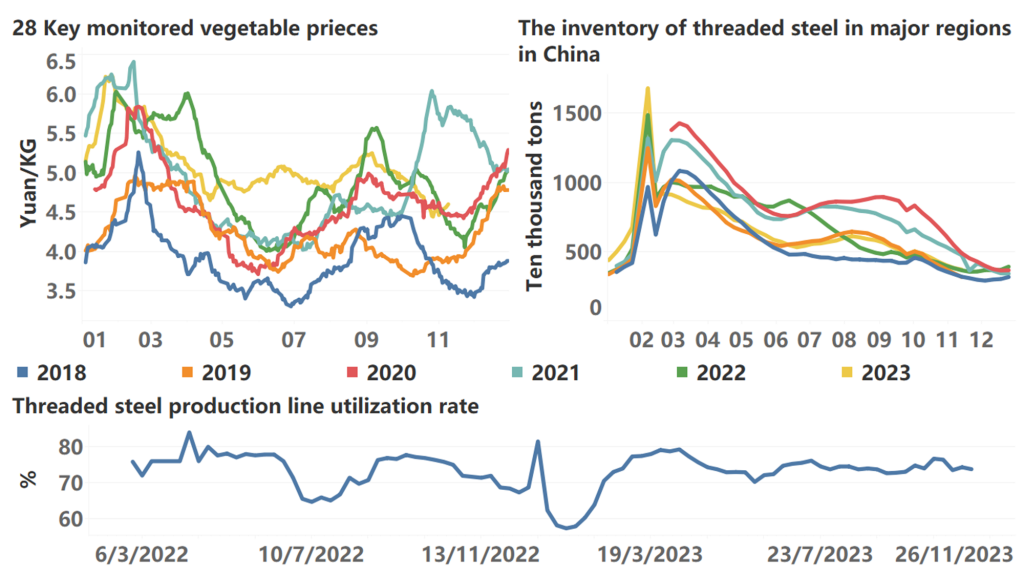

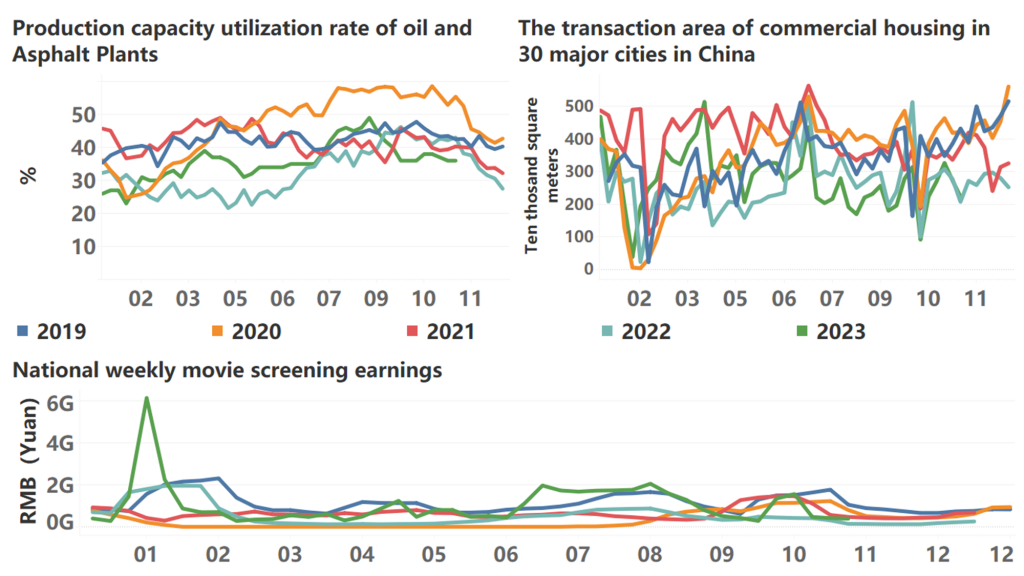

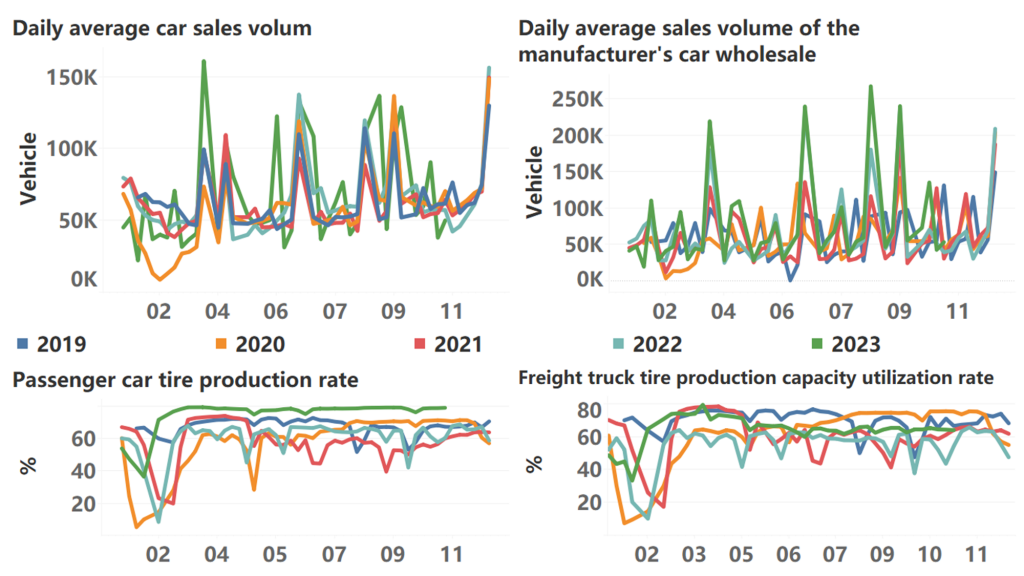

The following are high-frequency data for this week:

*Translated by ChatGPT