Our Mistake

In this round, we erroneously judged the trend of global asset prices, with incorrect assessments of the U.S. Dollar Index and the ten-year Treasury yield being the primary factors. Earlier, we believed that the yield on the U.S. ten-year Treasury would continue to rise due to the strong growth of the U.S. economy. In analyzing the process of the ten-year Treasury yield reaching 5%, we identified two factors: one was the excessive short-term Treasury supply, and the other was the robust growth of the U.S. economy. We realized that the short-term supply did indeed impact the ten-year Treasury yield, but due to the disruption of U.S. Q3 GDP data, we did not anticipate the yield to fall back quickly. Purely from an economic theory perspective, with short-term rates at 5.25%-5.5%, an inflation rate of 3.7%, and a growth rate of 4.9%, resulting in a positive real interest rate, this would indeed suppress the pace of economic expansion. A growth rate of 4.9% is still too high, and Powell’s stance is that the Federal Reserve will continue to raise rates if necessary, but this week’s market overall remains optimistic.

The performance of oil prices this week also increased everyone’s expectations. Brent crude returned to $81, and WTI fell to around $75. There are two possible reasons for this price fall: first, the risk of the Israeli-Palestinian conflict did not spill over, and second, there was no significant increase in global energy demand. The fall in energy prices has alleviated the risk of recession in the global economy, especially in the Eurozone, supporting a rise in securities prices.

In China, the October CPI year-on-year was -0.2%, mainly due to a significant drop in food prices. Domestic demand in the economy remains insufficient, consistent with the overall PPI. This week, the A-share index showed an upward trend, which seems inconsistent with the overall economic trend, but it exhibited a technical correction.

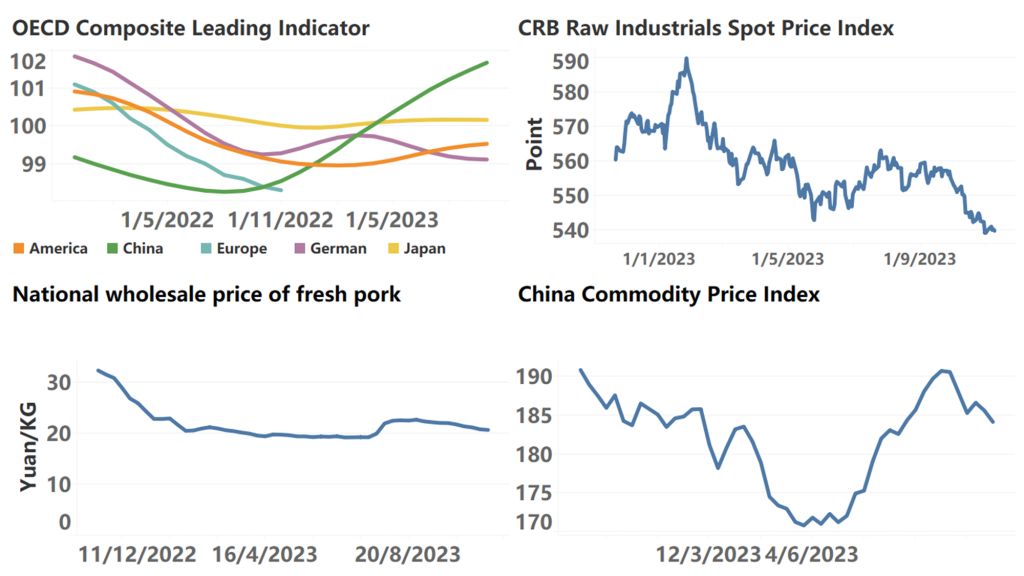

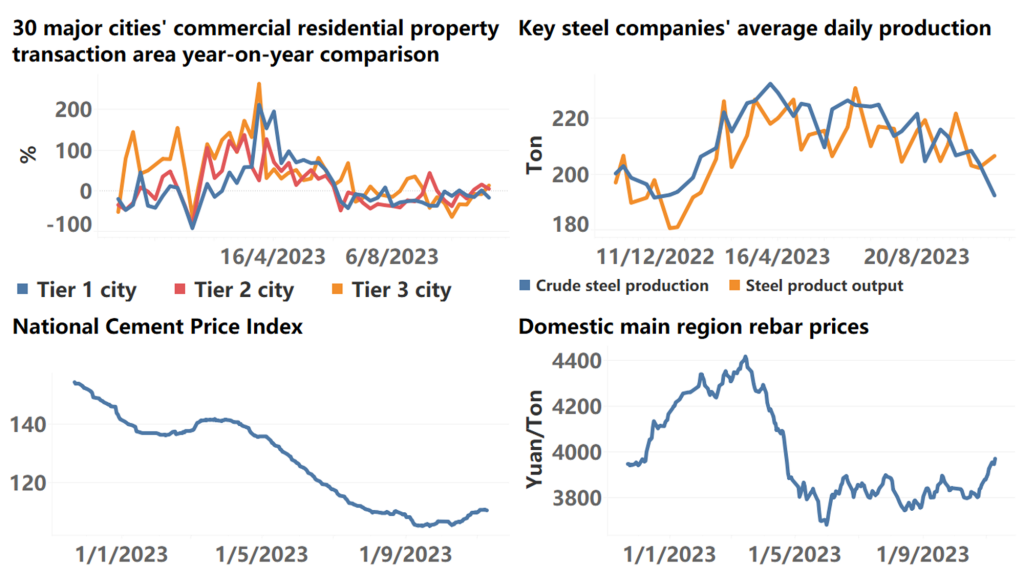

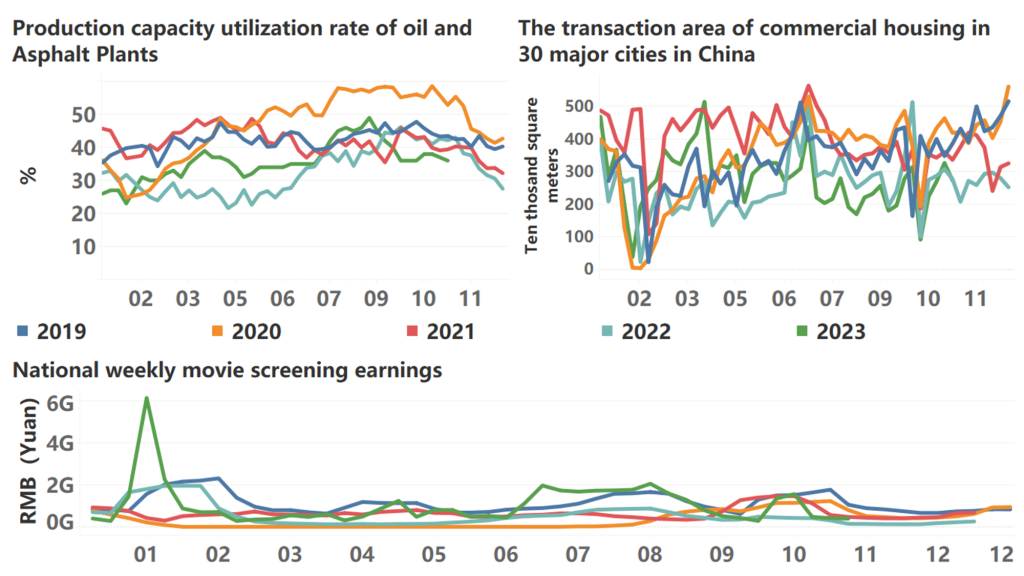

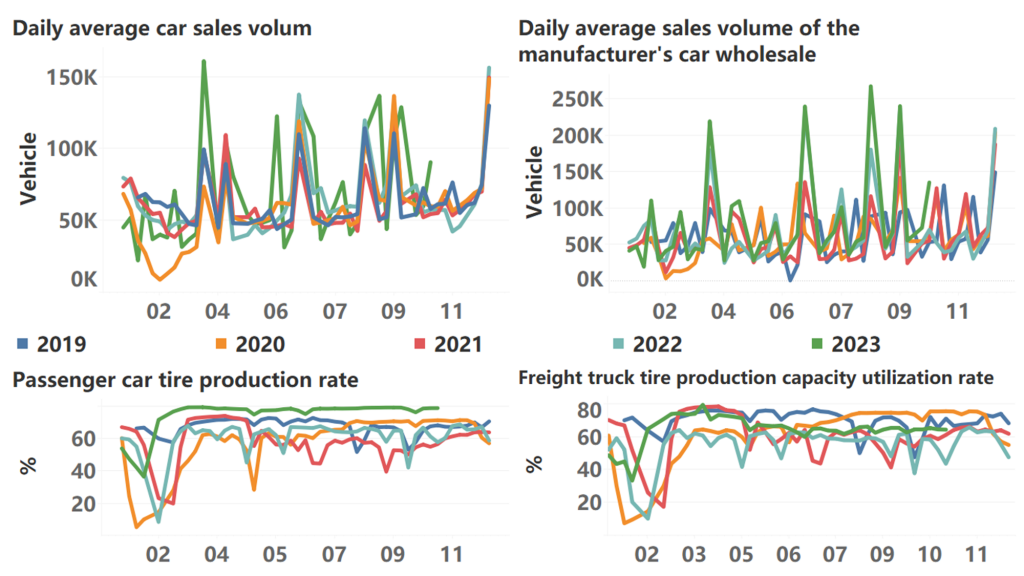

The following are high-frequency data for this week:

*Translated by ChatGPT