Current Fiscal Outlook : In 2025, we estimate the fiscal deficit rate may reach 4.5%, including the issuance of ultra-long-term government bonds, primarily driven by the anticipated issuance of ¥2 trillion in special government bonds.

The current fiscal landscape is shaped by two main factors:

- A significant decline in land finance, leading to a revenue cliff.

- The maturity of substantial prior debts, marking the peak of a credit cycle.

Interest payments on government debt have reached nearly ¥1 trillion, equivalent to 0.8 percentage points of the fiscal deficit. The ideal solution to manage the credit cycle would be robust economic growth and corporate profitability, yet such opportunities remain limited. Consequently, refinancing to lower funding costs and extend debt maturity is essential to alleviate the annual fiscal pressure from interest payments.

In November, the National People’s Congress approved ¥6 trillion in implicit debt replacement quotas. Additionally, ¥800 billion from annual special bond allocations has been earmarked to address implicit debt, bringing the total to ¥10 trillion. This strategy effectively lengthens maturities and reduces capital costs.

Fiscal and government fund expenditures in 2024 notably fell short of budget targets, while revenue growth from taxes and land sales also declined significantly. These revenue trends will be critical reference points for fiscal policy space in 2025:

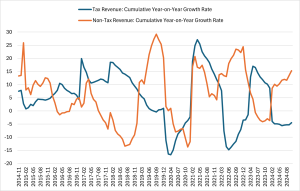

- Tax Revenue: By October 2024, cumulative tax revenue had fallen by 4.5%. Although monthly tax revenue turned positive in October, 2025 prospects remain uncertain. VAT, corporate income tax, and personal income tax—key pillars of China’s tax system—are unlikely to stabilize rapidly amid deflationary pressures.

- Land Revenue: This segment has seen a cumulative decline of 22.9%, exacerbating fiscal challenges.

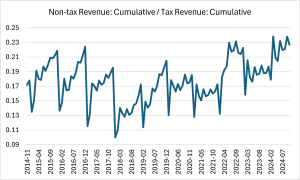

Meanwhile, rigid expenditures, such as debt interest payments (up 8.2% YoY) and social security spending (up 5.1% YoY), further constrain fiscal flexibility. Non-tax revenues, which exceeded ¥3.4 trillion by October 2024 with a YoY growth of 15.3%, have played a compensatory role but have also dampened market expectations in the private sector. Maintaining such high growth in 2025 seems unlikely, though non-tax revenues may still hover around ¥3 trillion. This figure is roughly three times the incremental funds from ultra-long-term special government bonds but offers limited sustainability, adversely impacting economic expectations.

Historically, non-tax revenues and tax revenues have demonstrated substitution effects, but their ratio hit a record high in 2024. Consequently, pressure has shifted to central fiscal deficits. The 2024 central fiscal deficit reached ¥4.06 trillion. In 2025, even without special government bonds, an additional ¥1 trillion deficit space is feasible; with special bonds, the figure could rise to around ¥3 trillion.

In the short term, fiscal deficit flexibility appears considerable, as most debt maturities are three years away, creating a debt ceiling-free borrowing window. However, this raises a theoretical question: What does fiscal deficit monetization mean for an economy?

Economist Simon Kuznets famously categorized global economies into four groups: developed nations, developing nations, Japan, and Argentina. Fiscal deficit monetization has been widely applied across these categories, with the following outcomes:

- United States: The U.S., supported by its trade deficit and the dollar’s status as the world’s reserve currency, has effectively leveraged fiscal deficit monetization to sustain economic efficiency. However, under Trump’s fiscal discipline policies, the U.S. began reversing this approach, reducing deficits and abandoning deficit monetization.

- Japan: Japan, with a massive fiscal surplus, used overseas income to stabilize its exchange rate and maintain economic balance. However, domestic economic vitality has suffered, with GDP per capita consistently declining relative to global levels.

- Argentina: Lacking trade surpluses, Argentina’s fiscal deficit monetization resulted in runaway inflation and economic chaos.

China, as a major trade surplus economy, faces unique constraints. Its surplus is heavily concentrated in Western markets, making it more vulnerable to potential disruptions, particularly under renewed U.S. protectionism or “Trump 2.0” scenarios. Trade negotiations could become increasingly limited, and the looming maturity of concentrated debts may lead to a fiscal cliff, posing significant risks.

China cannot directly emulate Japan’s fiscal strategies by citing debt-to-GDP ratios as evidence of ample fiscal space. Assertions that government debt is “owed to the people” are overly simplistic. Unlike Japan, China’s international environment is more challenging, requiring adherence to fiscal discipline to navigate external pressures.

A viable alternative lies in establishing an international RMB circulation system, combining trade deficits with financing initiatives under the Belt and Road Initiative and RCEP frameworks. Such a strategy could mitigate external shocks and foster sustainable fiscal resilience.