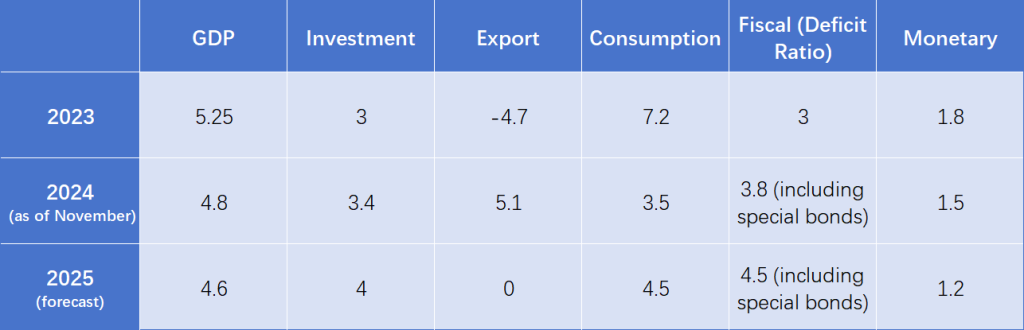

Our full-year GDP growth forecast for 2025 is 4.6%, primarily based on the economic trends observed in the third quarter of 2024. By the end of Q2 2024, cumulative year-on-year GDP growth reached 5%. However, starting in Q3, monetary policy was incrementally strengthened. In July, a special issuance of CNY 300 billion in ultra-long-term bonds was announced for “two new initiatives,” marking a mild stimulus phase for the economy. Fiscal policy during this period progressed steadily, leveraging the annual budget without significant additional measures. As a result, the Q3 year-on-year growth rate was 4.6%, serving as a benchmark for projecting 2025’s economic trajectory.

While Q4 2024 growth might reach 5.4%, allowing for the annual target to be met, this outcome hinges on multiple supportive factors: accelerated special bond investments, concentrated issuance of new debt restructuring funds, and export recovery. However, the stimulative effects of China’s recent policies typically sustain momentum for about two quarters. By mid-2025, these effects are expected to wane, exacerbated by worsening export conditions. Consequently, the 4.6% forecast is a conservative but realistic projection.

- lInvestment (4% growth): Achieving this target necessitates maintaining the pace of manufacturing investments. State-owned enterprises (SOEs) must continue increasing capital expenditure, focusing on investments in emerging technologies and equipment upgrades. A 10% contraction in real estate investment, while significant, remains manageable given the sector’s sustained scale—current completed and newly started construction areas total 1 billion square meters, against an estimated sustainable level of 600 million square meters annually. Infrastructure investment remains pivotal, with 2025’s special bond issuance projected to rise to CNY 4.5 trillion from 2024’s CNY 3.9 trillion. As of October 2024, infrastructure investment (excluding power) grew 4.3% year-on-year, while total infrastructure (including power) rose 9.35%. Investments in nuclear, wind, solar, and energy storage are expected to remain key growth areas.

- lExports (0% growth): Escalating trade tensions, such as the proposed increase in U.S. tariffs on Chinese goods from 19% to 60% under a potential Trump 2.0 administration, will weigh heavily on export performance. Drawing on the 2018-2020 trade war, these tariff hikes are likely to unfold over two years. Global retaliatory measures against a universal 10% U.S. tariff increase could create additional headwinds, making it challenging for China to maintain positive export growth in 2025. Proactive countermeasures, including enhanced trade negotiations with Belt and Road countries, RCEP members, and the EU, as well as expanded visa-free travel policies, signal China’s commitment to opening up, though the implementation speed and scale remain uncertain.

- lConsumption (4.5% growth): Supported by the CNY 300 billion ultra-long-term bonds, retail sales growth accelerated in 2024, but its sustainability warrants further observation. Expanding the funding scope and subsidy categories—potentially extending to services such as hotels and dining—could significantly boost consumption. Retail sales growth in October 2024 reached 4.8%, and with effective stimulus for dining consumption, achieving 4.5% annual growth appears feasible. From a policy perspective, consumption-driven investments yield higher leverage and immediate effects than infrastructure projects. However, challenges lie in funding mechanisms. While the central government could issue ultra-long-term special bonds, empowering local governments through accelerated reforms in consumption tax distribution could provide additional momentum. If these reforms succeed, retail sales data may see further improvement.