Last week proved to be a rollercoaster for the markets, starting with escalating tensions between Iran and Israel, followed by unexpectedly strong U.S. employment data that sent asset prices on a wild ride. High-leverage speculators faced repeated liquidations throughout the week. U.S. equity assets experienced a pattern of initial declines followed by recoveries, ultimately closing the week roughly at the same levels as they began. Crude oil prices surged rapidly, while gold continued its ascent to new highs. The Nasdaq and cryptocurrency markets remained in a state of high-level consolidation, showing no clear directional trends.

Currently, the market is focused on two key themes: interest rate cuts and recession risks, both of which are evolving in new directions. The recent non-farm payroll and unemployment data exceeded expectations across the board, significantly raising market anticipations of a slower pace for Federal Reserve interest rate cuts. The expectation of a 25 basis point cut in November has further solidified. The implications for the global market are twofold: first, the pace of liquidity release within the U.S. will decelerate, while the urgency for recession trades diminishes, collectively reinforcing expectations for a soft landing. In the absence of unforeseen events, this scenario is favorable for U.S. equities, characterized by a gradual, sustained upward trajectory without major pullbacks.

Second, the external environment for global assets, particularly the hot Chinese market, appears less optimistic than before. Whether the upward momentum can be maintained post-Golden Week remains uncertain; however, we believe it will continue for a while longer, as this rally largely reflects emotional sentiment and expected outcomes. If, as suggested by some research institutions, this rally is driven by retail investors, many may not fully account for subtle shifts in the overseas landscape. Thus, the momentum effect is likely to persist, as evidenced by the ongoing upward pressure in Hong Kong stocks. Conversely, if the rally has been propelled by foreign capital, it is probable that these investors have already begun to withdraw.

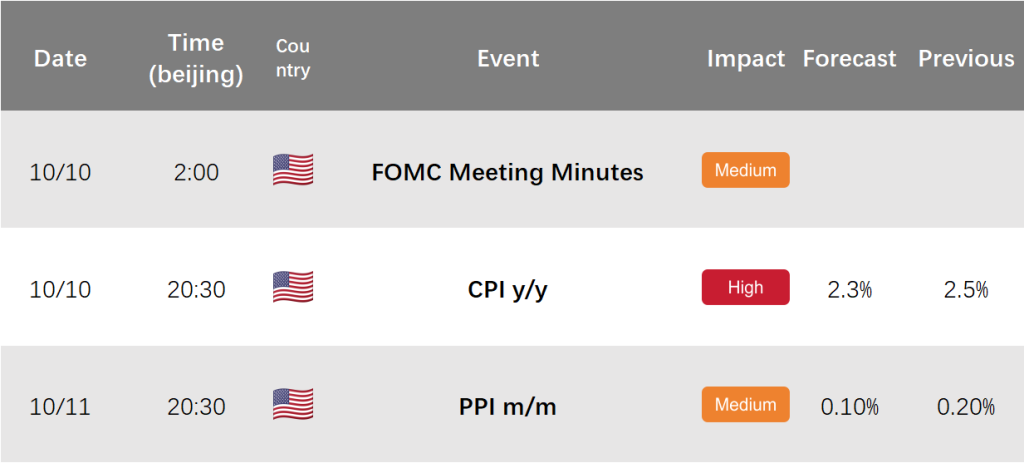

Next week features a macro data release cycle centered on price metrics. The impact of the FOMC meeting on the market is expected to be relatively limited, primarily inducing short-term volatility. Key attention will be paid to the CPI and PPI data, particularly the CPI, as it will significantly influence the Fed’s future rate-cutting path and corresponding asset price movements. Currently, the market’s critical pain point lies in liquidity, with recession risk no longer being the core concern. Therefore, a CPI reading below expectations would be considered a positive outcome, potentially accelerating the pace of rate cuts and enhancing the likelihood of more significant reductions later this year. Historical CPI data suggests that a rapid decline in CPI is plausible, reinforcing market expectations for future liquidity easing.

Overall, the market finds itself at a crossroads. U.S. equities and cryptocurrencies are still hovering at elevated levels, with black swan events, interest rate cut intensity, and recession risks remaining the primary battlegrounds for market participants. As attractive employment data diminishes recession fears, the focus will shift toward black swan events and the trajectory of rate cuts. We continue to hold our earlier view that, in the absence of any significant bearish news, a cautiously bullish stance remains warranted.