Last week marked a period of asset growth as the market increasingly tilted towards a 50bp rate cut from the Federal Reserve starting on Monday. By the eve of the rate decision, the odds had shifted to a 60:40 ratio in favor of a 50bp cut, aligning with our outlook from previous weeks. The FOMC meeting ultimately met our expectations, delivering an initial 50bp rate cut. According to the dot plot, only one committee member voted for a 25bp cut, while the majority supported a 50bp reduction, which significantly boosted market confidence, leading investors to anticipate an imminent soft landing and a substantial improvement in liquidity.

Following the announcement, the Nasdaq surged by as much as 3% in a single day. Tech stocks like TSMC posted similarly strong gains, with after-hours trading pushing the stock up more than 5%. The cryptocurrency market also rallied, with Bitcoin climbing over 5% and several altcoins posting gains of over 10%. Notably, the SUI/USDT pair stood out, rising more than 50% over the week and accumulating over 200% gains in nearly a month. The Bank of Japan also refrained from raising rates last Friday, which kept carry trades unaffected. Bitcoin responded with a 1% rise following the news, though U.S. equities did not follow suit, with the market closing slightly lower on Friday.

As we’ve emphasized before, no current macroeconomic data or events suggest a bearish outlook, so we maintain a cautiously bullish stance. However, it remains crucial to monitor the potential for black swan events or a recession in the U.S. economy. In the absence of either, we continue to recommend a cautious long strategy.

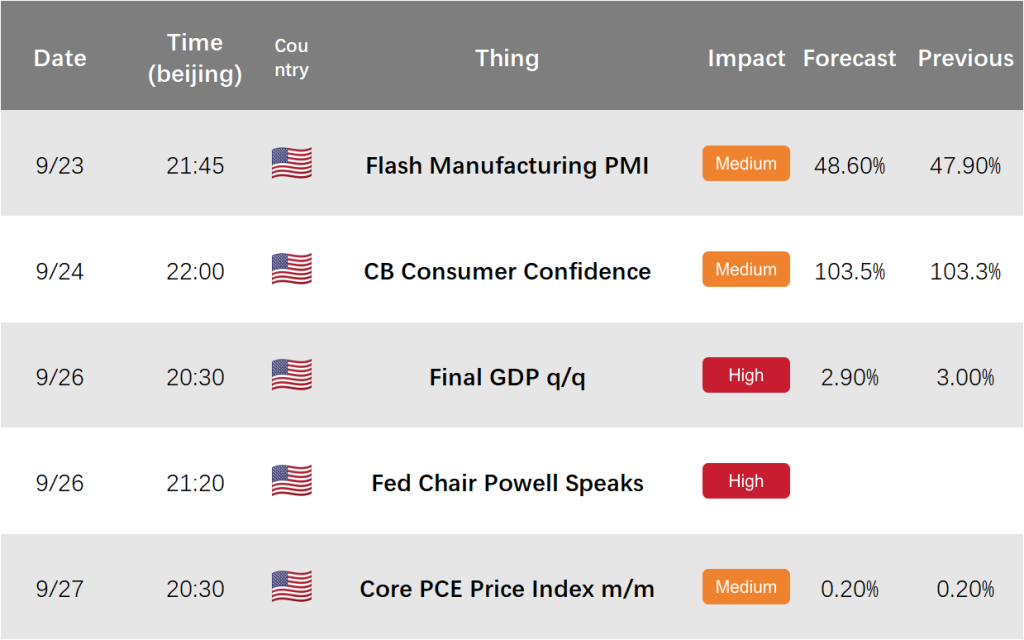

This week, the importance of economic data significantly increases, with key indicators from both the production and demand sides, alongside speeches from several Federal Reserve members. These developments are likely to drive substantial market volatility, and we lean towards going long on volatility. Production-side data to watch include manufacturing PMI and the final annualized Q2 GDP growth rate, both of which will provide a clear snapshot of the U.S. economy’s current state. As the rate-cut narrative gradually fades, recession risk remains the primary concern for traders, and any signs of recession will be closely scrutinized. We expect manufacturing PMI to fall short of expectations, while services PMI should continue to outperform, consistent with recent economic trends.

Regarding Q2 GDP growth, based on Jerome Powell’s comments during the FOMC meeting and recent economic data, we expect it to align with market forecasts. Core PCE inflation may not decline further, as previous data indicate that supply-side factors have created some inflationary stickiness, particularly in core inflation. We anticipate core PCE to meet expectations at 0.2%.

This week will also feature a series of speeches from Powell and several other Federal Reserve officials, which will likely introduce significant market volatility. We advise lowering leverage to minimize the risk of unnecessary losses. Historically, Fed officials tend to tighten the market when it performs well and provide reassurance during downturns. As such, the economic data from Monday and Tuesday will likely serve as a key reference for predicting the tone of these speeches, particularly from Powell. Considering last week’s market gains, it’s unlikely we will hear overtly bullish statements from the Fed this time.

In summary, we maintain our cautiously bullish outlook, believing that in the absence of black swan events or an economic downturn, the market will remain predominantly driven by long positions. We plan to hold our long positions through the U.S. presidential election.