Last week saw a broad market pullback. With U.S. markets closed on Monday due to a public holiday, trading resumed with a sharp retreat spurred by renewed expectations of a rate hike by the Bank of Japan. The Nasdaq dropped more than 2% in a single day and continued to consolidate throughout the week. On Friday, mixed U.S. employment data was released: the unemployment rate met expectations at 4.2%, but non-farm payrolls came in at 142,000, below the expected 164,000, with previous months’ figures revised down by a total of 80,000 jobs. Before the market opened, these figures were viewed as dovish, with pre-market Nasdaq futures recovering from a near 1% drop to slight gains. The cryptocurrency market saw broad gains, with Bitcoin rising more than 2% in the short term. However, within 30 minutes of the U.S. market opening, equities broadly declined, and investors flocked to low-risk fixed-income bonds. The underlying reasons for this shift are complex, leaving many investors puzzled by the sudden change.

The market’s reaction to the data underscores the extreme tug-of-war between bulls and bears, with participants deeply divided on the future direction of the market. Upon closer examination of the employment report and its revisions, many realized that the labor market might not be as strong as anticipated, causing the market to misfire once again, as prices failed to reflect reality in the short term.

Remarks by Federal Reserve member John Williams further contributed to the market’s decline. Williams emphasized a gradual approach to rate cuts, hinting at a 25-basis-point (bp) reduction rather than the 50bp many had hoped for. This set the stage for heightened anticipation around comments from Fed member Christopher Waller. The Nasdaq briefly rebounded following Waller’s remarks, in which he stated, “If appropriate, I would support a preemptive rate cut.” However, upon further scrutiny, particularly his comment that “the labor market is slowing but not deteriorating,” markets dipped again. The probability of a 50bp rate cut, as tracked by FedWatch, dropped from 57% at the time of the jobs report to an intraday low of 23%. Though this figure edged back up to 30% by September 8, it reflects the market’s diminished confidence in a larger cut.

In our view, despite the recent market pullback, this presents a clear buying opportunity. Over the past months, the Fed has consistently taken action to cool the markets when they perform well, yet has responded favorably when markets underperform. The flurry of comments from two key voting Fed members following the data release likely indicates a preparation for a 50bp cut at the upcoming FOMC meeting, which is a key reason for our bullish stance. Moreover, with unemployment falling, the “Sahm Rule” is no longer triggered, increasing the likelihood of a soft landing. We remain committed to holding a long position through the FOMC rate decision. A 25bp cut is already priced into the market, so even if this is the Fed’s final decision, the market should not see a significant further decline. However, if a 50bp cut materializes, the market would quickly erase Friday’s losses and enter a sustained upward trend.

In summary, we foresee two scenarios for the rate cut trade: First, a 25bp cut, which is the widely expected outcome and would not result in a significant market correction. Second, a 50bp cut, which would exceed expectations and undoubtedly boost the market. Based on current employment and price data, the Fed will likely be compelled to begin cutting rates in September, with only two scenarios—25bp or 50bp—remaining in play on FedWatch. Therefore, the possibility of no rate cut or even a rate hike is not part of our forecast.

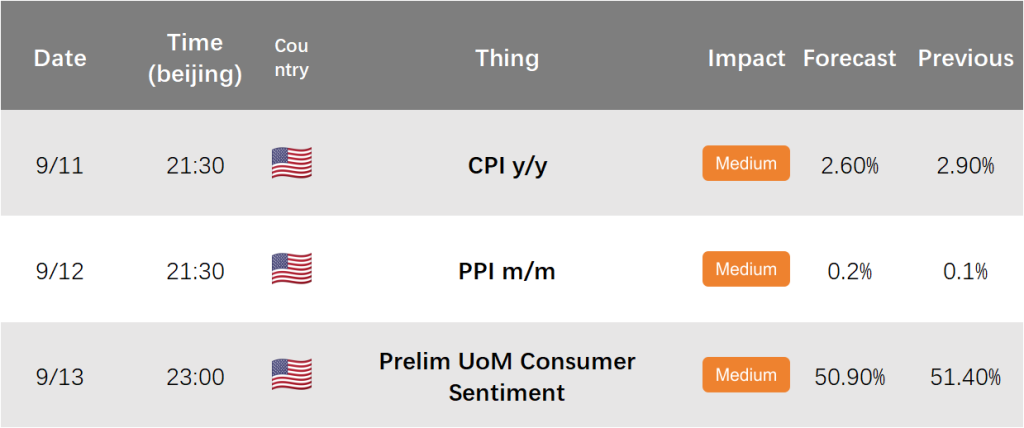

This week’s data holds slightly less importance. The key releases include price data (CPI and PPI) and the Consumer Confidence Index. The August CPI year-over-year will be released on the evening of September 11, with the market expecting 2.6%, down from the prior 2.9%. The PPI month-over-month, scheduled for September 12, is expected to come in at 0.2%, up from the prior 0.1%. CPI is the primary focus. If CPI meets or falls below expectations, it would further reinforce expectations for a Fed rate cut, with the strength of the data determining whether the cut will be 25bp or 50bp. For those seeking greater certainty before entering a long position based on a 50bp cut, it would be prudent to wait for the CPI release before making a move.

As for the Consumer Confidence Index, this will offer insights into the current state of the U.S. economy, providing a key basis for recessionary trades. If the data underperforms, recessionary concerns will linger. If the data meets or exceeds expectations, it will likely bolster the market. However, a significant upside surprise could reduce the likelihood of a 50bp rate cut, adding complexity to the data’s impact in this environment.

In conclusion, while last week’s market experienced significant pullbacks, we remain bullish leading up to the Fed’s policy meeting and are even willing to hold long positions through it. However, we must closely monitor this week’s price data, employment figures (such as initial jobless claims), and the Consumer Confidence Index to refine our trading strategy further.