Rate Cuts: What's Next?

Over the past few weeks, updates have been paused due to the CFA exam. Before diving into recent market trends, let’s revisit AI and its related investment opportunities.

During my CFA studies, I found ChatGPT to be far more practical than any textbook or course. Whether it’s tackling questions or understanding key concepts, it often provides answers within half a minute. It quickly identifies and corrects personal cognitive biases, making one wonder if purely lecture-based educators (those who merely read from textbooks and slides in university classrooms) might be the first to be replaced by AI.

On the other hand, popular domestic apps like Xiaoyuan Souti and Zuoyebang, which gained traction in previous years by hiring college students to answer questions and build a question bank, may find the value of these intangible assets drastically reduced—perhaps to less than 5% of their original worth—in the face of generative AI. Companies like these are likely to vanish soon.

From an investment perspective, similar overseas software includes Chegg, a publicly listed company that operates similarly to Xiaoyuan Souti. Its stock price peaked at $113 per share in early 2021, but with the onset of the current AI wave, its value has plummeted, dropping to $25 per share by the end of 2021 and down to just $2.22 per share today in 2024. This AI revolution has offered not only the opportunity to profit from Nvidia but also from shorting Chegg, provided one has sufficient imagination and logic.

Last week was favorable on the macro front. Although the manufacturing PMI fell short of expectations at just 48, the services PMI exceeded expectations, and the Fed has strongly hinted at upcoming rate cuts. Most FOMC members believe it’s time to cut rates—and quickly. This marks a new macroeconomic landscape: the recession has temporarily subsided, and liquidity is about to loosen.

This is an unequivocal positive. In a normally functioning economy, rate cuts will undoubtedly further drive up equities and commodity prices. On Friday, U.S. stocks, cryptocurrencies, and gold all rallied together, as if the recession fears and panic selling of the past two weeks had never happened. The momentum for unilateral gains remains intact.

Rate Cuts: What’s Next?

Historically, equity markets tend to pull back after rate cuts begin, as these cuts are usually a response to a recession. However, this cycle is different—the anticipated recession seems not to have materialized. So, can the rally continue without the need for prolonged corrections and consolidations?

We believe that, as of now, the outlook remains bullish through the end of 2024. A rate cut in a non-recessionary environment is the best-case scenario, and it will undoubtedly drive markets higher. The only question is whether a true recession might still occur. Based on current data, it hasn’t happened yet, but we must continue to monitor indicators of economic activity, such as PMI and retail sales.

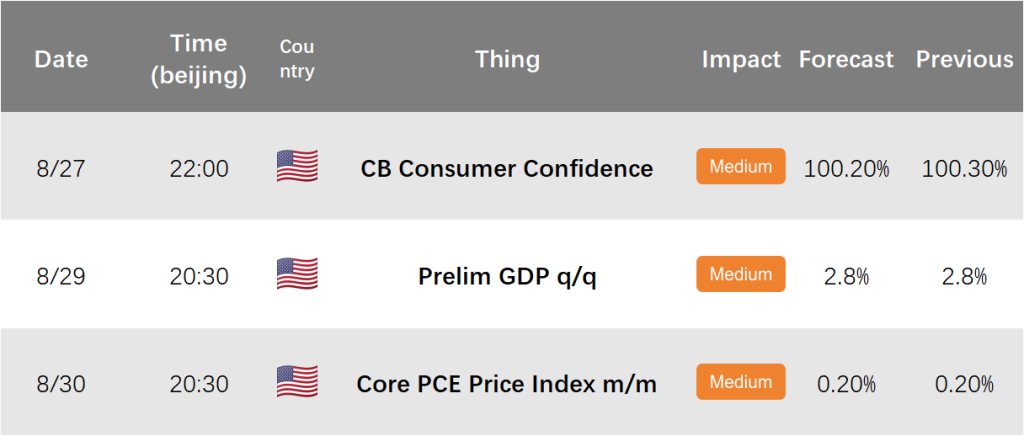

This week is relatively light on macro data. The first key release is the Conference Board Consumer Confidence Index on August 27 at 10:00 PM, with a forecast of 100.2, compared to the previous value of 100.3. The second is the revised annualized GDP growth rate for Q2, expected at 2.8%, unchanged from the prior estimate. While these data points reflect the current economic situation and are of limited importance, they are still worth watching as we exit the recession trade. Based on high-frequency economic data and U.S. monetary policy, we expect these figures to exceed expectations.

The third key data point is the core PCE, released on August 30 at 8:30 PM. The core PCE year-over-year rate has been steadily declining, with economic activity gradually cooling and converging toward its long-term potential growth level. We expect this data to come in below expectations, which could prompt the Fed to cut rates more aggressively—by 50 basis points instead of 25.

However, if this data declines too quickly, the potential for a recession may once again take center stage. Therefore, the best outcome for CPI data would be for it to meet expectations.

Overall, we will maintain a bullish outlook until the next FOMC meeting before considering a shift in strategy. The current macro environment does not present significant bearish signals, and the recession trade is gradually fading out, while the benefits of rate cuts are beginning to materialize. As such, we lean towards a bullish stance on equities, a positive outlook on bond prices, and a bearish view on Treasury yields.