Chinese Perspective: A Promising Start

On March 18, China disclosed its major macroeconomic data for January and February. Retail sales grew by 5.5% year-on-year, investment increased by 4.2%, industrial value added rose by 7%, while real estate sales fell by 29.3% and sales area dropped by 20.5% compared to the same period last year.

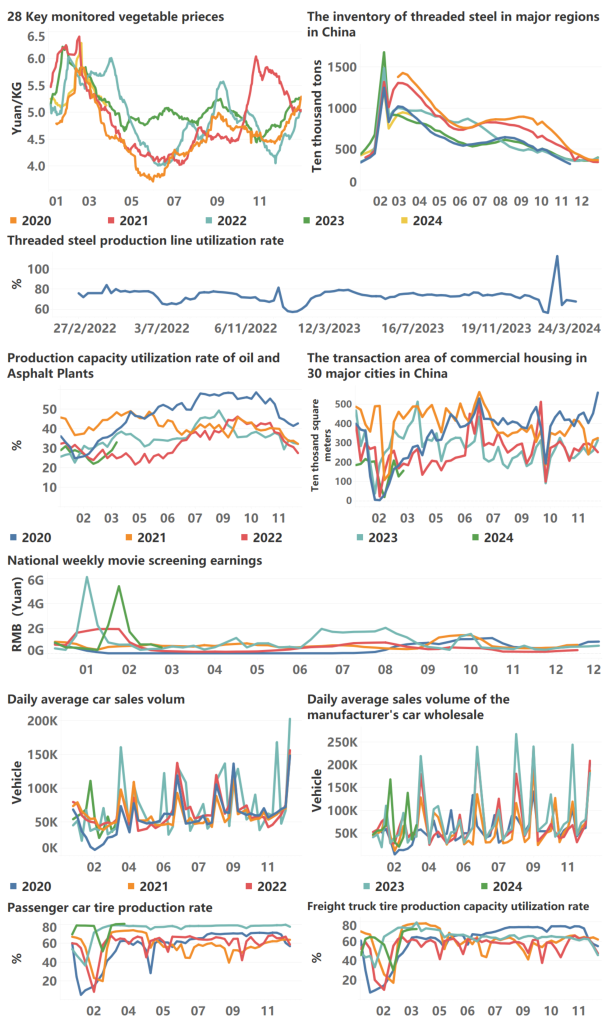

Overall, the economic growth pace in the first two months did not deviate from the annual target of 5%. Although there was a significant decline in sales area and sales value of newly constructed commercial housing, with real estate development investment dropping by 9% year-on-year, narrowing by 0.6 percentage points compared to the full year of 2023. From the perspective of investment driving force alone, the drag of real estate on the demand side of the economy did not significantly differ from the situation in 2023.

The 5.5% year-on-year growth in retail sales exceeded market expectations. Considering that in the fourth quarter of 2023, the two-year average growth rate was only 3%, rebounding to over 5% at the beginning of 2024 indicates a promising start. This is conducive to restoring confidence across various market sectors. Looking closely, the high level of consumption in catering services persists, while the growth rate of commodity consumption is declining. According to information from the China Association of Automobile Manufacturers, the year-on-year growth rate of retail sales of automobiles in March dropped to around 3%. There is a further downward trend in the growth rate of commodity consumption. It can be said that after experiencing this round of adjustment in the real estate sector, structural changes are emerging in the Chinese economy.

Household consumption, especially in catering and services, has performed exceptionally well, driving rapid recovery in profitability levels for industries such as travel and hospitality. We anticipate that in the upcoming overall economic growth, due to the sustained weakness in real estate prices, residents seem to be shifting towards spiritual consumption, not only pursuing consumption itself but also seeking personal spiritual enjoyment reflected through consumption.

Looking back at history, after the Great Depression, Japan’s economic bubble burst, and during Europe’s Renaissance period (inflation), there were social phenomena where young people shifted their focus from material consumption to spiritual aspects, accompanied by a rapid rise in individual liberalism. Among them, the book “On the Road” represented literature, while artists like Bob Marley and Patti Smith represented art.

Reviewing China, the Northeast’s tourism boom, Zibo barbecue, and Tianshui spicy hotpot may symbolize the beginning of a new consumption pattern. Moreover, although China’s consumption of new energy vehicles continues to grow rapidly, the overall growth rates of smartphone and automobile consumption have both fallen to single digits. This suggests that the enthusiasm for electronic consumer goods among young people and the growing population transitioning from middle school to university seems to be waning. Whether the upcoming AI era can still capture the interest of the younger generation requires closer observation of data.

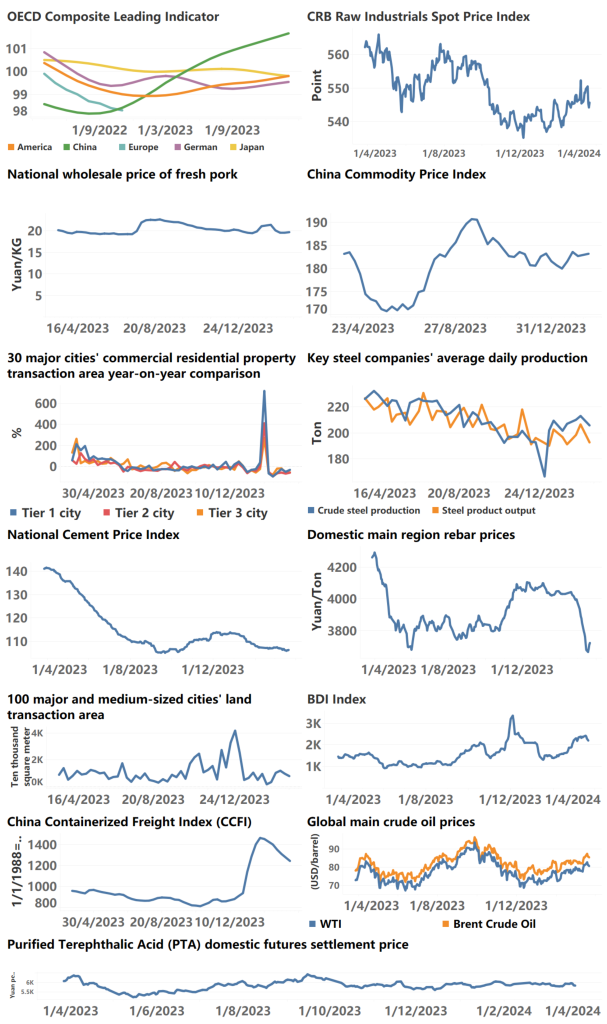

Let’s delve further into real estate data. The sharper-than-expected decline in the growth rates of sales area and sales value of newly constructed commercial housing, coupled with the continuous increase in the number of listings for second-hand houses, and the gradual decline in prices of both first-hand and second-hand houses disclosed by the National Bureau of Statistics, indicate a cooling market. We believe that there won’t be much bullish sentiment left in the real estate industry from all market participants. The signaling of prices suggests that for a considerable period in the future, real estate prices will remain stable. Such market expectations are gradually forming and will systematically change the operating styles of Chinese commercial banks, the investment and financing structures of Chinese local governments, and the entire capital market system in China. This stable economic condition is conducive to the rise of individual liberalism.

Long-term economic growth is rooted in institutions and the spiritual realm, and widespread innovation breakthroughs are eagerly awaited. We believe that any vibrant ideas will flourish in a free social environment.

International Perspective: Global Monetary Policy Divergence

This week, during a press conference, a journalist asked Powell about his views on the easing and tightening of the financial environment. Powell casually remarked that the financial environment always experiences periods of both easing and tightening. He downplayed concerns about potential localized liquidity shortages, stating they were not major issues. The Federal Reserve disclosed its expectations for the US economy in 2024 during this meeting: a growth rate of 2.1%, an unemployment rate of 4%, and a year-end Fed rate of 4.6%. This series of data reflects the Fed’s considerable confidence in the US economy.

However, significant changes have occurred in other major economies outside the United States. First, in Japan, the Bank of Japan initiated its first rate hike in 17 years, raising rates by 10 basis points to 0-0.1% and ending ETF purchases while continuing to purchase government bonds. This move symbolizes a significant shift for the Japanese economy. Although this rate hike still maintains an accommodative monetary stance regarding Japan’s inflation levels, in this “spring struggle,” corporations are raising worker wages by around 3-5%, far exceeding the international recognized inflation target of 2%. Clearly, the 10 basis points hike still leans towards accommodation, but it’s premature to conclude that Japan’s economy is overheating. This rate hike is more of a preventive measure, a gradual move towards restrictive monetary policy. Before crossing into restrictive monetary policy territory, rate hikes are beneficial for stabilizing Japan’s entire financial market. The volatility in the Japanese stock market will decrease, but the upward trend will remain. In the long run, whether Japan’s economy can break out of deflation and enter a phase of sustained expansion is highly dependent on corporate profitability. There exists a significant relationship between Japanese corporate profitability and overseas investments, especially considering the substantial increase in wages in the Japanese automotive industry during this wage hike, which correlates with the rapid rise in Japanese car sales in the United States. This may be due to high demand caused by replenishing inventory in the US automobile market. Monitoring the growth rate of the US automotive consumer market will help assess the sustainability of Japanese corporate profitability. Additionally, it’s worth paying attention to whether domestic demand in Japan will recover. Many works suggest that Japan’s deflation has formed a unified social expectation over the long term, affecting all aspects. Whether the resurgence of inflation in Japan can change this expectation and drive economic activity is also worth noting. We may not be able to simply compare Japan’s current situation with the high-growth period of the 1970s. Modern Japan has largely completed urbanization and industrialization. The key lies in the ability of young people to innovate in technology. This requires innovation in Japan’s corporate management model. Innovation is always disruptive. Without fresh blood, it’s challenging to foster new innovations. Overall, the challenges facing the Japanese economy are quite significant.

In Europe, Germany’s February CPI stood at 2.5%, down 0.4 percentage points from the previous month. Following the data release, European equity markets experienced a rapid upturn, reflecting a state where hot money is flowing into Europe globally. Expectations that the Eurozone will lead the Fed in interest rate cuts are gradually forming, especially after Switzerland took the lead in cutting rates by 25 basis points this week. Following the announcement in Switzerland, the US dollar index broke through the support level of 103, soaring to 104.5, completely reversing the downward trend of the past half-month. The upward movement of the US dollar index has brought about a series of changes in global capital markets. Global equity assets and commodities collectively retreated. The global market will enter a period of high asset price volatility. Investors should be mindful of their risk exposure. Continuously monitoring whether the strength of the US dollar index causes discomfort for the Federal Reserve is crucial, as it is undoubtedly a risk factor.