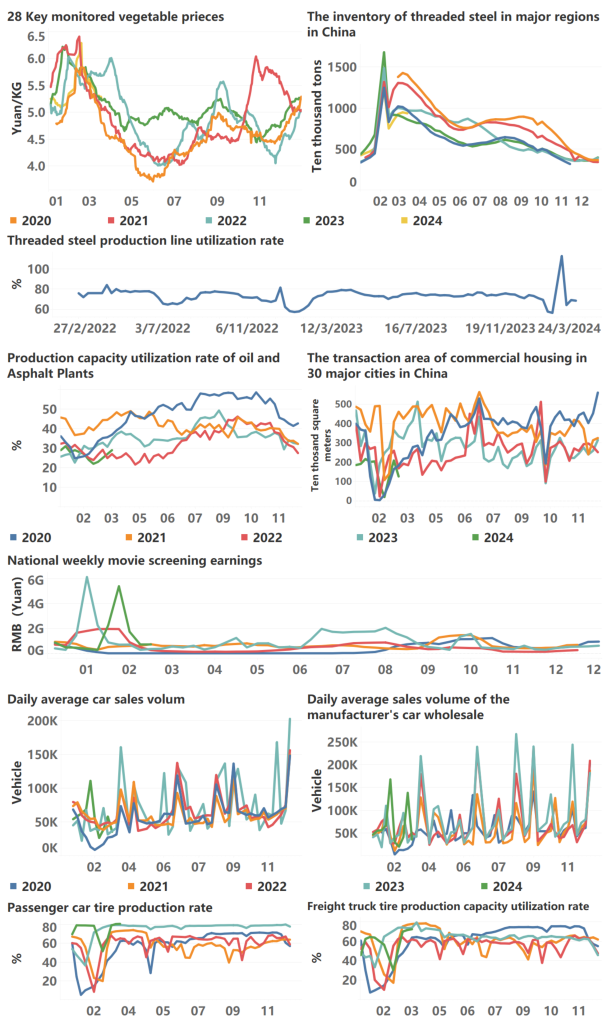

China : ' Equipment update promotes consumption '

Last week, we reviewed the report of the two sessions and mentioned the plan of updating equipment and exchanging old and new consumer goods. In the press conference, the relevant departments believed that the five trillion market could be involved. From the perspective of 126 trillion GDP in 2023, it can pull about 4 percentage points of growth, which is a considerable figure. This week, the State Council officially issued the ” Action Plan to Promote Large-scale Equipment Renewal and Consumer Goods Replacement ” notice, which aims to :

“By 2027, the scale of equipment investment in industry, agriculture, construction, transportation, education, cultural tourism, medical and other fields will increase by more than 25 % compared with 2023 ; the energy efficiency of the main energy-using equipment in key industries has basically reached the energy-saving level, and the proportion of production capacity with environmental protection performance reaching the level of A has been greatly increased. The penetration rate of digital R & D design tools and the numerical control rate of key processes in industrial enterprises above designated size have exceeded 90 % and 75 % respectively. The recycling volume of end-of-life vehicles is about twice that of 2023, the trading volume of used vehicles is 45 % higher than that of 2023, and the recycling volume of waste household appliances is 30 % higher than that of 2023. The proportion of recycled materials in resource supply is further increased. ”

The above target value involves the comprehensive field of investment and consumption. We never doubt the possibility that the Chinese government sets the target and then achieves the target. The stock assets mentioned in the above documents have shown a round of increase, and the market has already priced in advance, which lays a foundation for the subsequent disclosure of information.

After the official launch of the program, the boots landed, and the related stock assets fell back to a certain extent. Even if the above goals are so huge, the pressure for stock assets to profit and exit is still great. In order to achieve the above goals, the Ministry of Finance will increase fiscal efforts to promote consumption in the form of subsidies. Specifically, at present, the asset side of residents is shrinking, the income side is under pressure, the enterprise sector is weak in the face of CPI and PPI, and the profit is weak. To promote the active consumption of residents and the active investment of enterprises, it is necessary to have real gold and silver. From the previous measures, the Ministry of Finance will adopt the way of accelerating depreciation of enterprise assets to carry out tax deduction operation to promote the active renewal of enterprises. This goal is to be achieved by 2027, simply look at the average annual growth of 5-6 % can be, basically can be achieved. However, from the point of view of the whole national economy, to promote so many industries to carry out large-scale equipment update, will certainly be able to pull the corresponding upstream asset prices. The average annual growth of used car trading volume should reach about 10 %. Considering that the current new car price war continues to heat up, the price of used cars may need to decline by a larger margin.

The money market demand is still weak, and the uncertainty of the property market is increasing

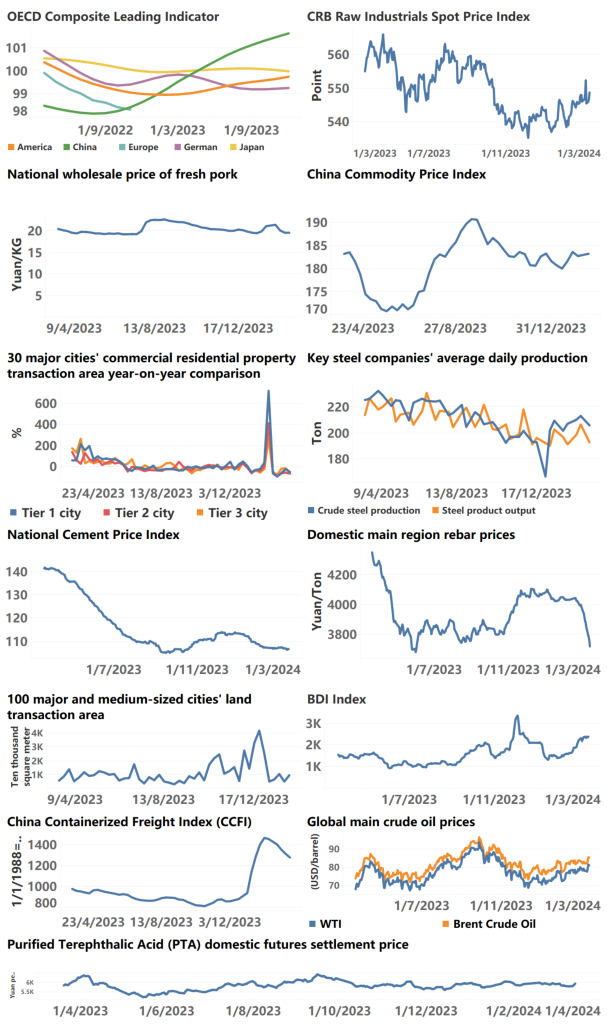

In terms of data, China has released very critical financial data. In February, social financing increased by 1.56 trillion yuan, a year-on-year increase of 1.6 trillion yuan, which is lower than the market average expectation of wind statistics ( 2.4 trillion yuan ) ; the growth rate of stock social integration was 9.0 %, down 0.5pct from the previous month. M1 rose 1.2 per cent year-on-year in February, down 4.7pct from the previous month. M2 rose 8.7 % year-on-year, unchanged from the previous month. On the whole, the financial data in February is weaker than expected. Although the year-on-year growth of CPI in February changed from − 0.8 % in January to 0.7 %, the financial data is still not ideal. The basis for price stability is not very solid. The financial data of the financial sector increased more than the year-on-year, the growth rate of M1 continued to decline, and the growth rate of M2 remained stable, indicating that the money demand of the overall market is still weak. The money supply is still dominated by medium and long-term funds, and the willingness to prevent savings is still relatively high.

Although the People ‘s Bank of China ‘s RRR cut in mid-February released $ 1 trillion of liquidity and guided the 5-year and above LPR down by 25 BP, it does not seem to stimulate the demand for money. Instead, it further aggravated the congestion of treasury bond transactions throughout the decade and 30 years, and the phenomenon of capital idling further intensified in the financial system. For the central bank, it has been trying to recover market liquidity in open market operations since last week. Treasury bond futures have also entered a shock phase accordingly, and the social finance data in March is not expected to be ideal. In order to raise the level of money demand of the whole society, the central bank may consider reducing short-term interest rates, and the Ministry of Finance should accelerate the supply of treasury bonds and special bonds.

In terms of real estate, in February, the sales price of new commercial housing in first-tier cities fell by 0.3 % month-on-month, the same decline as the previous month, down 1.0 % year-on-year, and the decline was 0.5 percentage points higher than the previous month. The sales price of second-hand housing decreased by 0.8 % month-on-month, a decrease of 0.2 percentage points compared with the previous month, a year-on-year decrease of 6.3 %, and a decrease of 1.4 percentage points compared with the previous month. The decline in the price of second-hand housing is still very fast. According to the data provided by the market parties, the number of second-hand houses in Beijing is also rising rapidly. On March 14, Hangzhou completely liberalized second-hand housing purchases and no longer set any purchase conditions. It is expected that major cities across the country will open a large-scale adjustment. At present, this unilateral behavior of real estate prices is a very horrible phenomenon from a financial point of view. Once unilateral financial behavior has no appropriate means of regulation, it will increase the volatility of the entire market. Judging from the latest Vanke and Country Garden insurance, the speed of sales recovery is still too slow.

If the price continues to decline, the speed of return will be slower, which will further affect the capital problem of Baojiao Building. At present, Vanke seems to have passed the liquidity risk of this round through rapid financing means such as Reits.We reported in the previous report ‘ Where is the equilibrium price of real estate ? It is believed that with the decline of prices, the purchase behavior of residents should rise, and there will be a balanced market price. However, at present, this unilateral price behavior is difficult to provide a macro environment for the formation of balanced prices.

U.S. : PPI soars, market responds to volatility

On the U.S. side, the key February price data was released, in which the February CPI was 3.2 % year-on-year, an increase of 0.1 percentage points from the previous month ; pPI rose 1.6 % year-on-year, 0.7 percentage points higher than the previous month. From the perspective of CPI subdivision, the rise of energy and housing prices has made the US CPI decline very slowly. The US core CPI fell from 3.9 % in January to 3.8 % in February, and the downward trend was also quite slow. The evening of the US CPI announcement did not seem to have a great impact on global markets, because energy prices remained above $ 80 and still contributed a large part of inflation. However, after the US PPI announcement, global markets have undergone rapid changes. The dollar index has risen, US bond yields have risen, global capital markets have fallen, and commodity highs have fluctuated. If US PPI growth exceeds 2 % year-on-year, it is almost impossible for CPI to fall back below 2 %. The 1.6 % PPI data is a quite dangerous interval.

In terms of expansion, the Fed believes that for the US economy, the supply-side problem has almost been solved, which is reflected in the stability of PPI growth. At present, it is necessary to maintain a restrictive interest rate level to cool the heat on the demand side, which is reflected in the stability of CPI growth and the decline of job vacancy rate in the service industry. If the growth rate of PPI rises, then the supply-side problem will interfere with the Fed ‘s decision-making behavior again. From the global market, this undoubtedly increases volatility.

On the European side, Germany ‘s CPI fell to 2.5 % in February from 2.9 % in January, which is quite close to the 2 % inflation target for the eurozone. Officials in the eurozone committee have come out to say that it is also possible for the eurozone to cut interest rates earlier than the Federal Reserve. We discussed in the previous report of the euro zone first cut interest rates, the dollar remains strong, the global asset pressure situation may become a reality.