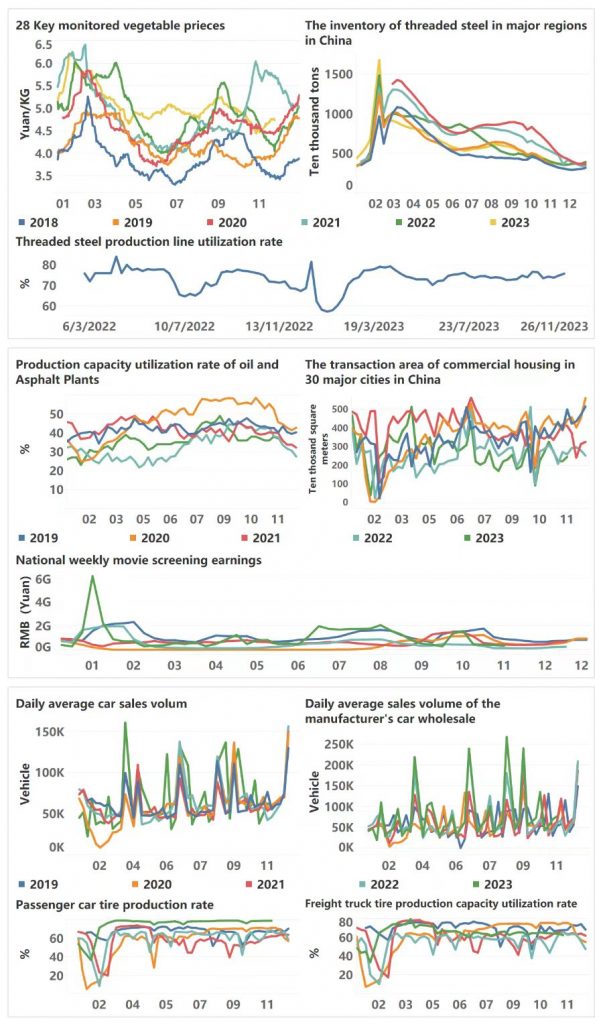

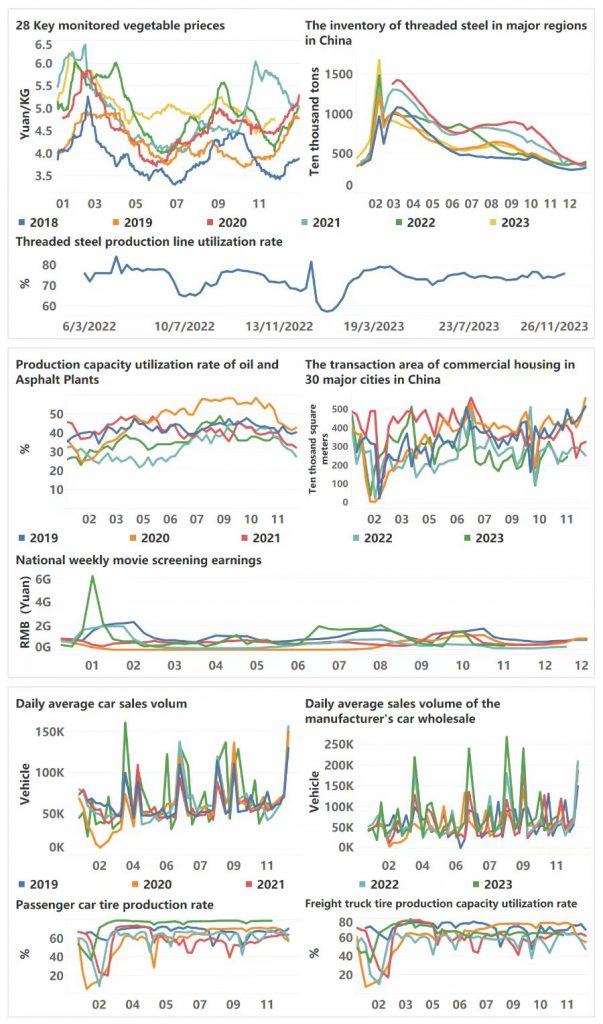

PMI Continues to Decline

On November 30, data released by the National Bureau of Statistics showed that in November, the Manufacturing Purchasing Managers’ Index (PMI) was 49.4%, a decrease of 0.1 percentage points from the previous month, indicating a slight decline in the prosperity level of the manufacturing industry. The Non-Manufacturing Business Activity Index was 50.2%, down 0.4 percentage points from the previous month. The Composite PMI Output Index stood at 50.4%, down 0.3 percentage points from the previous month, showing an overall declining trend.

The decline in the data generally suggests that the Consumer Price Index (CPI) and Producer Price Index (PPI) in November will continue to fall, and it is expected that investment and consumption data will remain low. In the manufacturing sector, the National Bureau of Statistics stated that 60% of enterprises reported insufficient orders. In the non-manufacturing sector, following the lifting of pandemic restrictions earlier this year and high travel activity during the summer vacation, the Service PMI has gradually declined from its peak and is expected to continue to fall before the new year. The overall decline in the Composite PMI is attributed to weak demand, deflationary pressures, and debt crises. This week, data related to real estate debt began to surface, with significant exposures in channel funding businesses represented by the Zhongzhi series, involving some quantitative funds and reaching billions in scale. An interesting observation to make is whether there will be a steep decline in China’s jewelry sales in the coming period.

The upcoming Central Economic Work Conference will discuss next year’s economic growth targets. Real estate remains a significant uncontrollable factor for next year. This year’s real estate regulatory policies, judged by the number of second-hand housing listings, have not yet achieved the goal of bottoming out the market, and residents’ expectations of the real estate market are still adjusting. This week, the People’s Bank of China led a banking symposium to implement loan demands for real estate enterprises. However, the actual impact might be limited due to the few assets available for mortgage by real estate companies.

There is market speculation about the Pledged Supplementary Lending (PSL) program, which involves the central bank directly purchasing assets. PSL could take three forms:

- Direct purchase of bonds and stocks of real estate companies: This could stabilize stock prices and protect small and medium investors, but it might be difficult for PSL to avoid losses.

- PSL as a re-lending tool: Purchasing commercial banks’ loans to real estate companies and securitizing these assets.

- Direct purchase of new homes, second-hand homes, and other physical assets. PSL, as a last resort of the central bank, is comparable in scale and intensity to the Bank of Japan’s ETF purchase program, the European Central Bank’s asset purchase program, and the U.S. Federal Reserve’s bond repurchase program. However, PSL is constrained by several factors:

- Political milestones;

- Potential impact on economic reform plans discussed at the Third Plenary Session;

- Yuan devaluation and stagflation.