Foreign Exchange: Significant Appreciation of the Renminbi

This week, the exchange rate of the US dollar against the renminbi depreciated from around 7.2 to 7.14. The primary reason is the global perception that the US dollar interest rate has peaked, and the US dollar index has significantly decreased after the release of the US CPI in October. Regarding the future trend of the US dollar index, Goldman Sachs believes that even in the US interest rate cut cycle, the US dollar will remain strong among global currencies. This is mainly due to the strong performance of the US economy. Therefore, even though there was a significant appreciation of the renminbi this week, it is not appropriate to compare it to last year’s scenario when the US dollar depreciated to 6.3 against the renminbi. At that time, there was a greater risk of a hard landing for the US economy, and China’s real estate industry was still performing strongly.

For the US dollar index, a more apparent risk is the US debt crisis. As interest rates are expected to remain high for a longer period, the US Treasury’s debt crisis is likely to reoccur. Particularly in 2024, an election year in the US, the Treasury’s ability to expand fiscal budgets will be constrained. China is currently in the process of selling off US Treasury bonds, while Japan appears to have ended its sell-off. It is essential to keep an eye on the behavior of the two largest buyers of US Treasury bonds and to assess the evolution of the US Treasury bond storm in 2024. The US Treasury bond storm gradually eased in 2023 due to McKinsey’s concessions, but it may intensify in 2024. Of course, there could be significant trading opportunities if a large amount of cash is stockpiled beforehand.

After the appreciation of the renminbi against the US dollar, China’s A-shares did not experience a widespread rebound, and the Hang Seng Index also showed weak performance. The Nikkei performed better. The main factor driving the renminbi’s appreciation was the decline in the US dollar index, but the domestic economic endogenous momentum remains insufficient, as seen from the economic data in October. Additionally, this week, the flu trended nationwide, and there are no signs of an economic rebound in November compared to October, considering consumer progress and resident travel. The central bank has been injecting liquidity into the MLF for several weeks, and from the interbank and exchange markets, this liquidity injection mainly went towards local government debt restructuring. However, these funds did not stimulate investment after debt resolution, and therefore could not generate money. Stocks, being assets sensitive to liquidity, naturally do not have a foundation for significant recovery. “Confidence is more important than gold, and what everyone lacks now is gold.”

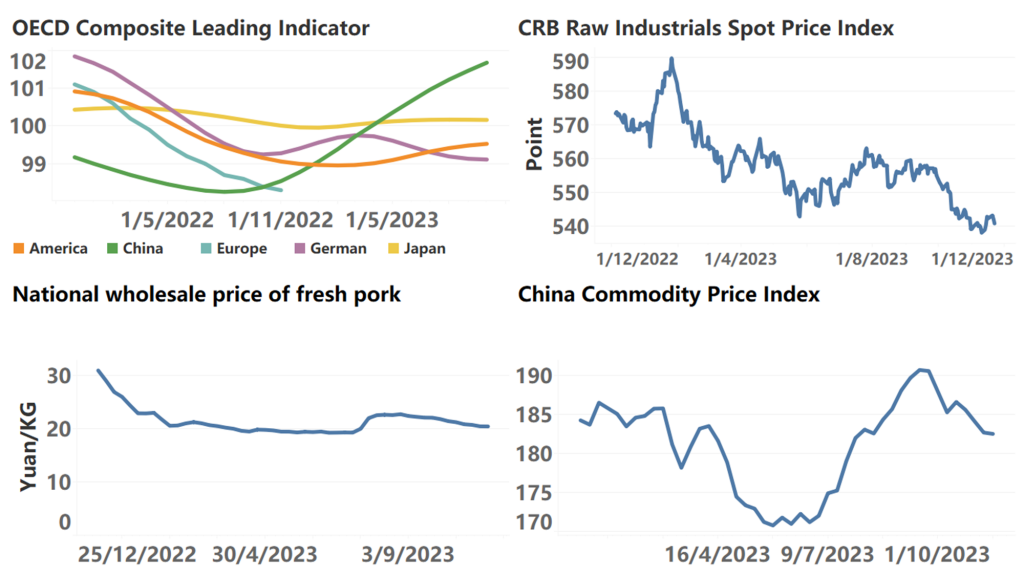

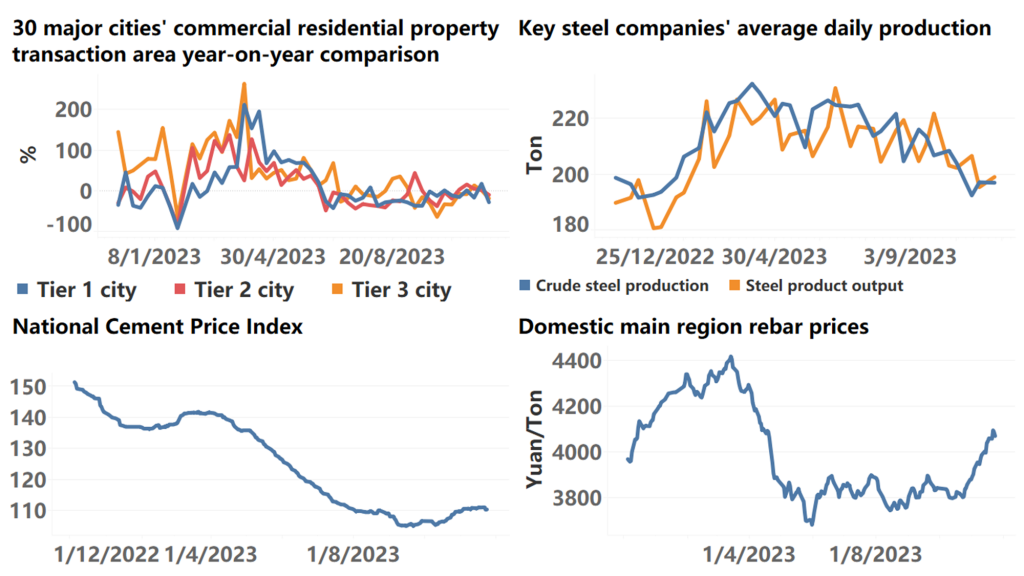

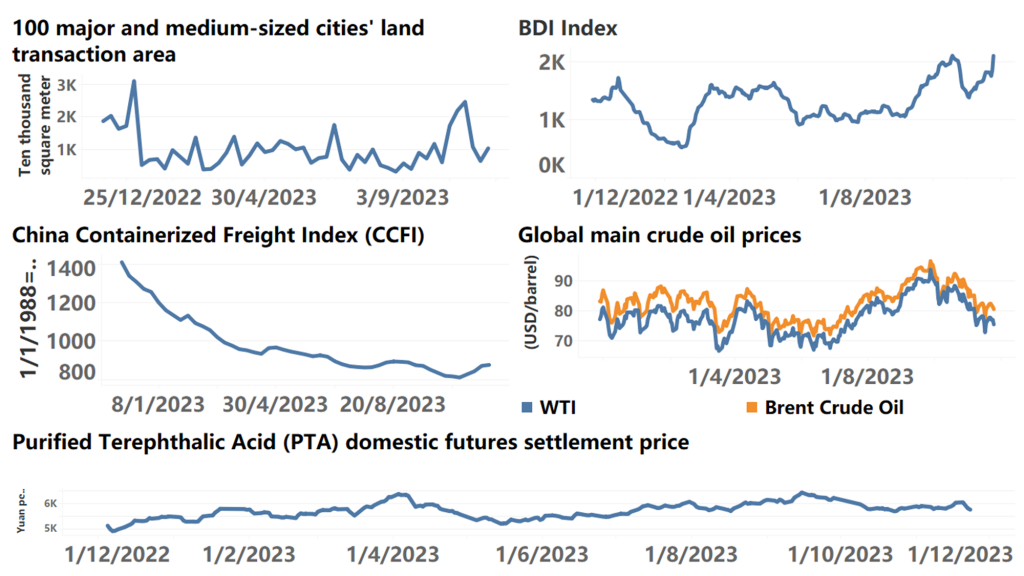

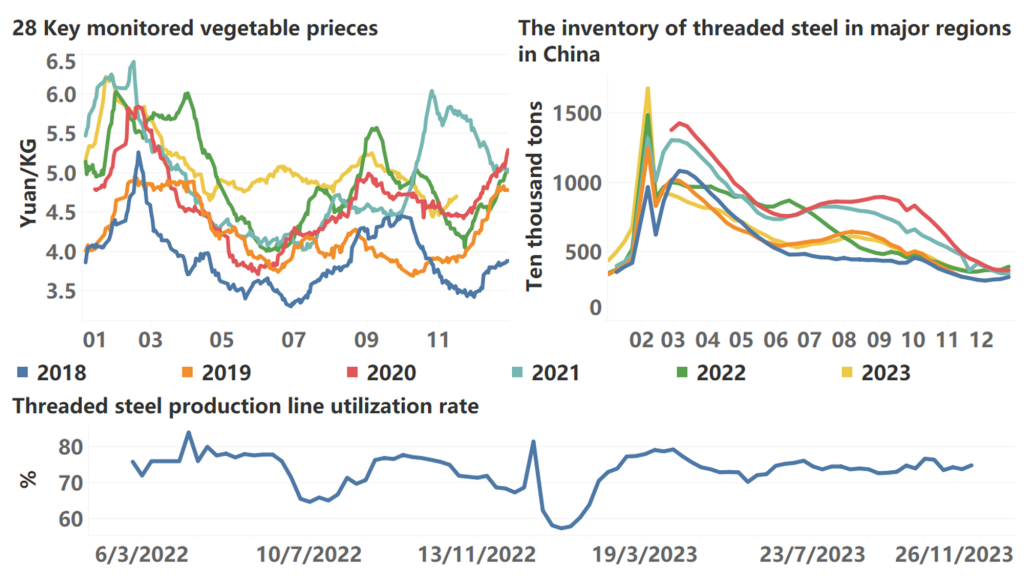

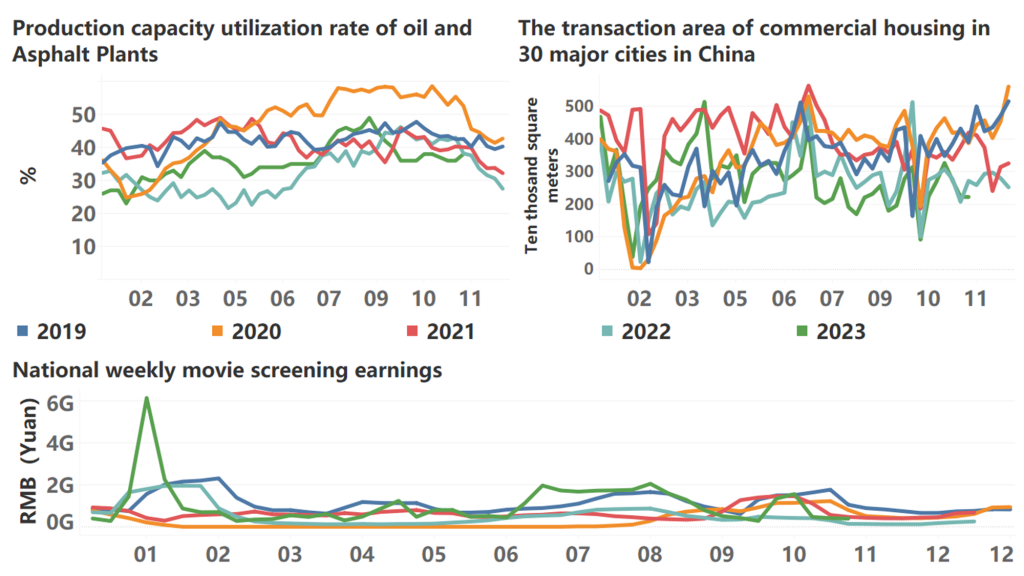

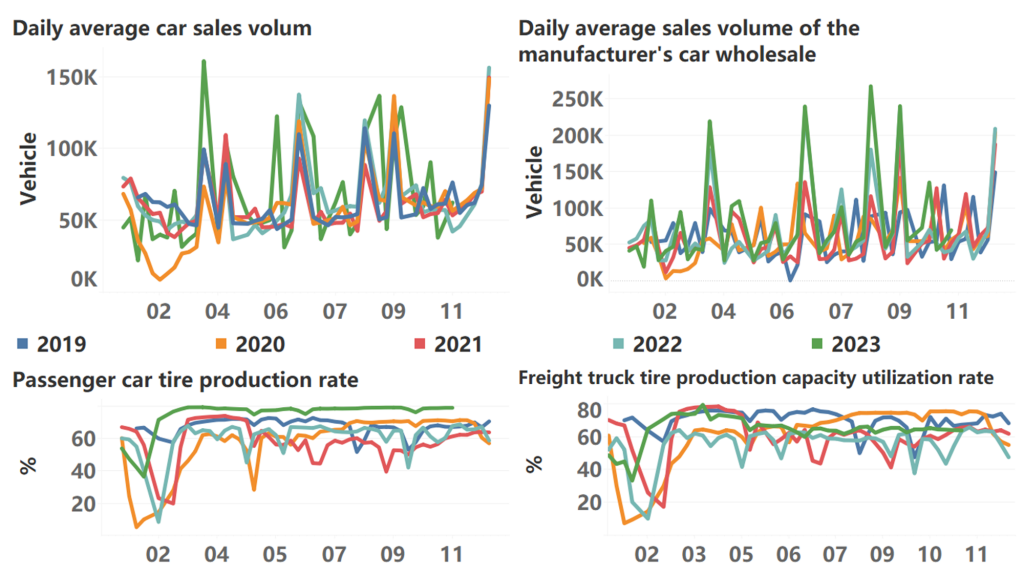

The following are high-frequency data for this week:

*Translated by ChatGPT