Federal Reserve Interest Rate Meeting

On November 2nd, American time, the Federal Reserve held an interest rate meeting and decided to continue the pause in rate hikes. This was the second pause since September; during this period, the overall inflation index of the American economy did not rebound, and the market expects that the inflation data for the U.S. in October will drop significantly to 3.3%. Looking at the components, energy data did not surge significantly due to the conflict between Palestine and Israel, and import-driven inflation has concluded. Powell’s performance at the press conference was overall dovish. He indicated that the Fed has not yet considered when to lower interest rates, conveying an attitude that short-term rates will still maintain a restrictive level. In general, the upcoming economic data from the United States will be quite important. Currently, the overall direction of the economy is quite chaotic. The U.S. CPI will face a lower base next year and has considerable room to rebound. The growth rate of 4.9% for the U.S. economy in the third quarter is very likely to continue, which increases the possibility of the long and short-term interest rates rising. Strong economic growth with inflation risk on the rise. Some believe that the yield on U.S. 10-year Treasury bonds could exceed 5%, and this risk still exists. Overall, the financial market liquidity is not yet at a stage of significant rebound.

Last week, after the Federal Reserve’s interest rate meeting, U.S. stocks rose consecutively, reaching the previous high points again, showing obvious volatility. We predict that U.S. stocks may experience short-term volatility upwards, and the pressure for the U.S. dollar index to rise is significant. Another point worth noting is that Japan’s central bank’s monetary policy may change, that is, to abandon the loose monetary policy. A representative data point is South Korea’s inflation index reaching 3.8%, and the Nikkei may have certain opportunities subsequently.

Domestically

Last week, a financial work meeting was held in China, which was convened after a six-year interval due to the impact of the pandemic. In these six years, China’s overall financial structure and legal system have been gradually improved. The meeting listed many work goals, including continuing to standardize the business processes of financial institutions and strengthening financial support for the real economy.

Last week, China’s capital market as a whole showed an upward trend, and there were many positive news on the news front, such as repurchases of stocks by manufacturing companies, financial regulatory authorities guiding long-term funds into the market, and the national security department dealing with malicious short-selling, showing a clear determination to maintain financial stability. Whether the financial market can stabilize ultimately depends on the progress of the overall macro economy. Judging from the approval of a special one-trillion-yuan national bond last week and the overnight interbank lending rate rising to 50% this week, the overall Chinese economy still faces deflationary pressures, and the growth rate of corporate bond financing and residential loans is still not ideal. Whether real estate and stock asset prices can stabilize? Can the downward momentum be halted? At present, it seems difficult for the economy to recover on its own. The key is how to inject liquidity into the economy. A very important issue is that after Evergrande’s Xu Jiayin and other executives were charged, the group’s debt restructuring entered a state of suspension, and it is expected that a professional official work organization will take over the debt work. According to the current market disclosure, Evergrande’s debt is divided into three types: the first is accounts payable bonds, the second is commercial paper, and the third is execution assets judged by local governments, each debt being around two hundred billion RMB. If only the local working group in Shenzhen is relied upon, it would be difficult to coordinate the nationwide accounts payable issues, and debt restructuring would be even more difficult. The financial work meeting proposed to treat real estate enterprises of various ownerships equally and to provide liquidity support. But to implement the requirements of the financial work meeting, the key still lies in having funds. Given the current situation of local fiscal revenues and expenditures, it is difficult to make a breakthrough. This week, the news of the issuance of just one trillion special national bonds alone caused such tension in bank overnight liquidity. In addition, with the central bank increasing the short-term liquidity injection, liquidity will continue to rise. On this basis, we believe that domestic gold targets may have the opportunity to go long.

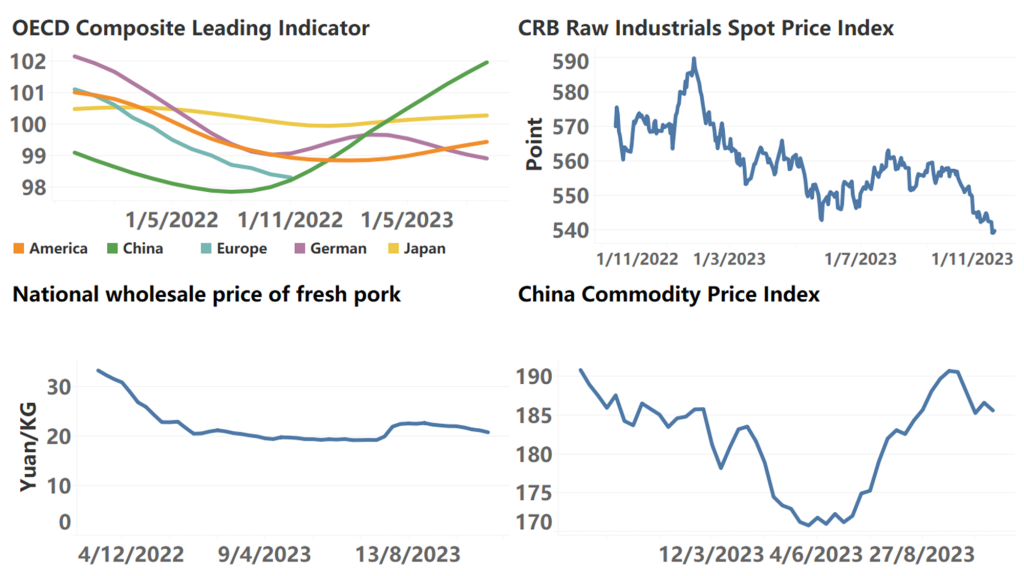

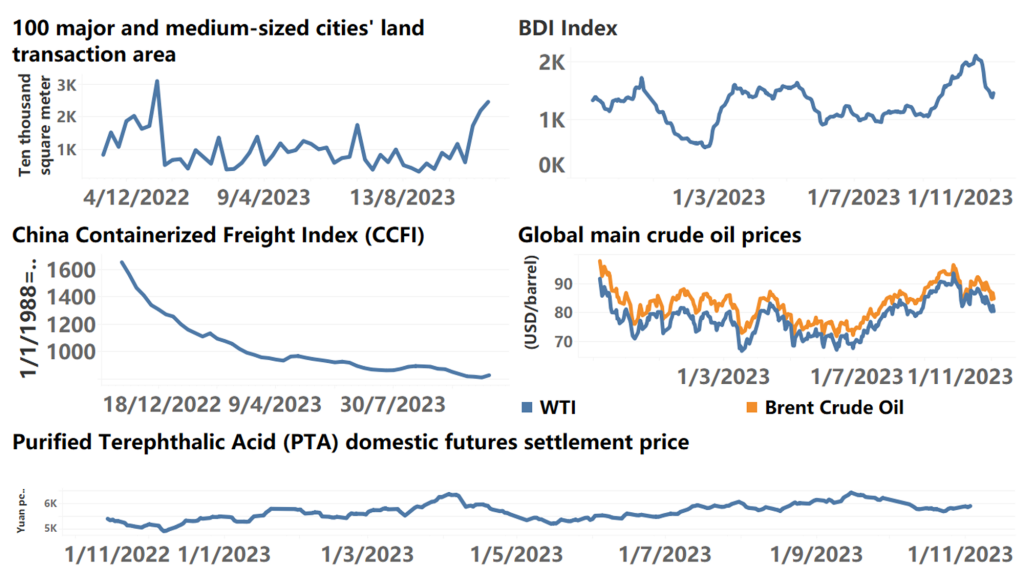

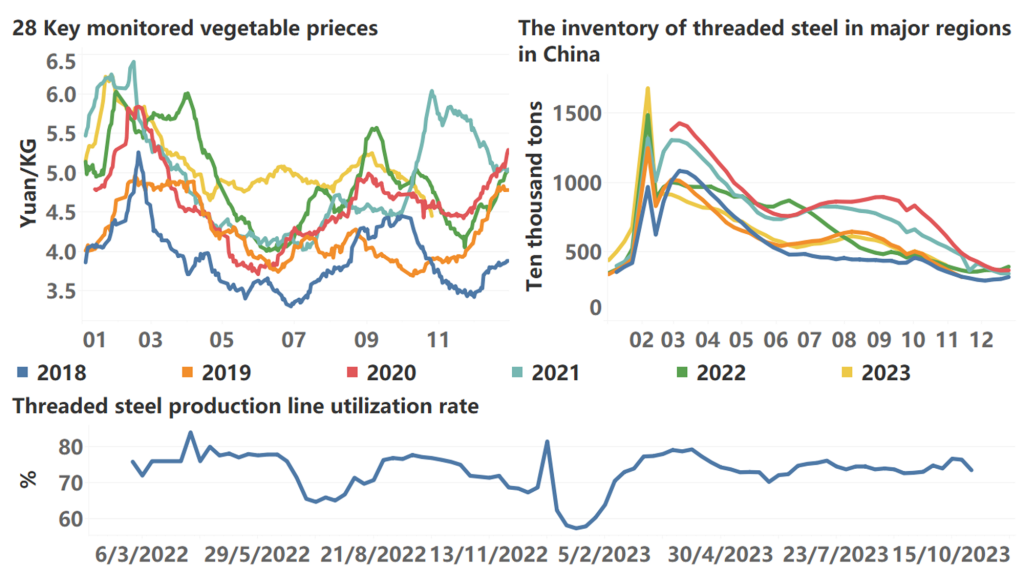

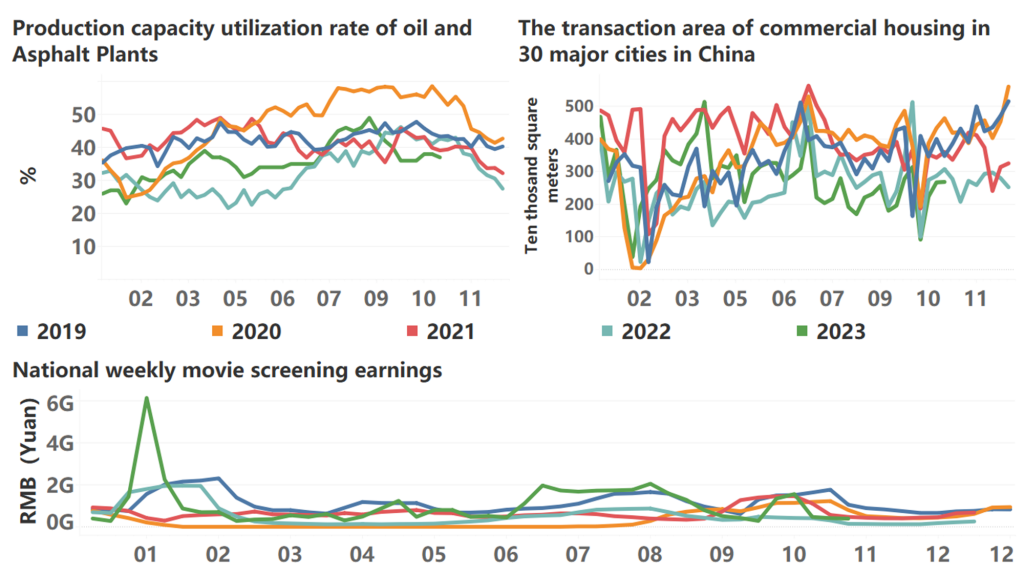

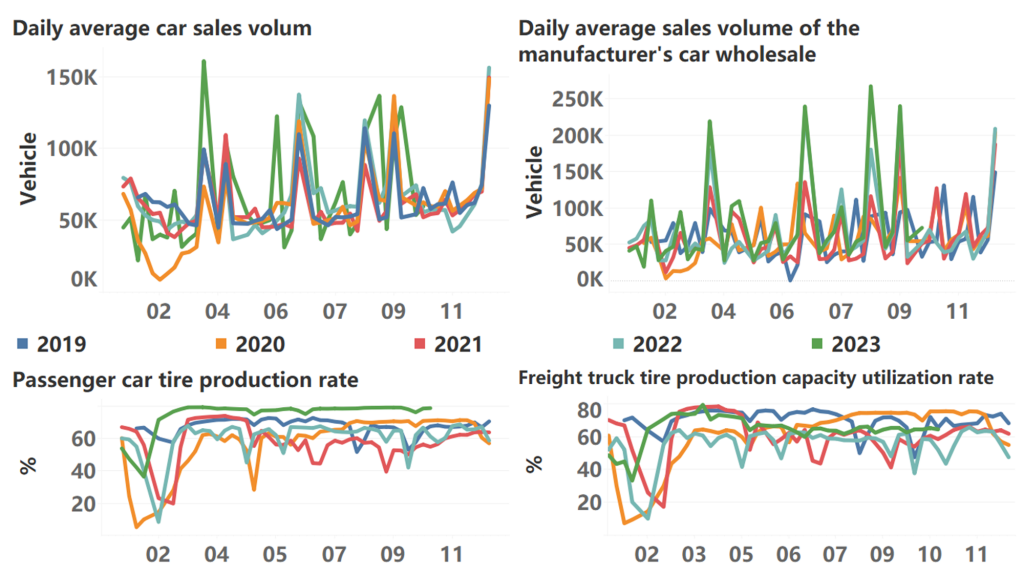

The following are high-frequency data for this week:

*Translated by ChatGPT