The US Q3 GDP showed a year-on-year growth rate of 4.9%, exceeding the market’s expectation of 4.5%. Although it only surpassed the forecast by 0.4 percentage points, the market had significantly underestimated the economic expansion rate during the third quarter, as the 4.5% forecast was only gradually adjusted since the start of October. Against this backdrop, the yield on 10-year treasuries surged to 5% before retreating to 4.86%. After the release of the Q3 GDP data, it rebounded near 4.9%. The 5% bond yield was initially impacted by short-term US bond supply. On one hand, the US Treasury issued a large amount of bonds in the short term, and on the other hand, the Fed continued its balance sheet reduction by selling treasuries. This led to increased market supply, dropping prices, and rising yields, exerting great pressure on the global capital market.

From a stock perspective, both the Dow Jones and NASDAQ have retreated to support levels. The key question now is whether they will break below these levels.

In terms of assets, cryptocurrencies have been on the rise. Partly due to market speculation around the SEC approving ETFs and also due to risk aversion sentiment. This week, cryptocurrencies stood out as the most notable asset. Gold also saw a slight increase, while the US dollar index remained around 106. It’s worth observing if the US dollar index is entering a consolidation phase. After this round of adjustments, we might have a new understanding of digital currencies. They rise with the stock market when global liquidity is high and take on a gold-like safe-haven status when liquidity is tight. They are also heavily influenced by regulatory news.

This week, the National People’s Congress approved the issuance of an additional one trillion special bonds by the State Council. Half of this will be utilized in Q4 of this year and the remaining half next year. This ensures ample funds for infrastructure projects, preventing incomplete projects. Normally, between October and December, there would be news about structural reforms from the third Plenum, but no major policy news is expected in these months this year due to the extra trillion in bonds being beyond expectations.

One reason for this bond issuance might be that the proactive fiscal policy of 2022 required a lot of spending, and a 3% fiscal deficit in 2023 isn’t sufficient. The adjustment of the real estate sector exceeded expectations, and it’s far from stable.

In terms of capital markets, the external interest rate environment is very stringent, putting downward pressure on China’s asset prices. This week, the Chinese A-share market once again defended the 3,000-point mark. From a hindsight perspective, we didn’t anticipate the US economy’s 4.9% growth rate in Q3. The news of the trillion bonds might be accompanied by a short-term liquidity injection by the central bank. However, this trillion in bonds shows the central government’s clear signal to ensure economic growth, which is good news for the capital market. As for the trend of A-shares, there has been an increase over two trading days.

In summary, domestic investors can buy low and sell high in the short term, engage in intraday trading, short the NASDAQ and Hong Kong stocks globally, and go long on gold.

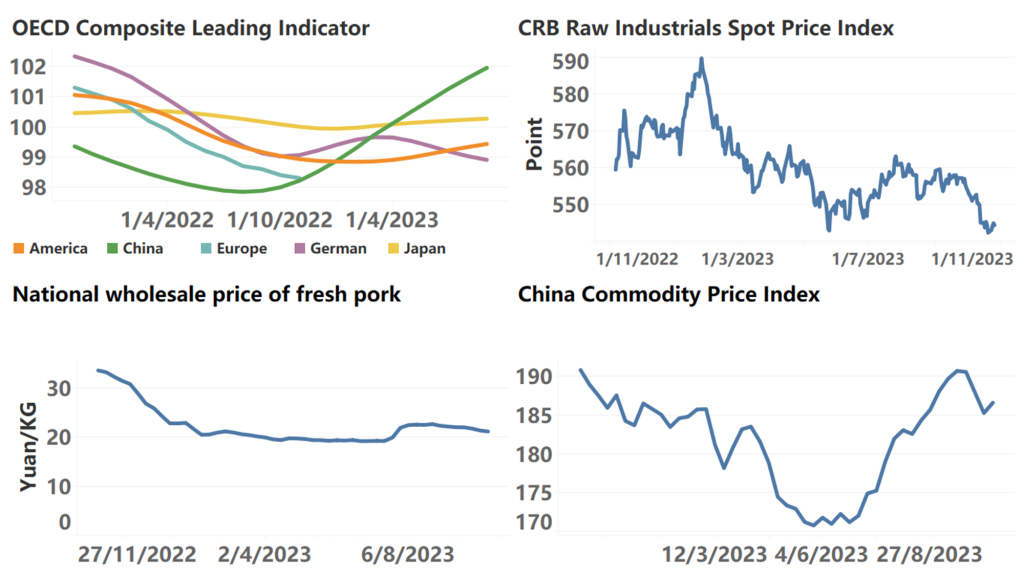

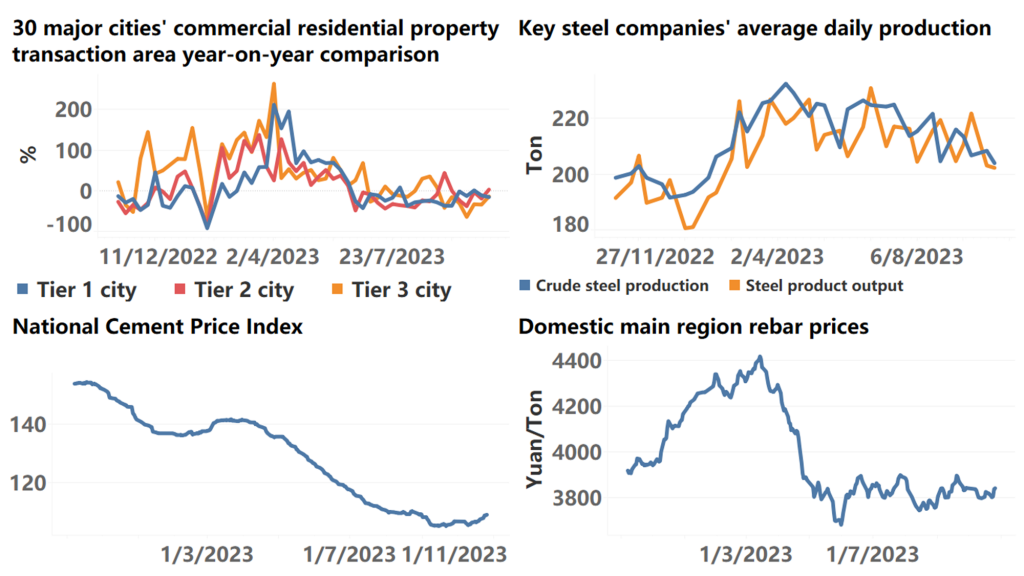

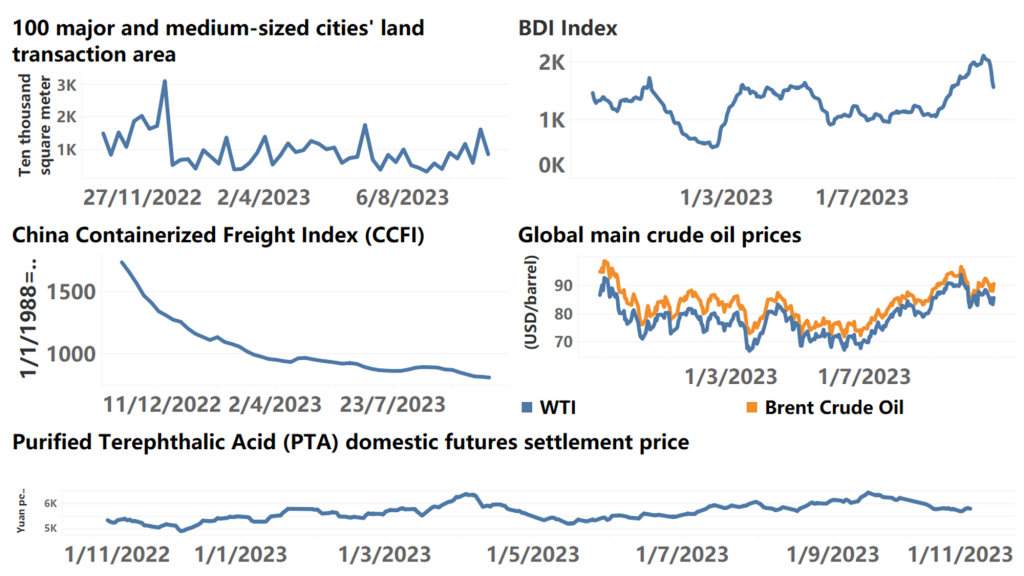

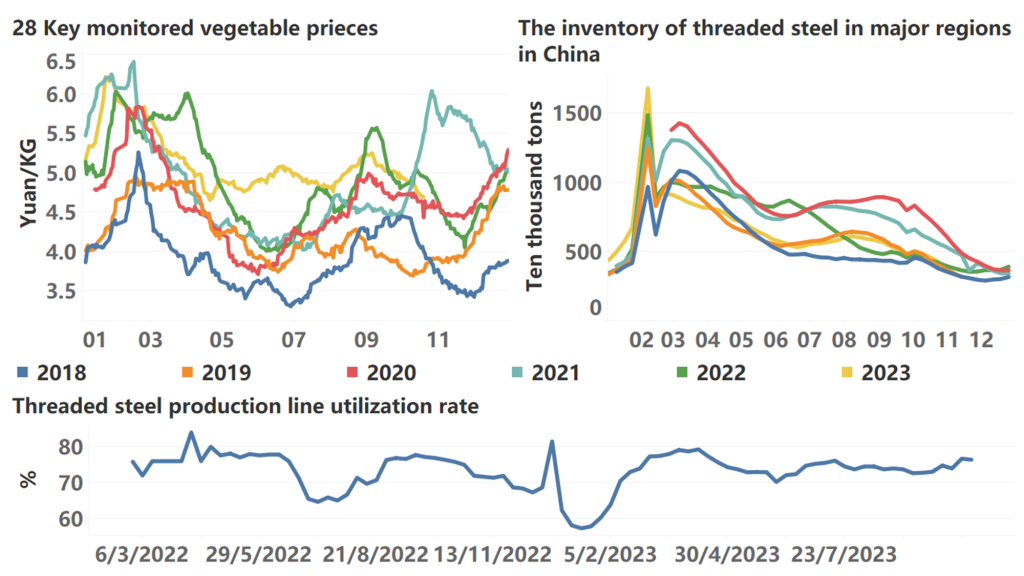

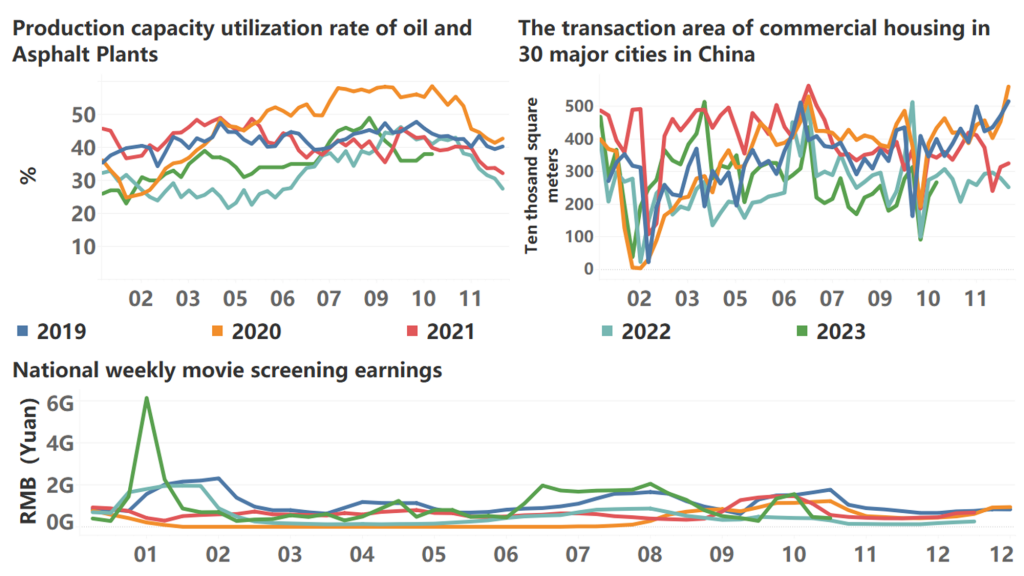

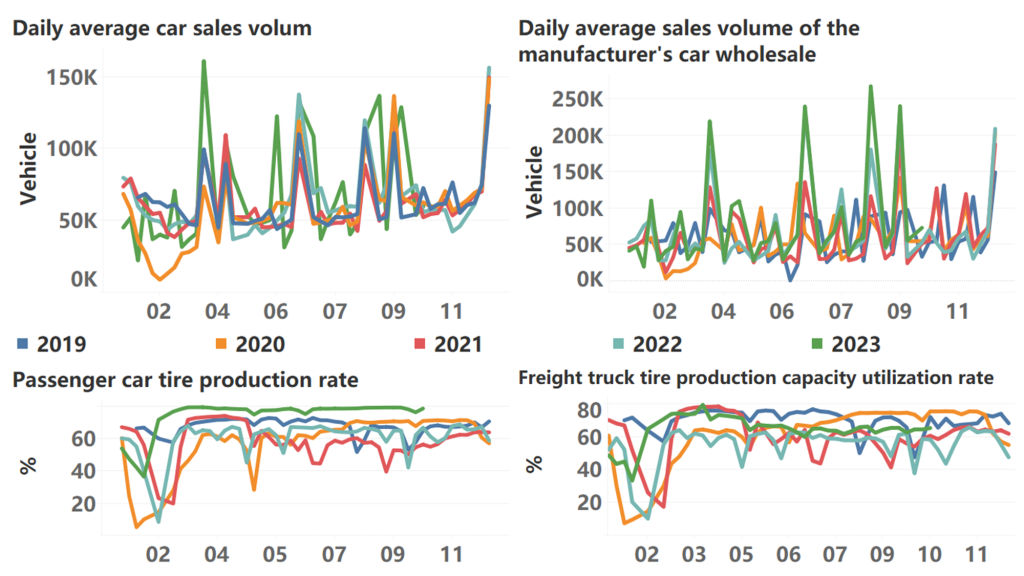

The following are high-frequency data for this week:

*Translated by ChatGPT