The GDP for the third quarter grew by 4.9% year-on-year, accumulating to 5.2% year-on-year. According to the National Bureau of Statistics, if the fourth quarter reaches 4.4%, the annual target of 5% can be achieved. Last year’s fourth quarter was 2.9%, with a relatively low base. Given the current recovery trend of retail sales, the stable development of manufacturing investments, and assuming there is no concentrated outbreak of real estate debt, a 4.4% growth rate in the fourth quarter is essentially attainable. In light of this, we believe that there won’t be any major economic conferences until mid-December. The focus of macro-control policies will be on implementing existing policies. From the perspective of the central bank’s use of monetary price and quantity tools, the LPR quotation hasn’t decreased. The reverse repo volume has significantly increased in the short term, and the intensity of market liquidity injection is increasing. The space for further rate cuts and reserve requirement ratio reductions is not particularly large. The most crucial issue for the economy at this stage is the debt restructuring negotiations related to real estate issues, which are difficult to solve with simple fiscal and monetary policy tools. Real estate debts seem to be surfacing, with risks emerging related to Longhu and Country Garden debts. Looking forward to the first quarter of 2024, whether the intrinsic growth momentum of the economy can continue depends on the external environment. From an internal perspective, China is likely to maintain a stable and progressive working tone. This year’s experience has shown that this approach has indeed produced good results: unemployment has gradually decreased, the price environment has remained stable, and consumer momentum has increased.

Currently, gold, crude oil, and the US dollar index are all rising simultaneously. This indicates that global risk-averse sentiment is high. The robust US economy and these two factors have become the dominant factors for global asset prices. Our previous judgment on the US dollar index was clearly erroneous. We believed that the US dollar index would not exceed the previous high of 105, but it is now moving towards 107. Global asset prices are clearly suppressed, and the US bond yield curve has become steeper, stimulating expectations of long-term financial contraction. The key lies in whether the strong US economy can be sustained. This can be determined by gradually observing US data. It may be a gradual process, but the unpredictability of the Israel-Palestine conflict risk is clearly much larger. When Israel launches an aggressive attack, will there be a spillover risk to nearby oil-producing nations, leading to a continued rise in oil prices?

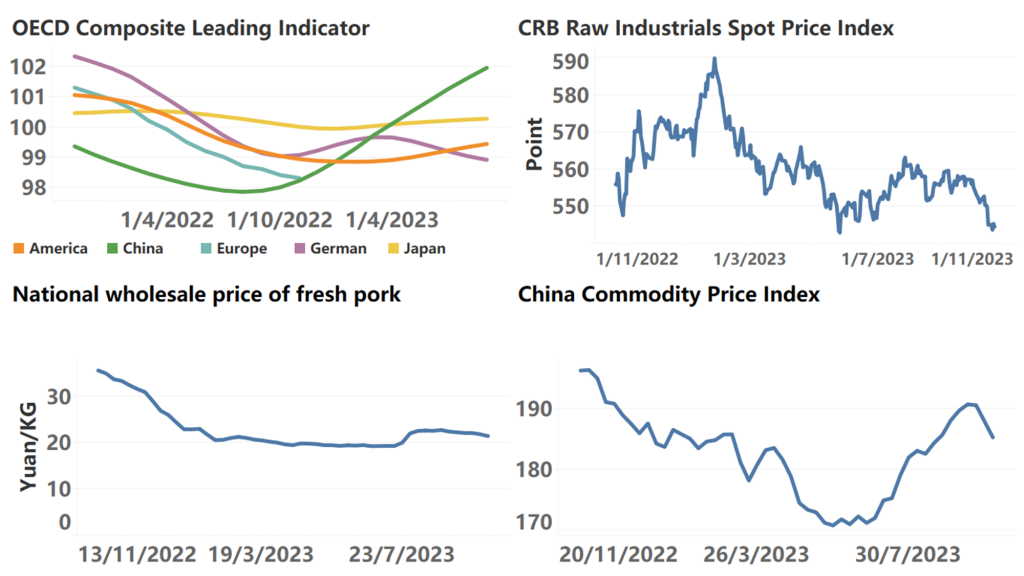

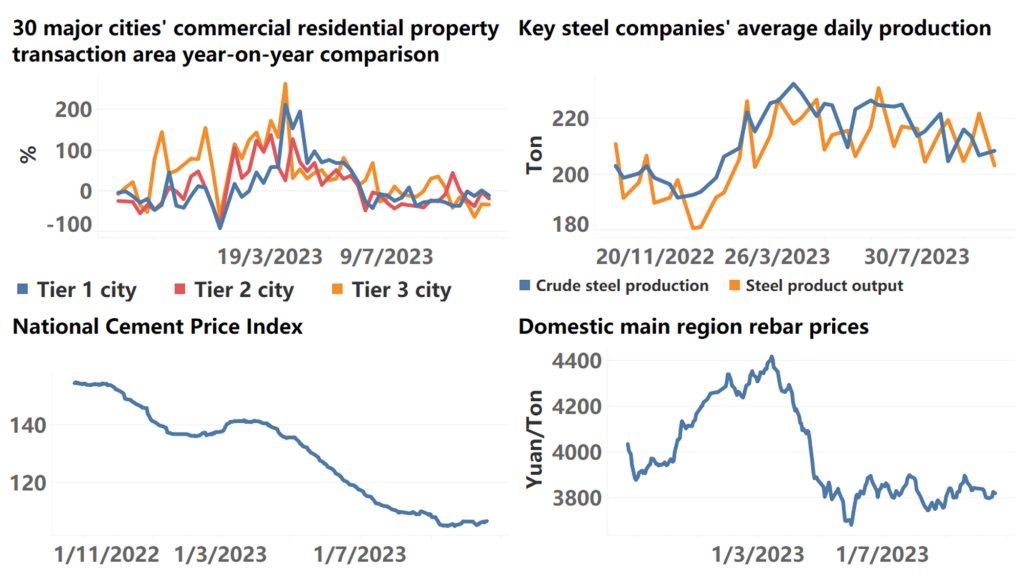

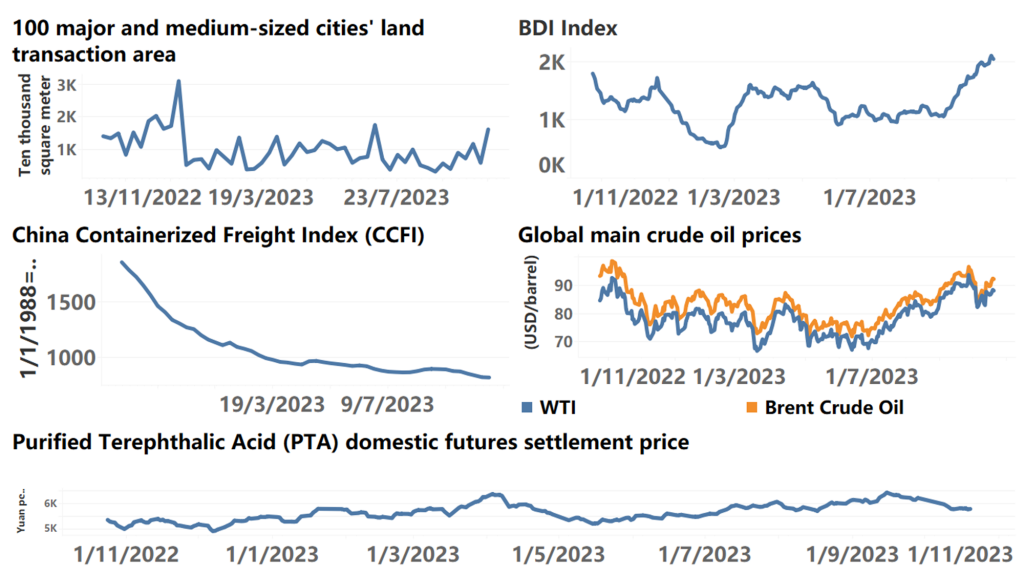

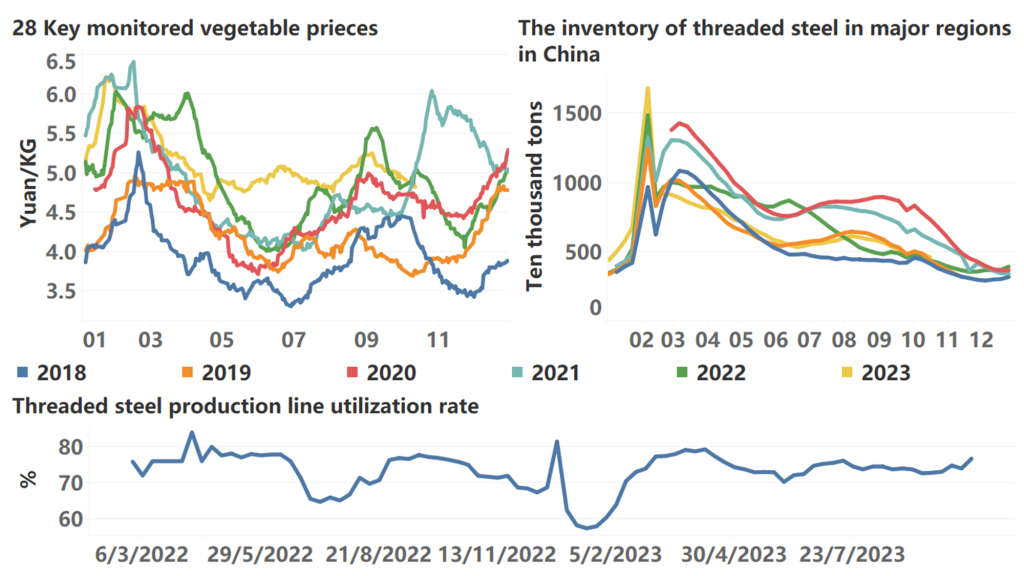

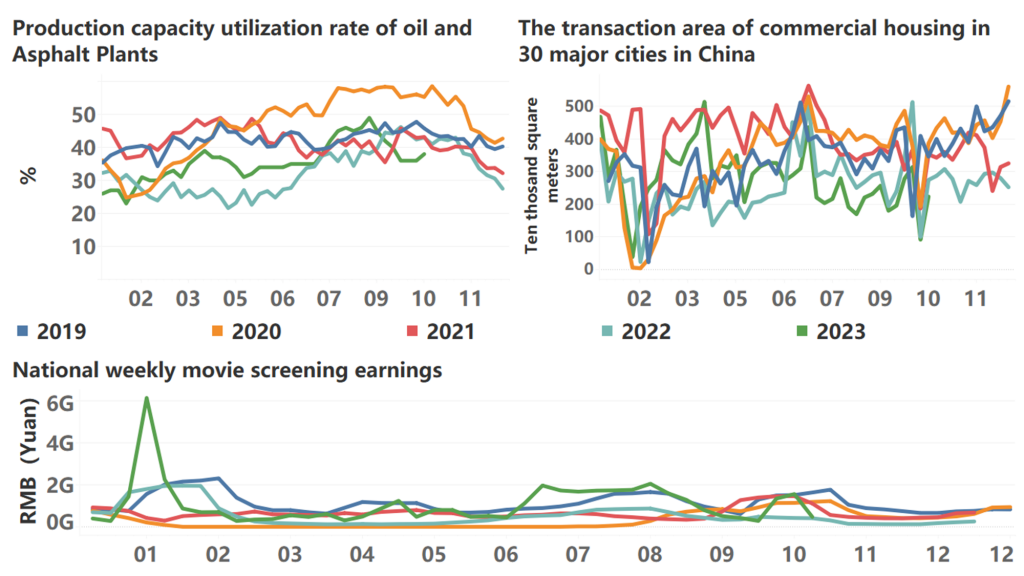

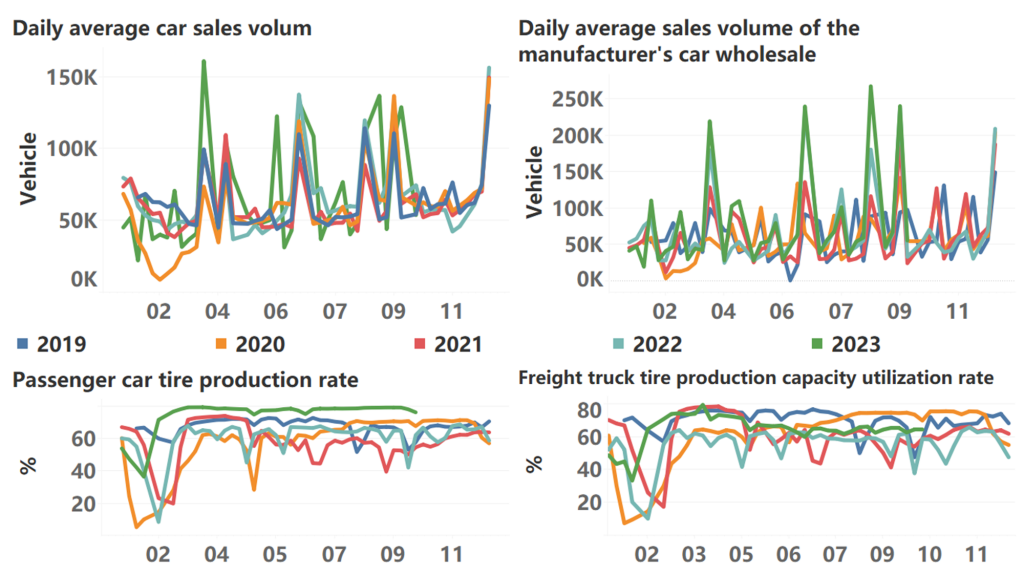

The following are high-frequency data for this week:

*Translated by ChatGPT