Federal Reserve

This week, the Federal Reserve’s interest rate meeting sent out two signals: pausing the rate hike for September, but not ruling out the possibility of continuing to raise rates this year. The market sees this as a hawkish pause, with September’s dot plot compared to June showing an upward adjustment of rates in 2024, indicating that the timing of rate cuts in 2024 will be delayed and the number of rate cuts will decrease. After the information was released, both the Dow Jones and Nasdaq fell, while US Treasury yields rose across the board. Besides the dot plot, the Federal Reserve also released quarterly forecasts for the US economy, raising the GDP growth rate for 2023. Powell mentioned in the press conference that the real interest rates are now positive, which should have a restrictive impact on the economy. However, the strong performance on the demand side exceeded everyone’s expectations. All signs indicate that the Federal Reserve has enough confidence to raise interest rates again, and mentioned three risk points in the press conference:

- Rising oil prices

- Strikes

- Federal government shutdown Powell believes that these three factors are not enough to affect the prospects of a soft landing in the US, something we had noticed in our last report with the rise of both oil prices and the dollar index. Currently, the dollar index has risen to its highest point since March 2023, and this week on Wednesday, Thursday, and Friday US time, the Nasdaq index underwent a deep adjustment, seeming to have hit the bottom. The window for shorting the dollar and going long on Nasdaq seems to have arrived.

State Council Policy Routine Press Conference

At the State Council Policy Routine Press Conference held by several department heads on September 20, it was mentioned that since August, relevant parties have continued to optimize a batch of phased policies, researched and launched a batch of highly targeted new measures, and actively planned a batch of reserve policies, forming a set of policy “combinations” to effectively stabilize growth, boost confidence, prevent risks, and continuously consolidate the positive momentum of our country’s economic recovery. Data from August shows that consumption and manufacturing investment have picked up, the price monetary environment has improved, and this week is the first week after all the data for August has been disclosed, with the overall financial market environment being quite complex. To judge the continuity of the economy in August, the real estate issue remains central. Currently, the debt related to real estate (standard debt facing restructuring pressure, non-standard debt showing triangular debt relationships) is in focus. From the pace of central regulation, it seems that a firm decision has been made to let both the creditors and debtors of related debts share the losses, rather than having a large fiscal stimulus. Since the political bureau meeting on 7.24, relevant policies on real estate regulation have been gradually relaxed, but the lag in policy timing seems to be a fairly long process, and the authorities have enough patience to wait for the results of the restructuring between debtors and creditors. The pace at which the panic in the real estate sector is spreading to the overall economy seems to have been controlled, and if real estate prices cannot stabilize, the residential sector will not leverage up.

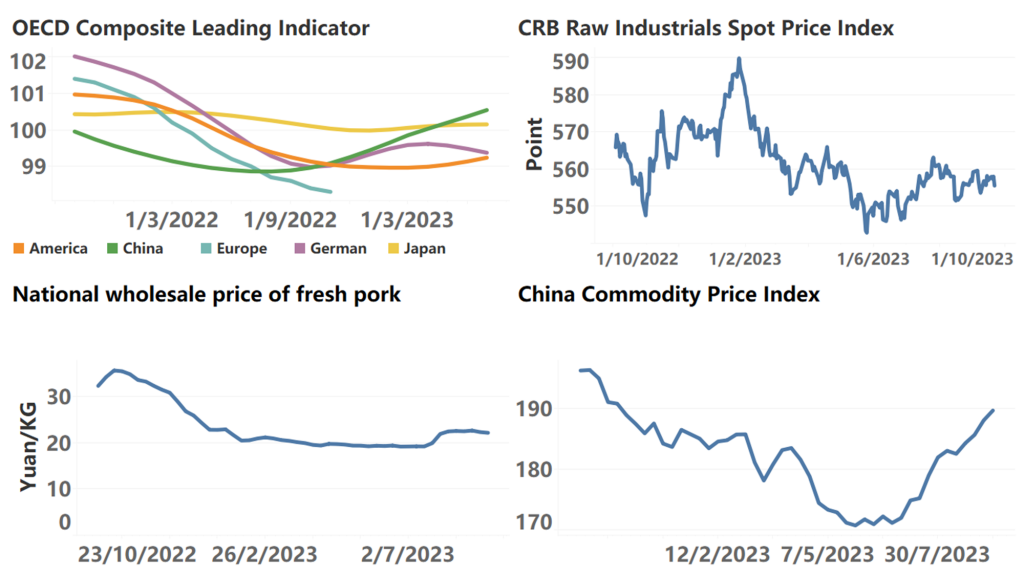

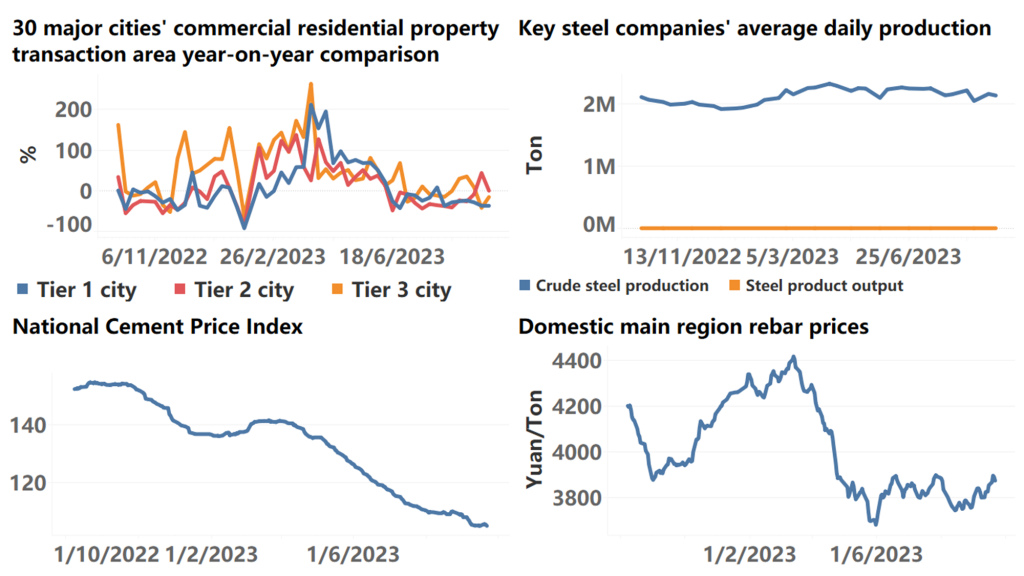

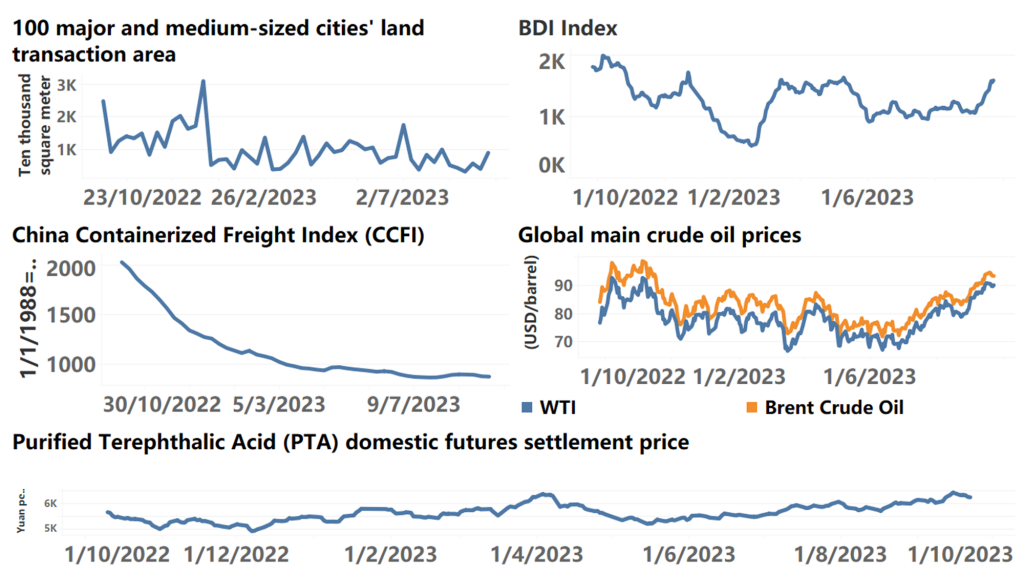

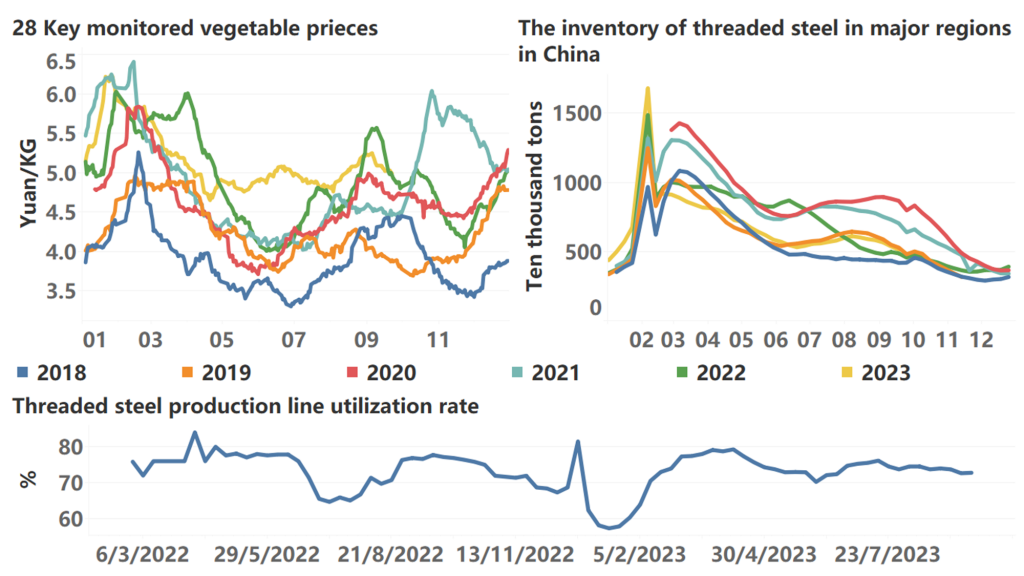

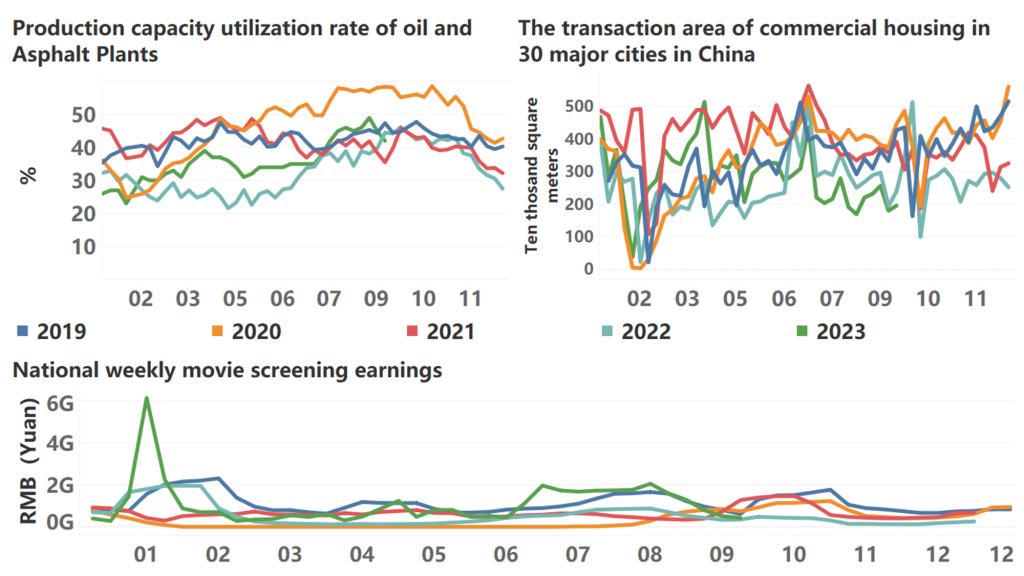

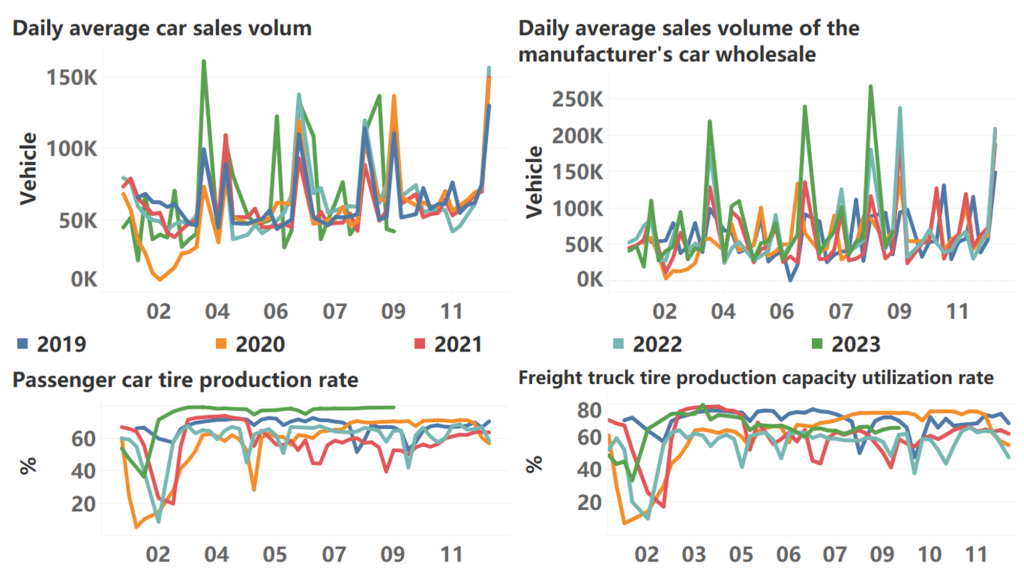

The following are high-frequency data for this week:

*Translated by ChatGPT