China’s Inflation, Social Financing, M2

July’s CPI YoY (year-on-year) is -0.3%, previous value 0%; core CPI YoY is 0.8%, previous value 0.4%; PPI YoY is -4.4%, previous value -5.4%. The new credit and social financing in July did not continue the expansion trend of June, both YoY and MoM (month-on-month) significantly decreased. Among them, new RMB loans amounted to 3.459 trillion yuan, the lowest single month since November 2009; new social financing was 5.282 trillion yuan, the lowest level since July 2016. Structurally, July continued to show the characteristic of “strong businesses, weak residents”. However, both business and personal loans shrank YoY. The momentum of growth in long-term business loans weakened, and the pressure on the resident end significantly increased, with bills financing and non-bank loans becoming the key supports for the month.

July M2 YoY grew by 10.7%, a speed that is 0.6 and 1.3 percentage points lower than the end of the previous month and the same period of the previous year, respectively, marking the lowest since May 2022. The M2-M1 spread further expanded to 8.4%. Even considering seasonal effects and the rapid pace of previous credit issuance, the growth rates of social financing and M2 still slid beyond expectations. The SSE (Shanghai Stock Exchange) Composite Index also saw a sharp decline on August 11. As of now, the price and currency data in the major economic data for July have been disclosed, and external demand data such as imports and exports have also been released. Next week, internal demand data like retail sales and investment will also be made public. Judging from the price-money trend, the July domestic demand data is expected to be unsatisfactory, which may depress investor sentiment in the short term. The upward fluctuation of the PMI (Purchasing Managers’ Index) temporarily soothed investor sentiment, but this positive factor is now hard to maintain.

Overall, data on prices in the economy has entered negative growth territory, and the growth rate of monetary demand and supply exceeded expectations, which indicates that the risk of economic deflation is on the rise. We’ve repeatedly emphasized in previous reports that deflation won’t disappear on its own; it’s typically a market failure phenomenon dominated by debt (as mentioned in the reports “Huge Waves” and “Concerns About Structural Issues”). The evolution of deflation could lead to a minor recession or even more severe downturns, like the Great Depression of the 20th-30th centuries, Japan’s lost decade in the 1990s, and the global financial crisis around 2008. Scholars have derived numerous economic findings from studying these downturns, one consensus being that deflation is primarily a monetary phenomenon. The government can counteract this by easing monetary policies like interest rate cuts, quantitative easing, and MMT (Modern Monetary Theory). When choosing between tackling a crisis and its costs, the preference tends to lean towards “curing the disease first, then saving the person”, which forms a complete theoretical and philosophical system. Currently, the deflationary cycle risk between China’s CPI and money is escalating. Without regulating this cycle, the following two issues may remain unresolved:

- Reforming China’s old real estate model and establishing a new one.

- Stability of the RMB exchange rate. For these two issues, we’ve discussed and reminded everyone numerous times in previous reports about their decisive factors for asset prices. Asset prices reflect anticipations, influenced not only by the latest disclosed data but also the market’s expectations on deflationary prospects. Investors should pay attention and be part of this game. The evolution of China’s real estate dilemma seems not to have seen substantial improvement, and the process of balance sheet contraction continues. Evergrande’s delay in paying its U.S. bonds, despite its official statement about encountering a temporary liquidity predicament, has conveyed a super pessimistic message to the market. Intuitively, liquidity issues in real estate companies should evolve from smaller to larger companies. Now, if the top companies are facing problems, the issues in smaller companies will only be more severe. Furthermore, as a leader in commercial real estate, Wanda also encountered liquidity difficulties.

We’ve also mentioned the stability of the RMB exchange rate more than once. If asset prices valued in RMB decline across the board, the investment value of the RMB itself will also fall, making it hard for the exchange rate to remain stable. We had emphasized the importance of stabilizing the RMB exchange rate when the USD/RMB exchange rate was around 7.1. After two rounds of adjustments, the RMB remains in a weak position.

Both of these tough problems should be discussed under the overarching frame of deflation. Once the risk of deflation is addressed, the aforementioned issues can be solved more easily.

U.S. Inflation The U.S. CPI for July YoY increased by 3.2%, slightly below the market expectation of 3.3%, with a previous value of 3%. The U.S. core CPI for July YoY increased by 4.7%, slightly below the market expectation of 4.8%, with a previous value of 4.8%. Market expectations for the Fed to stop raising interest rates in 2023 are growing stronger. A new development in the U.S. economy is the intensification of labor wage negotiations, which brings certain uncertainties to the future development of the U.S. economy, warranting our continued attention.

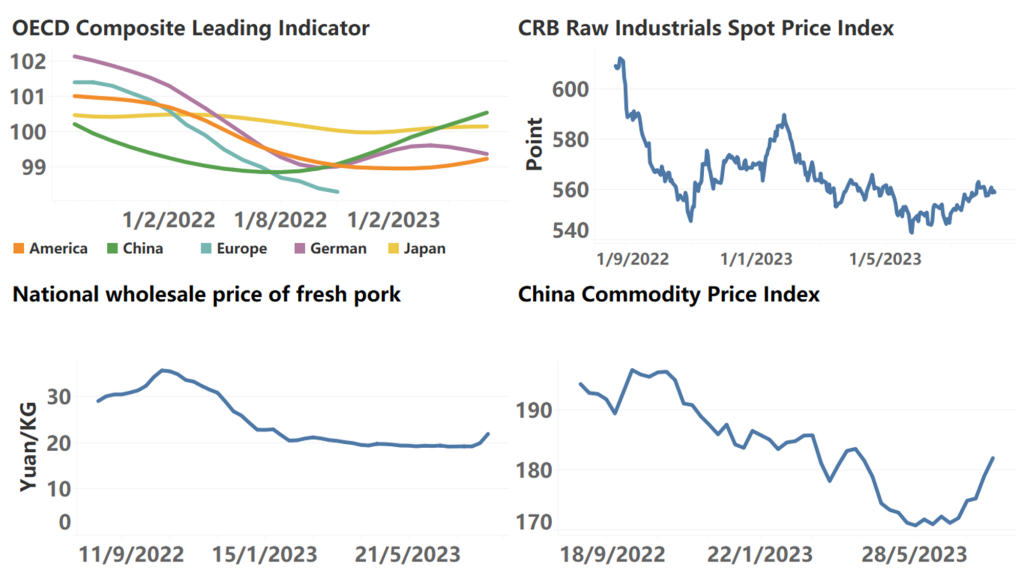

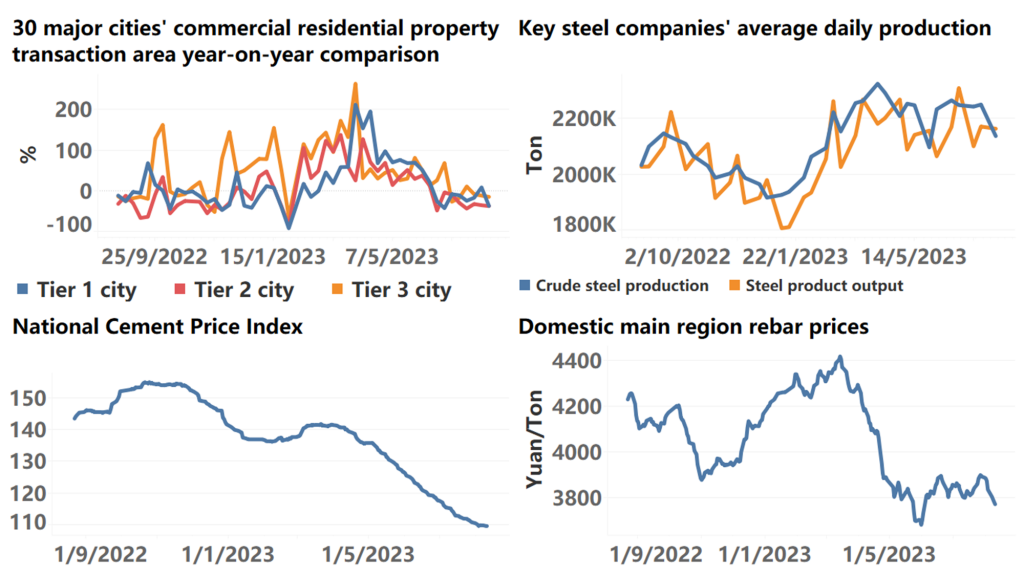

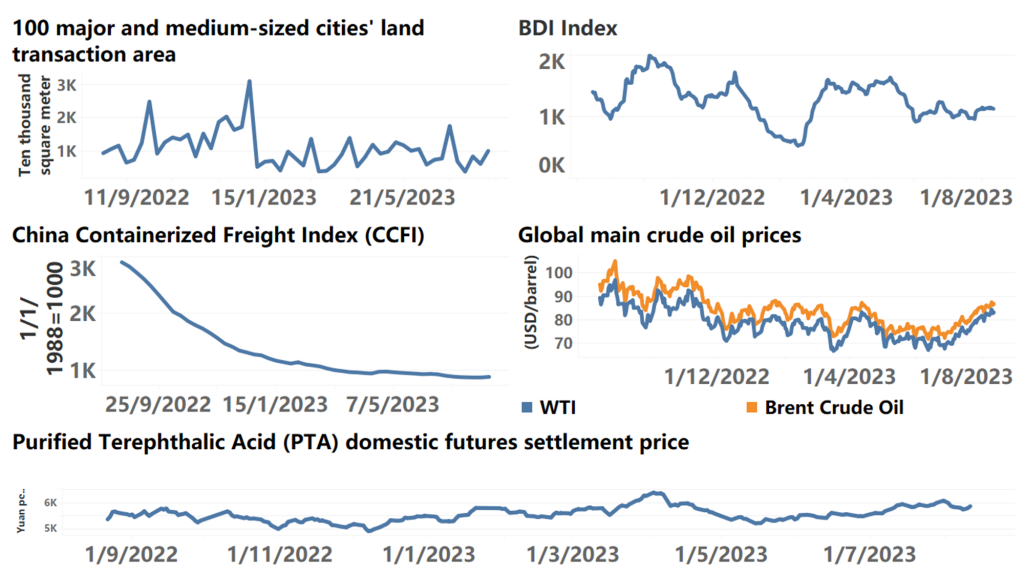

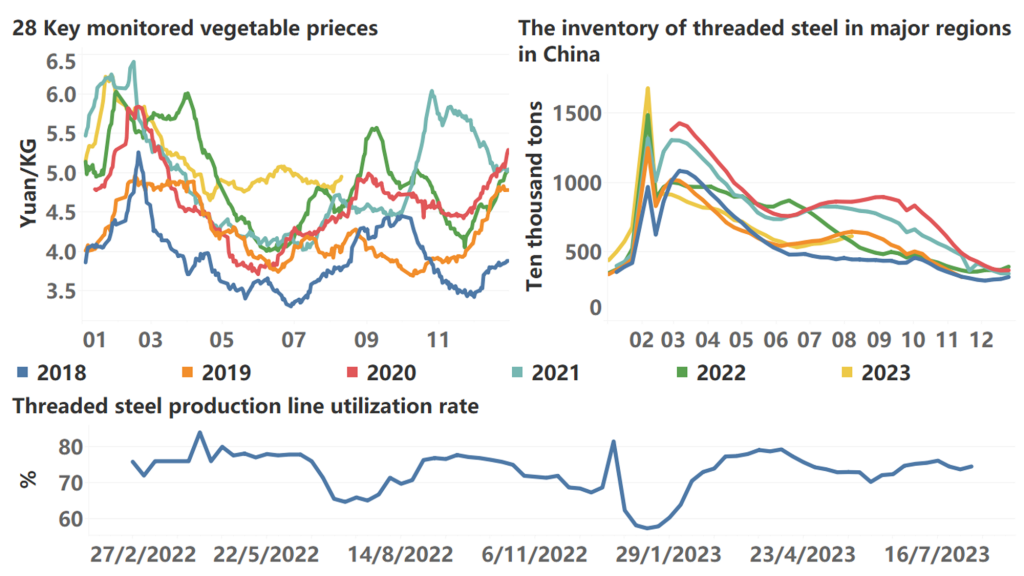

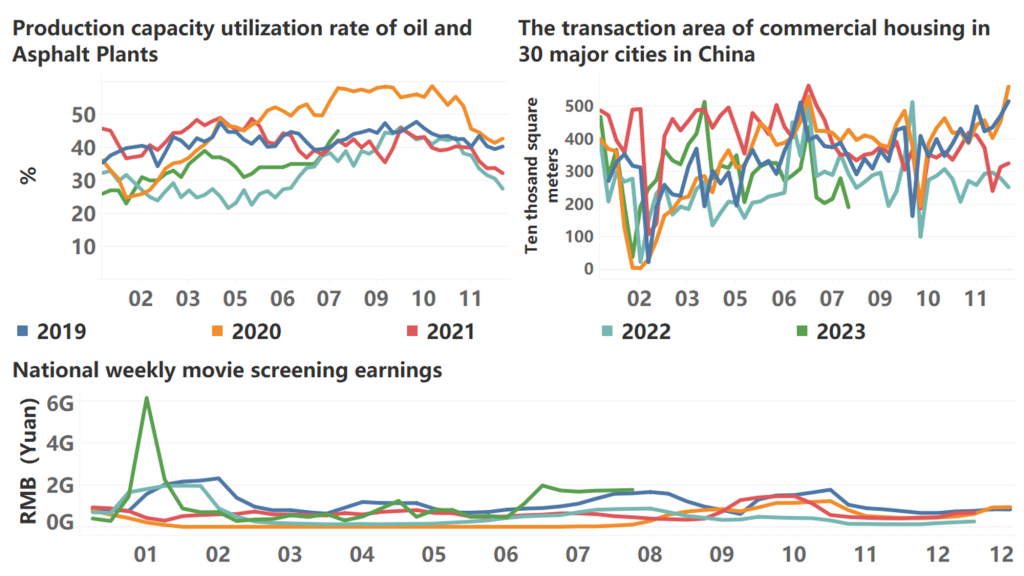

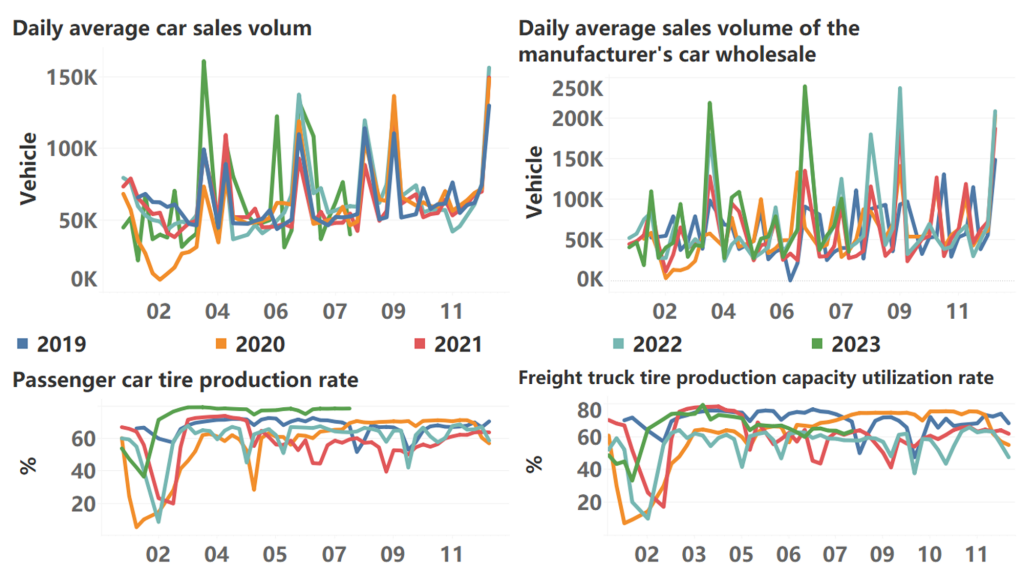

The following are high-frequency data for this week:

*Translated by ChatGPT