Yi Gang: Monetization of Assets

The Chinese economy is a continuous process of industrialization, where assets are slowly moving from fixed assets to more liquid assets (financial assets). In the process of trading and storing financial assets, a lot of money will be naturally derived, which leads to the faster growth of China’s money supply relative to countries at the same development stage. The policy point derived from this is: the money supply growth matches the economic growth and inflation level. In numerical terms, the growth rate of M2 surpasses the growth rate of GDP + CPI to some extent.

So, after the baton of the central bank governor passed from Yi Gang to Pan Gongsheng, is this view still the most fundamental equation of monetary policy? For the Fed, the Taylor Rule might be its core equation. What is the equation for China’s monetary policy next? There is not an official statement yet. The goal of maintaining a stable exchange rate within a reasonable and balanced range will not change.

The U.S. Debt Issue

On August 1st local time, Fitch Ratings announced a downgrade of U.S. credit ratings from “AAA” to “AA+”. Fitch pointed out that the U.S. government’s debt burden is high and increasing, and it is expected that the U.S.’s fiscal situation will continue to deteriorate over the next three years. On August 1st local time, U.S. Treasury Secretary Janet Yellen issued a statement on the Treasury Department’s official website regarding Fitch’s latest rating decision. Yellen responded, “I strongly disagree with Fitch’s rating decision. The rating adjustment announced by Fitch today is arbitrary and based on outdated data. Fitch’s quantitative rating model has significantly declined between 2018 and 2020.”

After this announcement, both Dow Jones and NASDAQ experienced some pullbacks, clearly impacting investor sentiment. This news is more about long-term development issues in the U.S.: The risk of U.S. debt default is gradually increasing, the price of U.S. Treasury bonds as an investment will decrease, yields will increase, and the proportion in international reserves will decrease. Therefore, the long-term risks in the U.S. come from two aspects:

- The debate between the two U.S. parties about the debt ceiling will become more intense. However, neither party will genuinely gamble on the U.S. defaulting on its debt, as neither party can bear the political cost. But the volatility of U.S. debt will indeed increase, in other words, U.S. debt no longer reflects a risk-free yield, but also includes the risk premium of a default event. Therefore, for investors, the value of this asset should accordingly decrease, from this perspective, the downgrade makes sense.

- The ratio of U.S. fiscal income to expenditure is gradually becoming unbalanced. In dealing with medium-term challenges, such as rising social security and health insurance costs due to aging population, progress has been limited. The two parties are competing to expand welfare expenditures in their race to build American social welfare systems, and U.S. fiscal revenue is tied to corporate tax, another area where the two parties compete fiercely.

U.S. Recession

The above mainly discusses the long-term risks of the U.S. Recently, discussions about the U.S. encountering a slight recession in the fourth quarter of this year or the first quarter of next year have gradually heated up. This is reflected in the recent downward volatility of U.S. stocks, with two observations that are quite accurate: 1) U.S. job vacancy data is falling beyond expectations, and layoffs in the U.S. tech industry are continuously expanding. The long-lag effect of monetary policy is gradually becoming evident. 2) The current strong consumption is due to resident savings accumulated from previous quantitative easing. From the current situation, the portion of fourth-quarter resident savings from easing policies will gradually clear, and consumption data will fall back.

As the soft landing of the U.S. economy becomes more and more likely, a slight recession becomes the focus of everyone’s discussion. The degree of this recession will interact with the Federal Reserve’s actions, ultimately determining asset prices. How great the risk is in the fourth quarter requires continuous observation.

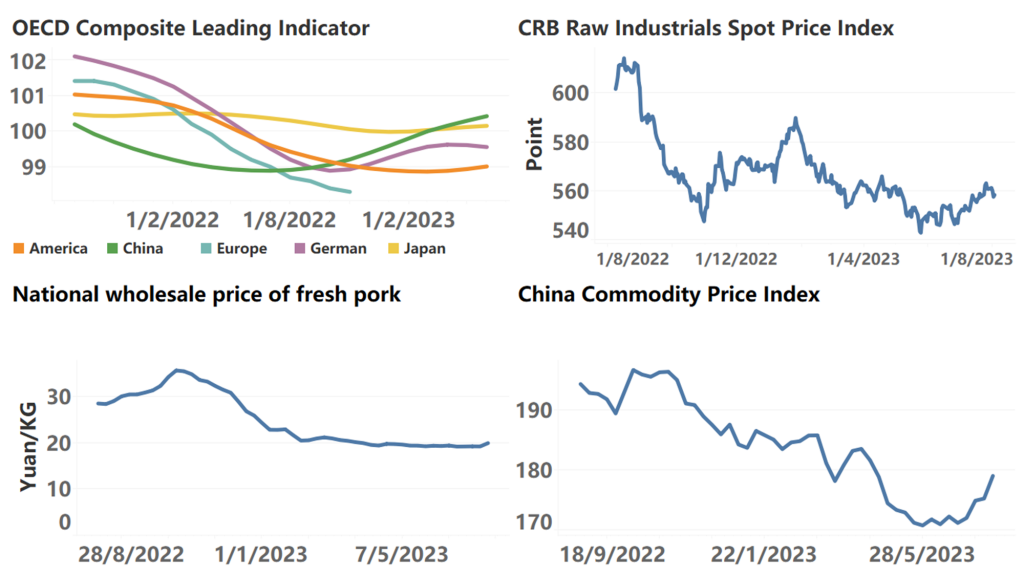

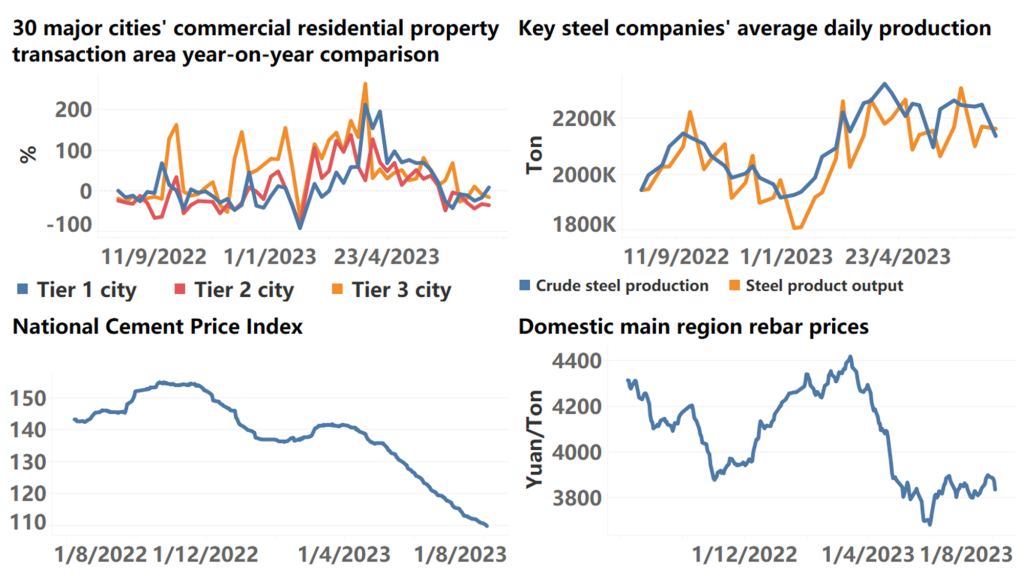

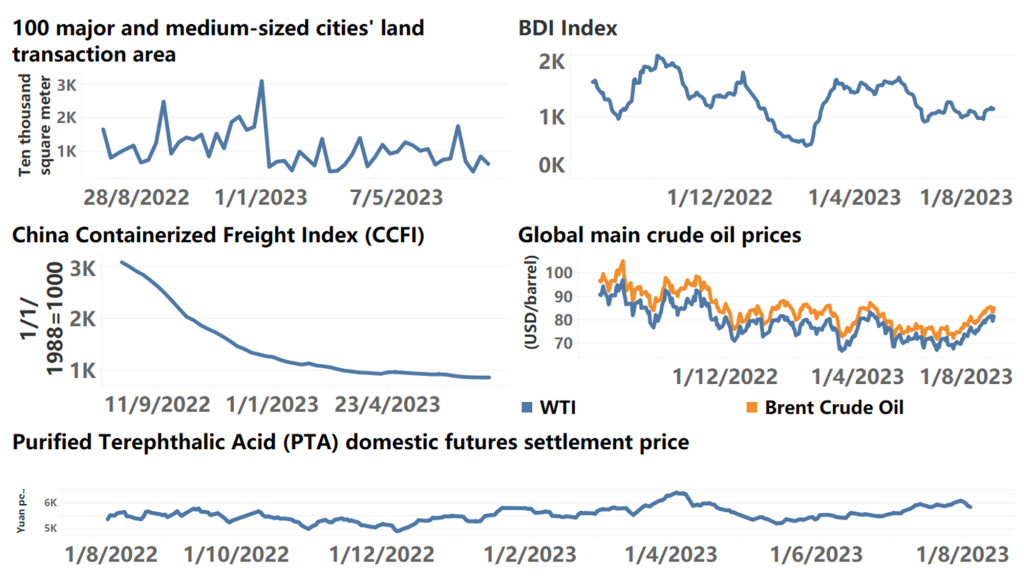

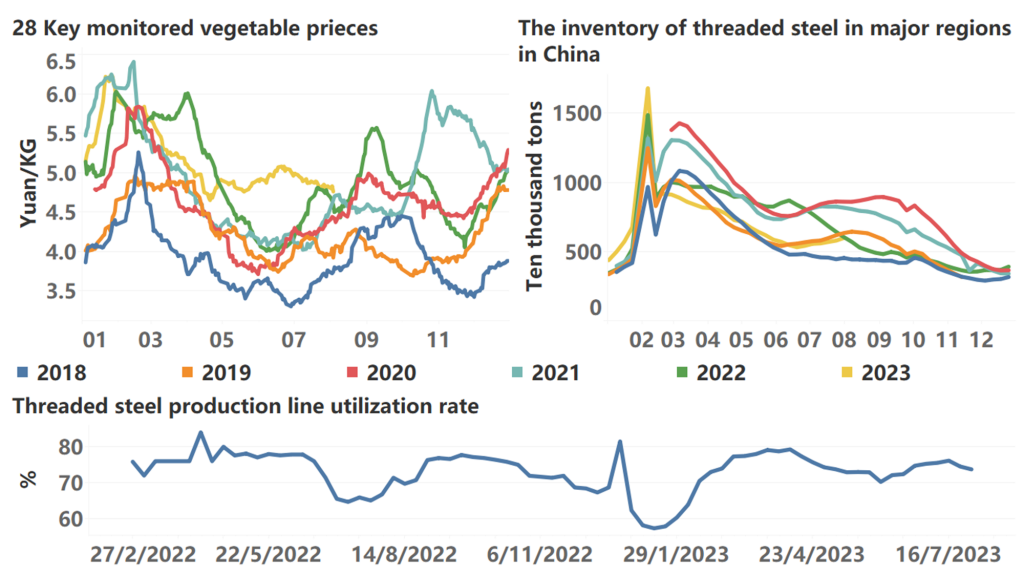

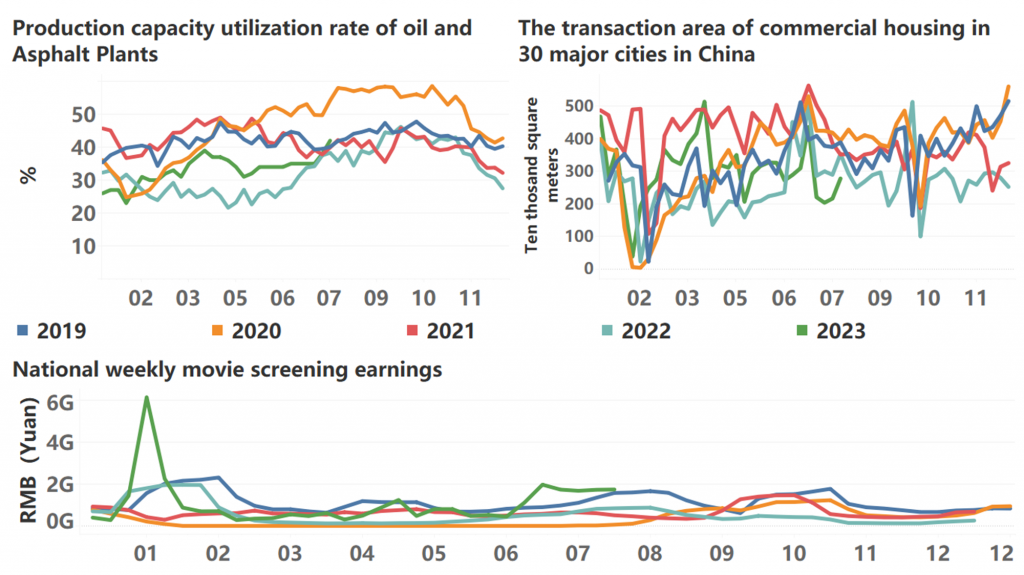

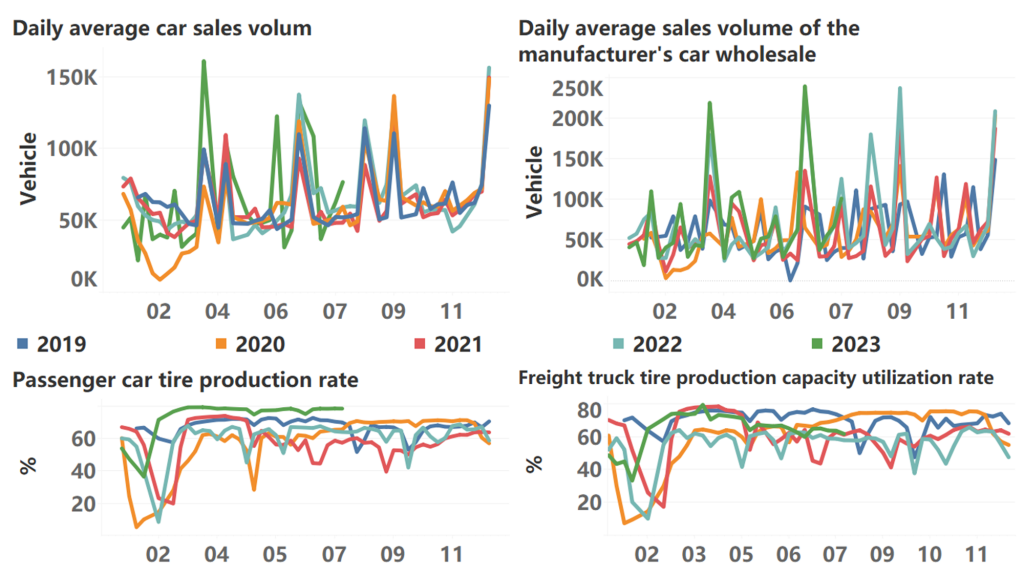

The following are high-frequency data for this week:

*Translated by ChatGPT