We didn’t see a few issues correctly.

First, the relative relationship between the Dow Jones and the Nasdaq. The Dow Jones experienced 13 consecutive rises, but the Nasdaq performed mediocrely, mainly because the tech industry relies heavily on financing. It needs high valuations to support its financing. Tightening financial conditions have suppressed its rise. Second, the Hang Seng Index performed stronger than the Nikkei this week. After the Nikkei ended its previous rapid rise, it clearly entered a fluctuation stage. The Hang Seng performed outstandingly beyond our expectations this week. The possibility is that under the leadership of Dow Jones, the Nikkei is relatively weak, and the market has already priced the basic situation of the Japanese economy. Next, we need to keep an eye on the upcoming disclosure of Japan’s GDP data. Third, the relative relationship between gold, oil, and the dollar. Last week, the prices of these three assets all rose together, which does not conform to the typical recession trading logic, and the price difference between New York gold and London gold is obviously widening. Our previous judgment was that with the exit of the “recession trade” mainline, gold prices would gradually correct, but gold prices were very strong this week. One possible explanation is that the “recession trade” has turned from the United States to other emerging markets.

Federal Reserve

On July 27, the Federal Reserve raised interest rates by 25 basis points as expected, and threw out signals that it might pause rate hikes in September. According to the latest US GDP disclosure, the first quarter grew by 2%, and the second quarter by 2.4%. Just from the perspective of GDP, the impact of high interest rate policies on the economy seems limited, and the soft landing scenario is becoming more likely. The IMF predicted in July that the US GDP growth rate for 2023 would be 1.8%, which means the third and fourth quarters would fall to around 1.4%. The Federal Reserve’s signal of a possible pause in rate hikes may be the long-lag proposed by Friedman, that is, the Federal Reserve is waiting for policy effects and feedback from macroeconomic data.

Increase in Capital Adequacy Ratio

At the same time as the Federal Reserve signaled a possible pause in rate hikes in September, the market also heard that the US regulatory authorities plan to ask the eight largest banks to increase their capital by 19%. In some ways, this news did not break out during the banking crisis. Its emergence now shows that the crisis in the US banking industry is basically over. The US is systematically adding some safety nets to its entire financial system. If investor sentiment recovers after inflation and soft economic landing, a huge amount of US dollar M2 may derive a very terrifying asset price performance. Increasing bank capital before this is a very sensible behavior.

Bank of Japan’s YCC

The market heard that the Bank of Japan will discuss the YCC position in the near future, and Kazunari Ueda also responded to market concerns. He expressed the meaning is still in the discussion stage. We think this is more a communication skill, guiding long-term market expectations by “talking”. Looking at Japan’s inflation performance, Japan’s New Normal needs Japanese inflation to be maintained for a while, and it cannot fall back too quickly to the previous state.

European Central Bank raises interest rates by 25 basis points

The European Central Bank followed the Federal Reserve’s pace to raise interest rates by 25 basis points. Relative to inflation in the European region, the power of 25 basis points may not be enough to limit the development of inflation. The current interest rate peak is still too low, and the possibility of a hard landing in the European region continues to rise.

Central Political Bureau Meeting

Deflation – asset prices, for nearly a month and a half, domestic asset prices have been continuously low. The real estate (price, trading volume) has continued to decline since the second quarter. The stock prices and trading volume have also fallen. The prices of bulk commodities have continued to be low since the beginning of the year. The CPI fell back to 0% in June, and the economy is moving towards quasi-deflation. In response to insufficient demand, the Central Political Bureau meeting was held on July 24, proposing: to expand income to increase consumption.

We believe that the July Central Political Bureau meeting can help the macro economy smoothly transition through the July-October stage, but large-scale stimulus policies will not appear before the Third Plenary Session. Two changes in direction in this meeting are relatively large, one is the real estate direction, the next real estate policy may undergo major changes, a series of adjustments such as down payment ratio, first loan interest rate, second-hand housing transaction commission will appear, the Ministry of Housing and Urban-Rural Development has already sent a clear signal at the meeting. However, we believe that the continued contraction of real estate companies and the difficulty of continuing the previous prosperity due to price factors and purchasing power on the resident side. The other is the capital market, to invigorate the capital market, which directly manifests as an increase in trading volume, and naturally supports the rise in asset prices when liquidity rises. If the performance of asset price increases is flat, it may require the power of institutions to increase this trading volume. The capital market has seen a large increase in the direction of real estate and securities companies.

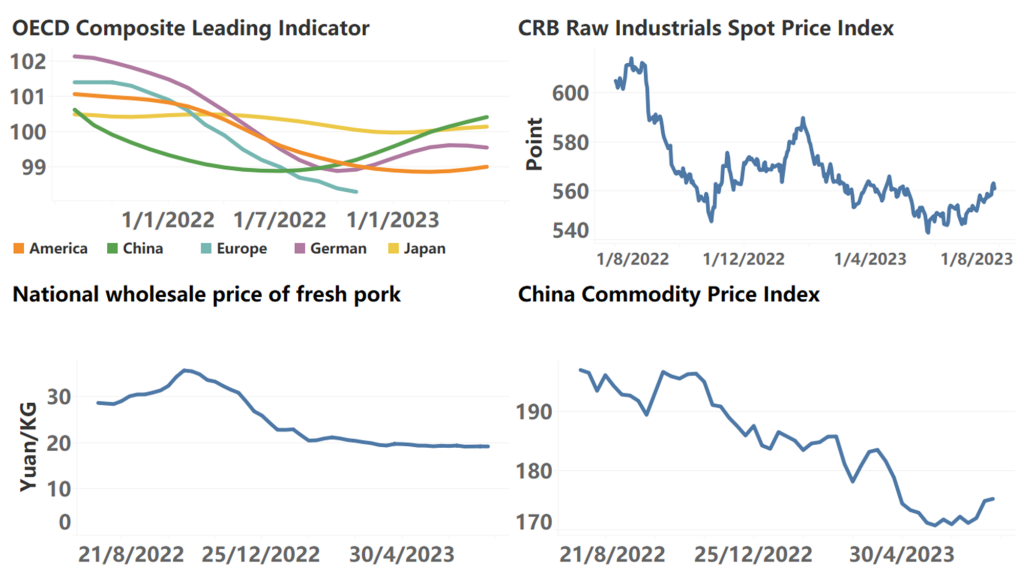

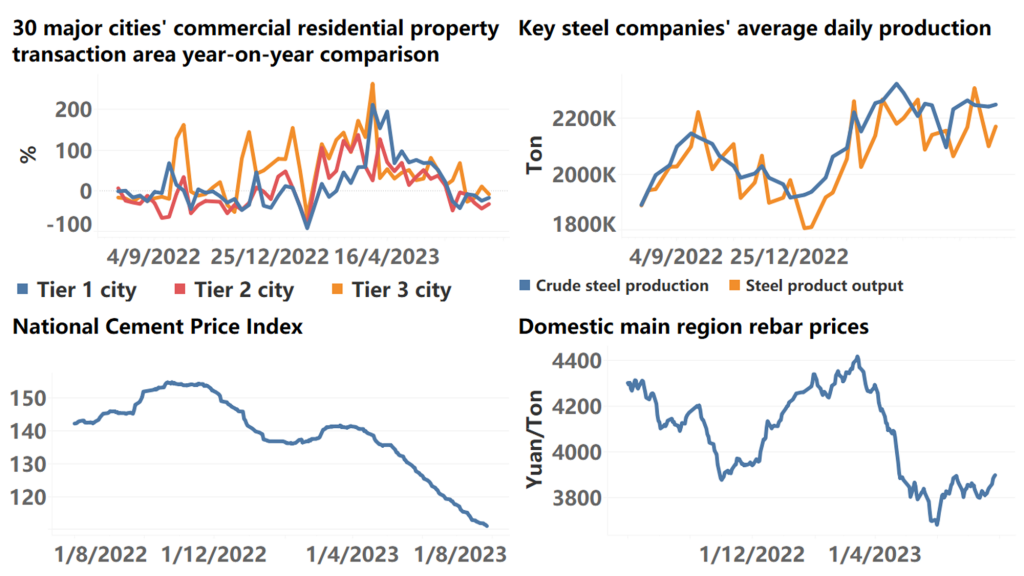

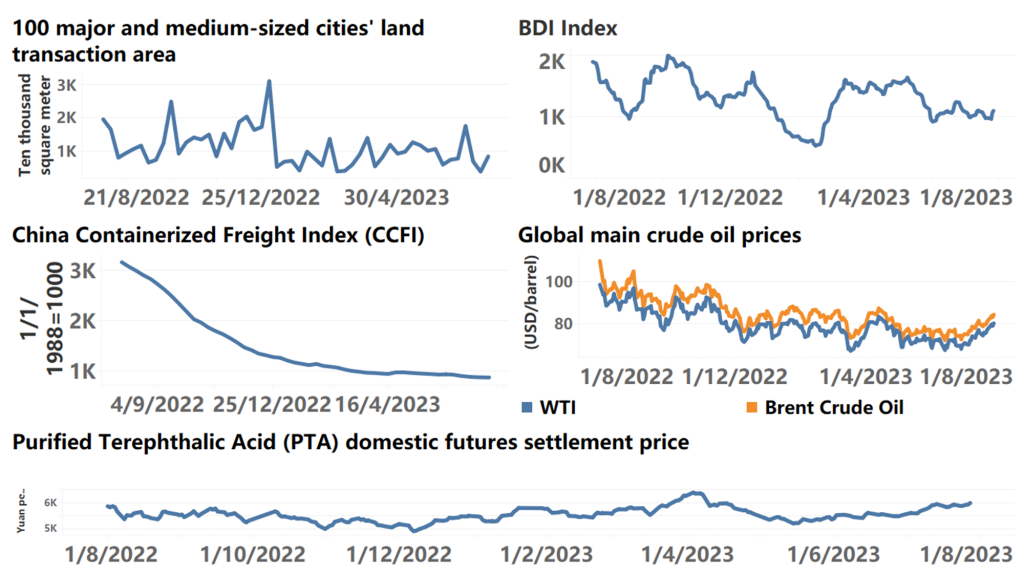

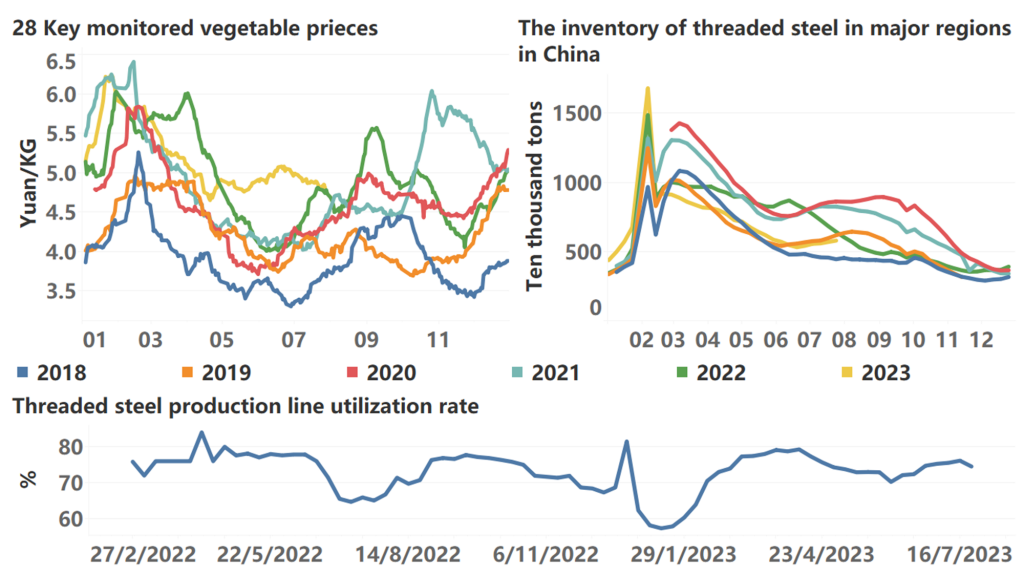

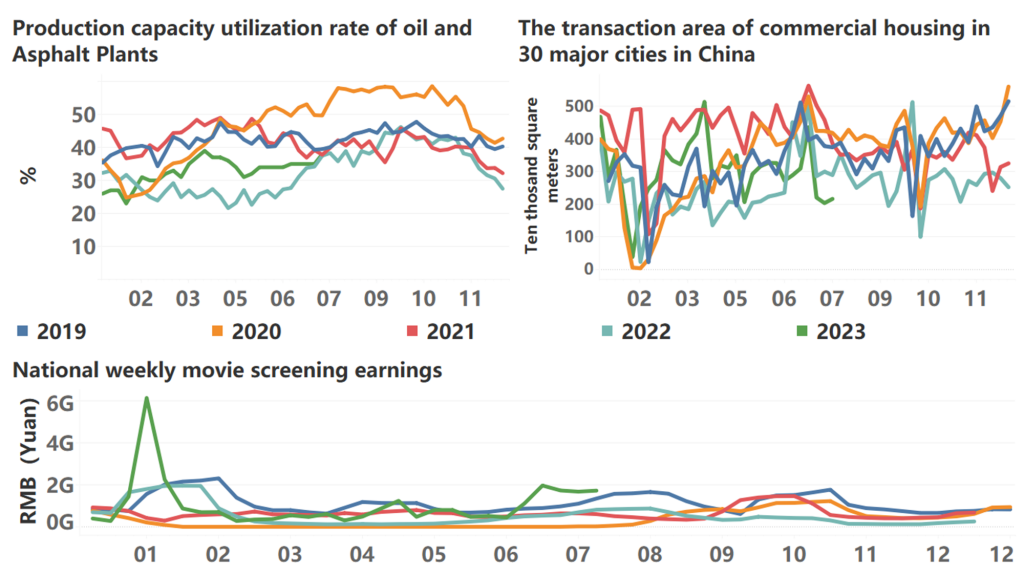

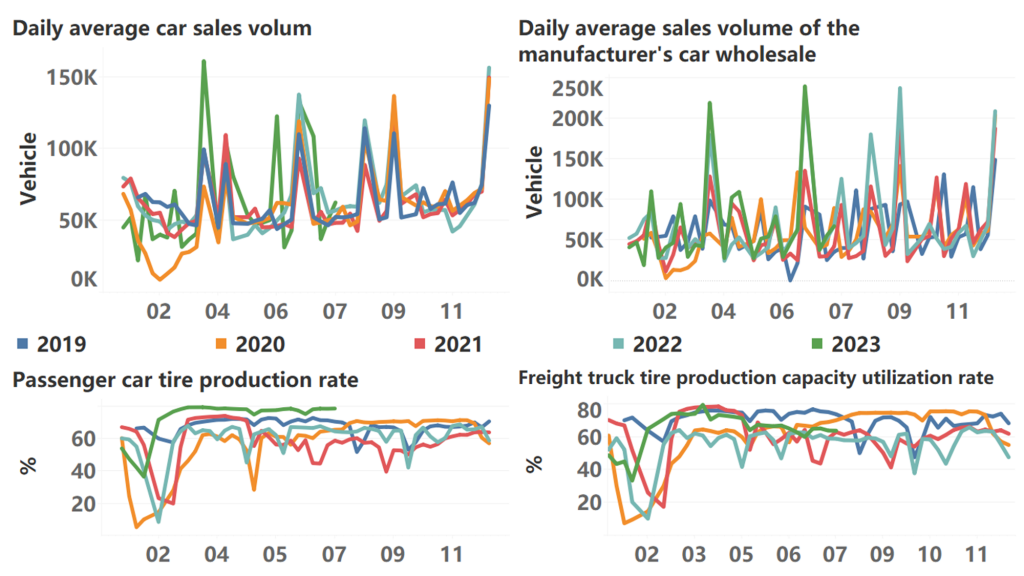

The following are high-frequency data for this week:

*Translated by ChatGPT