Markets

In the past two weeks, a rise and fall pattern has been observed in the global stock markets. Among them, the Hang Seng Index has seen a substantial pullback, the Nikkei seems to have ended its previous upward trend, and the Shanghai Composite Index is also on a downward trend. This fluctuation in asset prices is natural, progressing through ups and downs, but a structural differentiation has appeared in the simultaneous decline. Secondly, from the perspective of fundamentals and sentiment, US Q1 GDP YoY growth rate has been revised to 2%, European inflation remains high, and the global manufacturing PMI continues to decline. In particular, the June European manufacturing PMI was 45.4%, down 0.8 percentage points from the previous month, decreasing MoM for five consecutive months and remaining below 50% for 11 consecutive months, marking a new low since June 2020. The downward pressure currently faced by the Eurozone’s manufacturing industry has increased, and its economy has entered a technical recession. The Eurozone’s June composite PMI fell below the boom-bust line for the first time in six months. The fall of the Eurozone’s composite PMI below the boom-bust line for the first time should be a new signal. If it remains below 50 in July, the expectations of a European recession will be confirmed. This could be a significant blow to the global stock market. The global stock market return rate in July may experience substantial volatility due to this type of signal.

On the sentiment side, both the European Central Bank and Federal Reserve meetings indicate certainty in continuing to raise interest rates in the second half of the year. However, there are two interpretations of this ongoing rate hike in the market: Firstly, for the United States, the market believes this represents the Fed’s great confidence in the growth of the U.S. economy, and that even if the interest rate peak continues to increase by 25BP twice to reach 5.75%, the U.S. economy will still maintain its expansion. Powell expressed his confidence in the current state of US economic expansion in his speech at the meeting, so the market’s expectation of a 25BP rate hike in July is very clear. We also clearly stated in our last report that this is a standard scenario. It should be said that the global stock market has fully priced in this signal. Secondly, for Europe, inflation remains high, and there is a view in the market that Europe’s interest rate peak could reach 7%. Of course, this is an extreme view, but the market generally believes that Europe’s interest rate peak should be around 6%, which is obviously a very bad situation. That is to say, at each European Central Bank meeting in the second half of the year, there will be a rate hike, therefore, the time point when the European Central Bank first pauses the rate hike is the most important for the market. This expected time point should depend on the outlook for inflation and the situation of European economic recession. For investors, they should keep a close eye on the signs of European recession, dare to go long on Europe in the worst outlook for the European recession, and seize the investment opportunity when Europe pauses interest rate hikes.

The divergence between the United States and Europe indeed brings a lot of difficulties to judge the global stock market. The overall stock volatility in Europe continues to rise, but Nasdaq is still a relatively good investment opportunity.

After discussing the stock market, we will focus on the following directions:

- Crude oil

- Gold

- Renminbi exchange rate

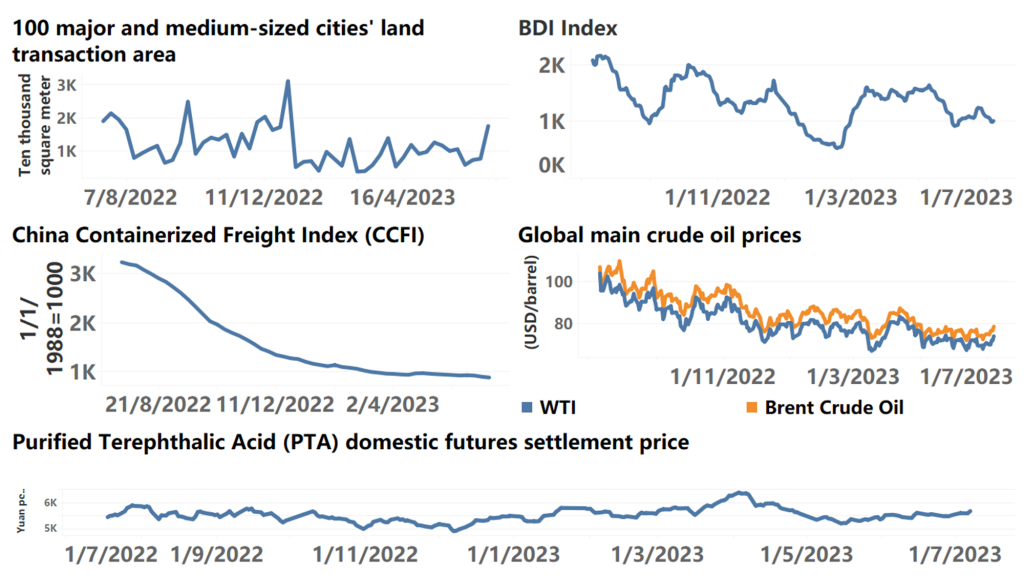

First, the Brent crude oil price remains around 75 dollars per barrel. We explicitly pointed out in our last report that in the context of modern monetary theory prevailing, the price of crude oil is a manifestation of the interests of all OPEC+ countries. The rise and fall of oil prices obviously do not conform to the interests of OPEC+ countries, which is why Russia has always criticized the outbreak of this big inflation as a result of policy errors in the West. Therefore, even if the prospect of recession continues to intensify and the expectation of the interest rate peak continues to rise, shorting crude oil prices is not a wise choice. The price of crude oil more reflects a national game and it is impossible to read the expectations of global total demand and supply from it. Recently, Saudi Arabia announced on July 3rd that it would extend the measure of voluntarily reducing oil production by one million barrels per day to August. Russia also announced on July 3rd that it would reduce daily oil exports by 500,000 barrels to the global market in August to ensure market balance.

In addition, the global reemergence of El Niño phenomenon has led to global high temperatures and a continuous increase in demand for electricity. Against the backdrop of addressing global climate change, the contradictions between traditional energy and new energy have become more prominent, which is also a major driver for the continuous rise of China’s photovoltaic and energy chemical sector. The background of climate change to some extent determines the long-term ceiling of crude oil prices. The significant increase in global investment in photovoltaics and wind power will impact the price of crude oil. However, in the short term, crude oil is still the world’s main energy source. The relative prices between crude oil, coal, natural gas and photovoltaic raw materials may undergo trend changes, and the price of a single crude oil may not represent the changes in the overall energy market prices. Even if Brent crude oil prices are relatively stable, coal prices may see a huge increase.

Second, gold is gradually declining. We clearly pointed out in our report two weeks ago that the inflection point of gold’s decline had appeared, and indeed, the price of gold has been gradually falling in reality. There are mainly three factors: 1) Global recession trading, 2) The strength of gold relative to the dollar index, 3) The demand of global central banks for gold reserves.Firstly, the U.S. economy has shown a strong expansion trend, with a year-on-year GDP growth rate of 2% in the first quarter, weakening recession expectations. In the next half year, the probability of a soft landing for the economy is continuously strengthening. Even if the U.S. economy goes down, it will likely be a shallow dip. China’s PMI has fallen below 50 temporarily, and it is highly probable that large-scale macro-control policies will be introduced in the second half of the year. The economic prospects of the world’s first and second largest economies are gradually becoming clear, which obviously suppresses the global recession trade and suppresses the price of gold. Secondly, the dollar index has strengthened, and despite market expectations that the Euro and the pound will surpass the dollar with substantial interest rate hikes, the dollar index remains strong, which is unimaginable. This indicates that the dollar’s position as a global reserve currency is still hard to shake, and gold is thus relatively weak. Finally, if central banks globally hoard gold on a large scale against the backdrop of a strong dollar, it will result in short-term asset depreciation.

Thirdly, the RMB exchange rate is gradually weakening. We emphasized as early as May that we should pay attention to the trend of the RMB exchange rate. A weak RMB can hardly support a strong domestic capital market performance. In previous analyses, we mentioned that some believed this was dominated by seasonal factors, but now it appears that the weakening of the RMB exchange rate clearly has the herding effect of financial asset prices and panic devaluation expectations have arisen, with reports even claiming that the RMB will depreciate to more than 7.3. Asset prices always show a stop-and-go trend. Continuous depreciation of the RMB cannot be the norm, but it also faces some challenges: The current RMB price relative to the U.S. dollar should have fully priced in the Federal Reserve’s July interest rate hike of 25 BP. After the next round of rate hikes, the pressure on the RMB relative to the U.S. dollar may decrease, but there is still 25 BP of pressure waiting. The weakening of China’s PMI has suppressed investor confidence. Subsequently, a package of stimulus policies will to some extent alleviate the pressure of the RMB relative to the U.S. dollar. We should continue to monitor the fluctuations in the PMI.

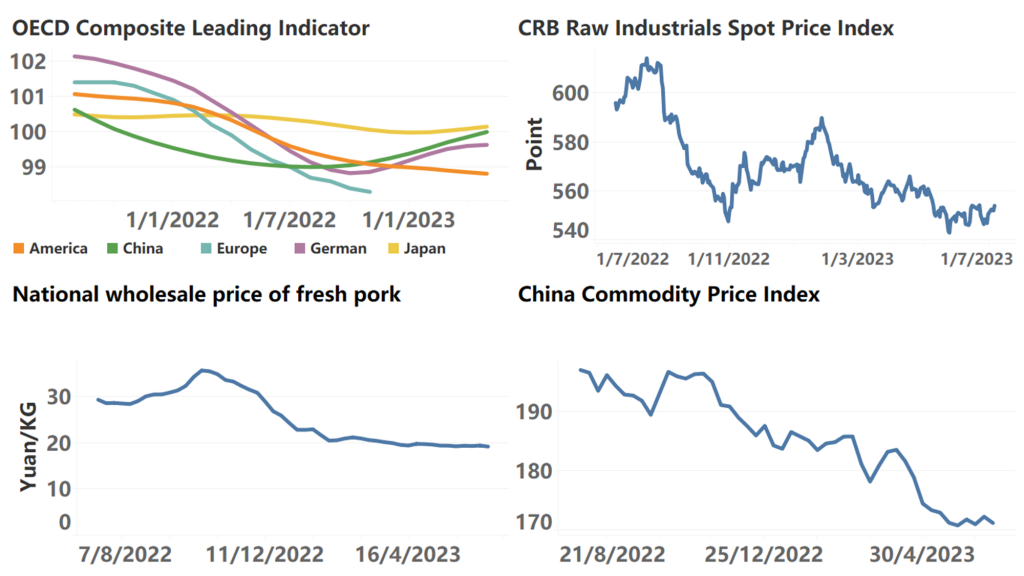

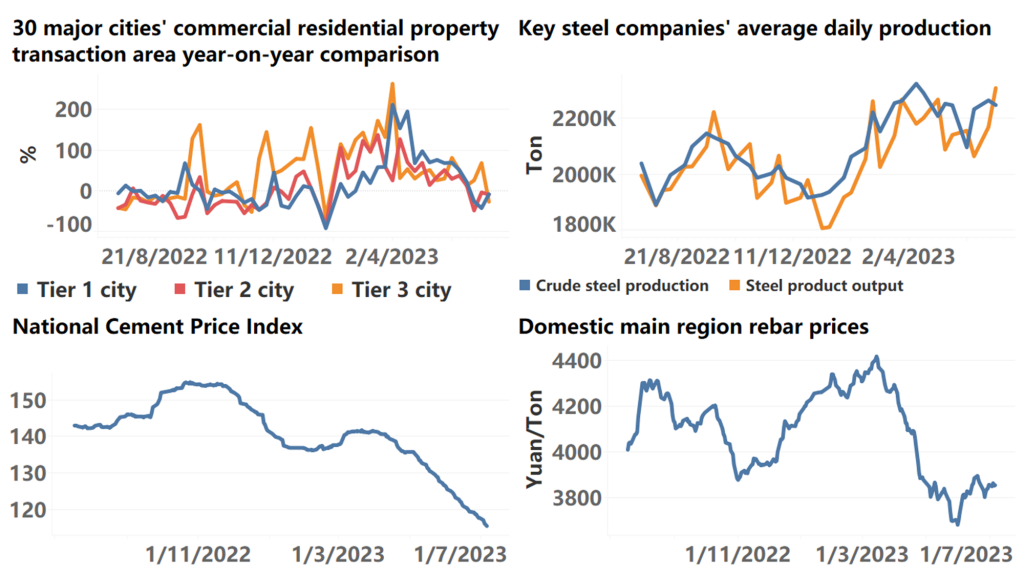

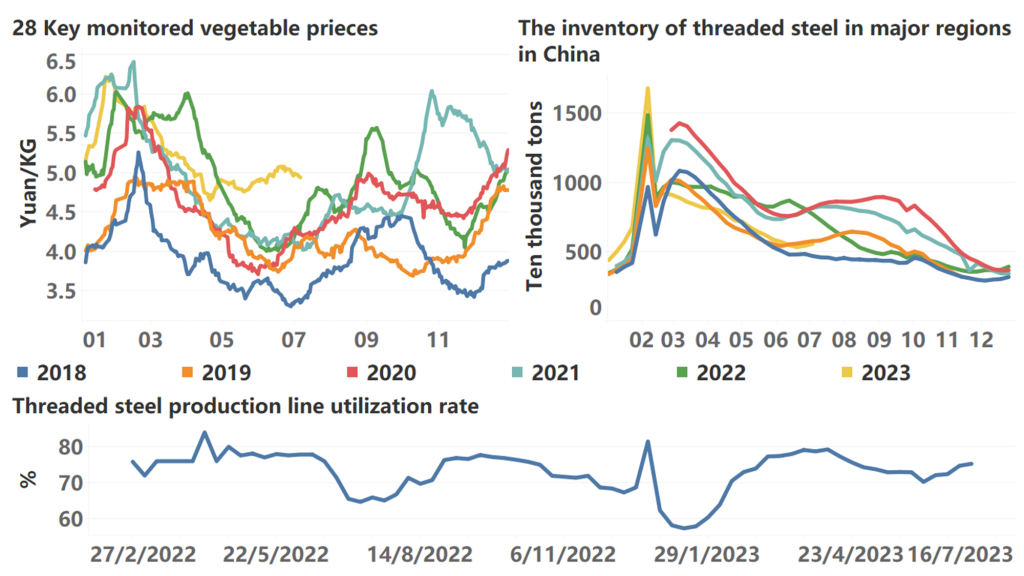

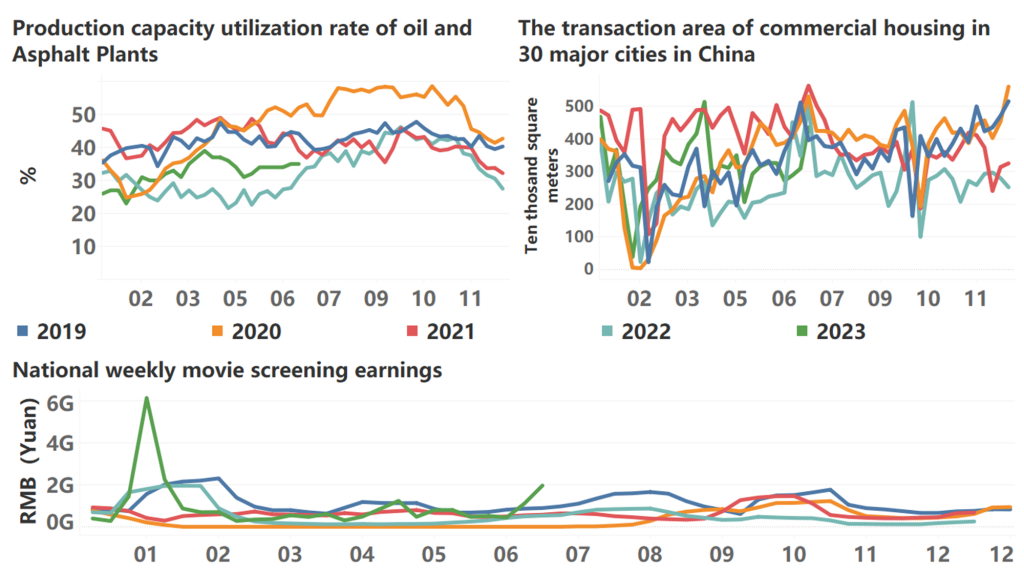

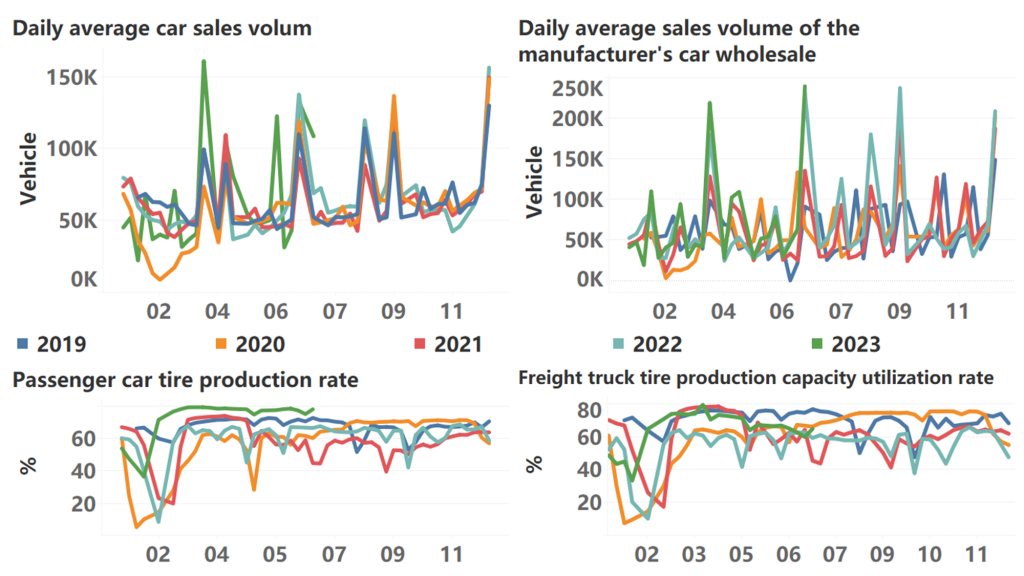

The following are high-frequency data for this week:

*Translated by ChatGPT