Skipping Interest Rate Hikes

On June 15th, the Federal Reserve’s interest rate meeting, in line with market expectations, did not choose to raise interest rates. The US CPI fell to 4% in May, a decrease of 0.9 percentage points, but the decline in the core CPI was slower, recording 5.3%, a drop of 0.1 percentage points. The PPI fell to 1.1, mainly due to the rapid fall in gasoline prices. At present, the Northern Hemisphere is in summer, and future energy prices may rise in the third and fourth quarters, which may affect the speed of the CPI’s fall. If the core remains around 5.3 and is difficult to fall, the Federal Reserve’s target interest rate – core inflation is a negative interest rate, which basically means that the Federal Reserve will continue to raise interest rates until the two are approaching. Because when the result is a negative interest rate, current consumption is more cost-effective, and demand will not be suppressed.

Looking at the relative position of the Nasdaq, the current position is very low, conveying the message that there is still danger at the high level of core inflation. If the fall rate exceeds 0.2 next month, then the Nasdaq will have the conditions to be bullish. Our previous view was not to short the Dow Jones, and indeed, it has been rising. We can ask a question: What is the prospect of the Western economy? There were three paths: hard landing, soft landing with high interest rates, and proper soft landing with high interest rates. The current data is increasingly leaning towards a proper soft landing with high interest rates, in which case, it has brewed expectations for a global stock market rise.

- The current risks are as follows:

- The wave of defaults on US commercial real estate loans spreads to the economy through the banking system;

- Europe’s inflation is not as ideal as the US, causing it to be unable to stop raising interest rates, and the European economy may continue to shrink, with the UK and Germany continuously technically receding, which may bring about debt issues;

- The Russo-Ukrainian war continued in the winter of 2023, causing commodity prices to remain high; Based on our previous triangle relationship between financial stability, economic growth, and employment, before the above three risks are clearly disclosed, the overall financial market should still be booming. We need to emphasize here that in the long run, both commodity prices and wages are sticky. Compared with the pre-pandemic period, prices in the global economy have risen by more than 30%, and these rising prices will not fall back. Therefore, when the economic recession passes through the bottom, the total demand of the whole society recovers to its original position. Compared with the current price, the new equilibrium point may be more than 30% higher than the original equilibrium point. In other words, the global capital market may have a growth space of 30%. Japan is a very typical fact, because asset prices are calculated at current prices.

China cuts interest rates

This week, following the 10-basis-point cut in the seven-day reverse repo (OMO) operation rate and the standing lending facility (SLF) rate on June 13, the medium-term lending facility (MLF) rate was also cut by 10 basis points on the 15th. This sends a signal: faced with not very ideal macro data, government authorities should take a series of short-term stimulus measures in the coming time.

Looking at the trading volume of A-shares, this signal significantly improved the market sentiment, and the market trading volume once again stood above one trillion, and the following view on the Chinese economy can be analyzed on three levels:

- The trend of China’s macro data, such as CPI, M2, industrial added value, and social retail total

- The macro tools we can use

- The trend of the capital market

Second, for the second level, the short-term stimulus effect is difficult to drive long-term economic growth. China’s long-term reforms have their specific political nodes. From the timeline, it may exist in the Central Political Bureau meeting in July and the Third Plenary Session in October. The stimulus policy in July must help the macro economy to tide over the downward pressure from July to October.

First, for the first level, we believe that the macro data for June are likely not optimistic. Here we propose two academic viewpoints: one is the Keynesian school, which believes that the recession of the economy mainly comes from the lack of demand, and expansionary fiscal policy should be used to stimulate the total demand in the economy. The second is the monetarist school, which believes that insufficient credit expansion and efficiency decline in the financial system have caused the economy to continue to deflate, and a loose monetary policy should be adopted. Observing the Chinese economy from the two schools, first of all, the main problem of the Chinese economy currently comes from real estate. The debt related to real estate is closely connected with local financing platforms. These financing platforms are difficult to bankrupt, so their assets are difficult to liquidate and balance. The market is difficult to clear, and it is difficult to solve the problem by adopting two types of stimulus policies. Short-term stimulation can stimulate CPI and M2 in the short term, but it is difficult to change the long-term trend.

Third, for the third level, the trend of the capital market depends on the economic growth situation and the overall sentiment of investors. Short-term stimulus policies may boost the overall sentiment of investors, but when the short-term benefits are over, the data falls back, and the capital market faces downward pressure at the same time. So does China have a synergistic relationship between financial stability and economic growth, that is to say, the economic growth is not ideal, but the capital market still maintains a good upward trend. This depends on a very key inflation factor. Without physical growth and monetary support, the capital market is difficult to break through. One very good piece of information is that our real estate market is completely extinguished, and its monetary diversion effect on the financial market is decreasing, which means that there is such a scene: even under the downward pressure of the macro economy, the capital market is still the only one that can support the currency Object.

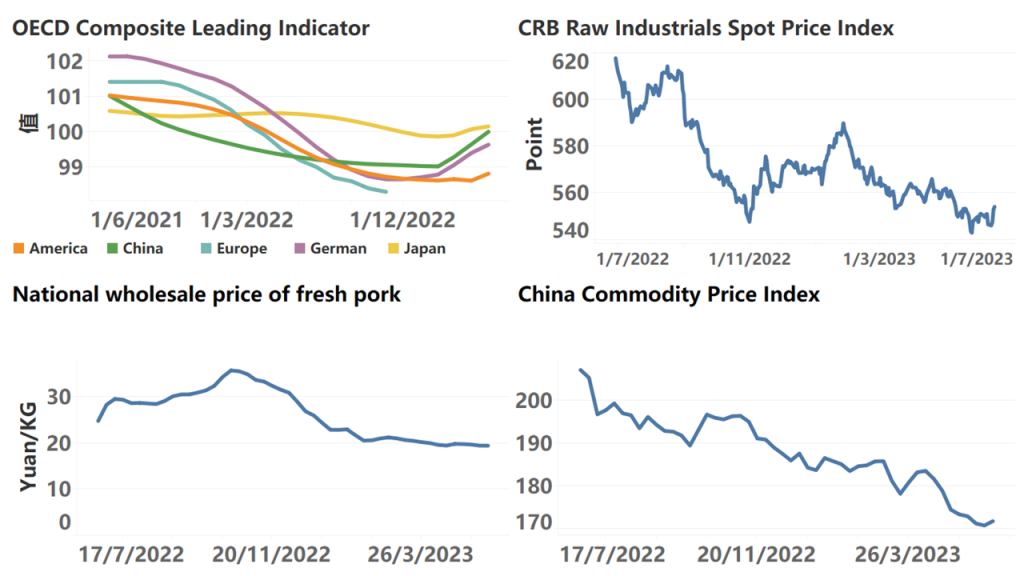

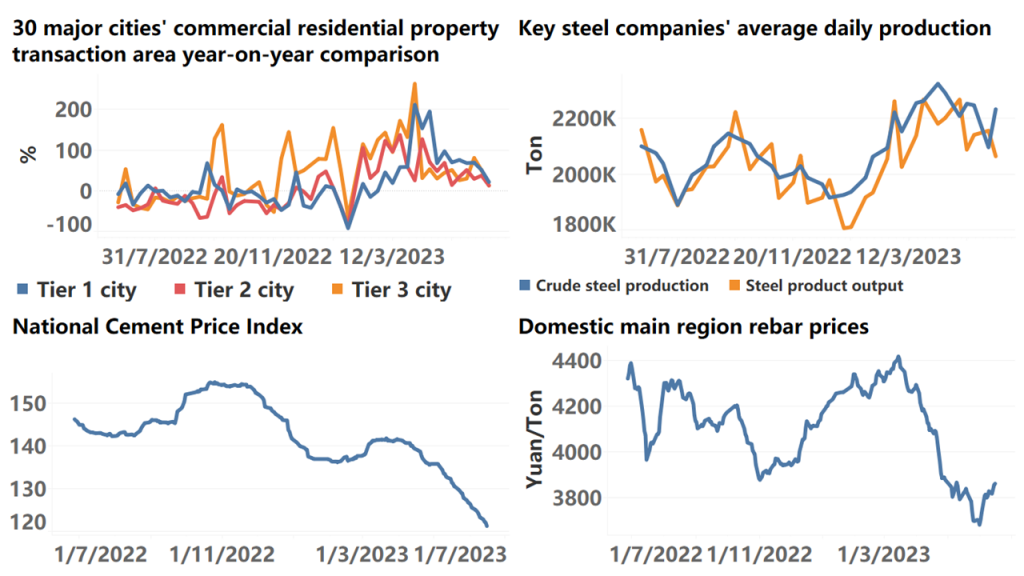

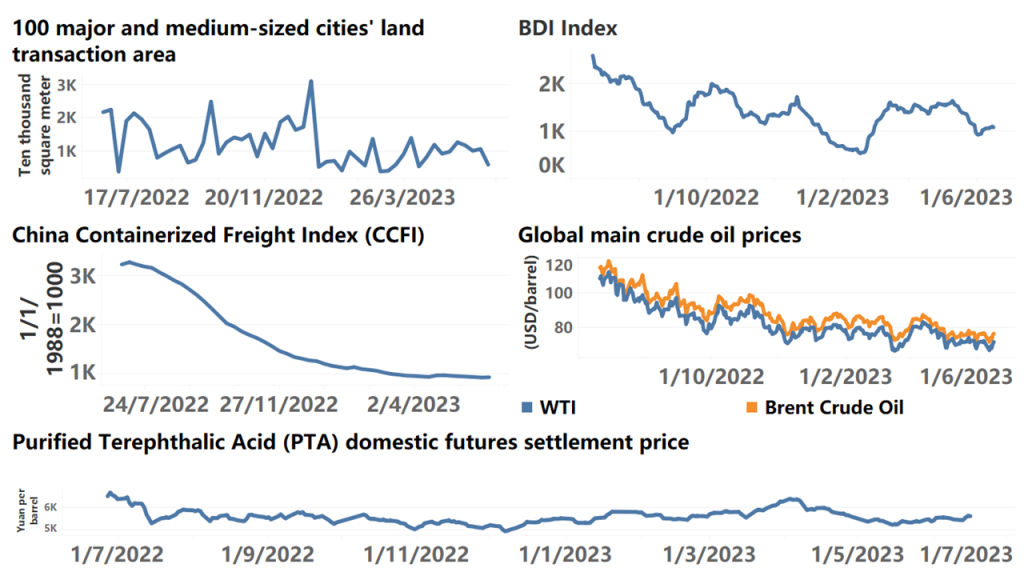

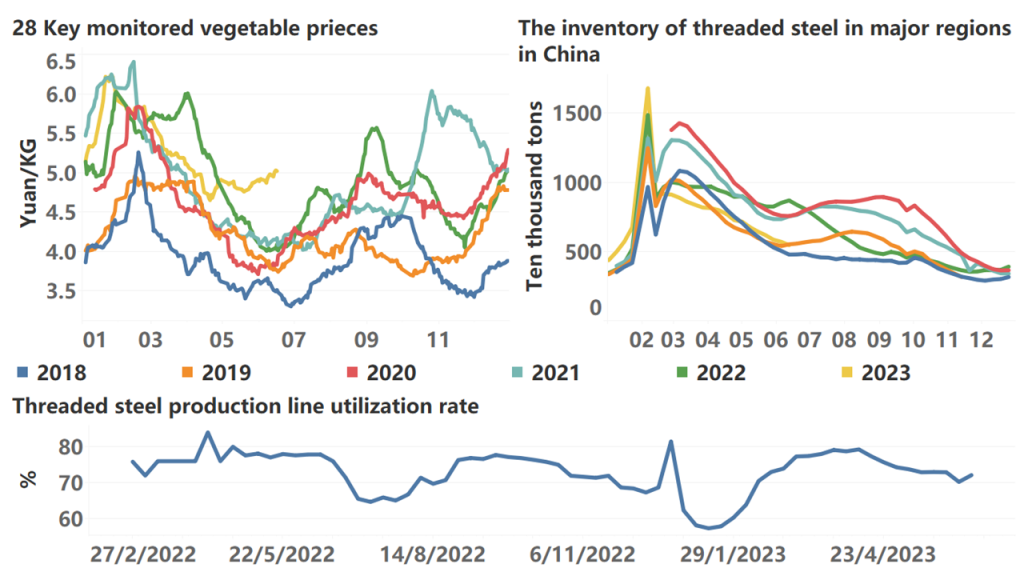

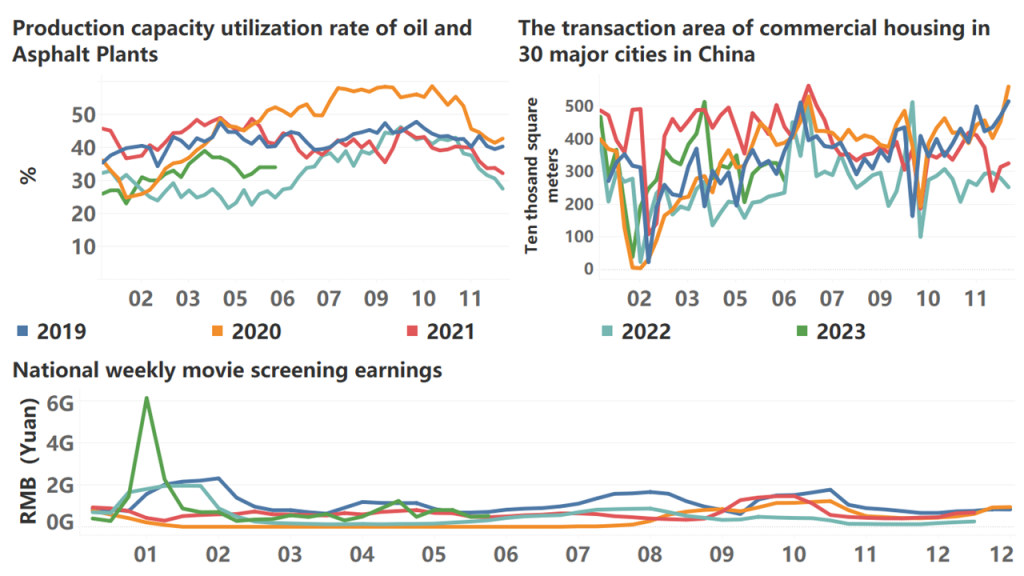

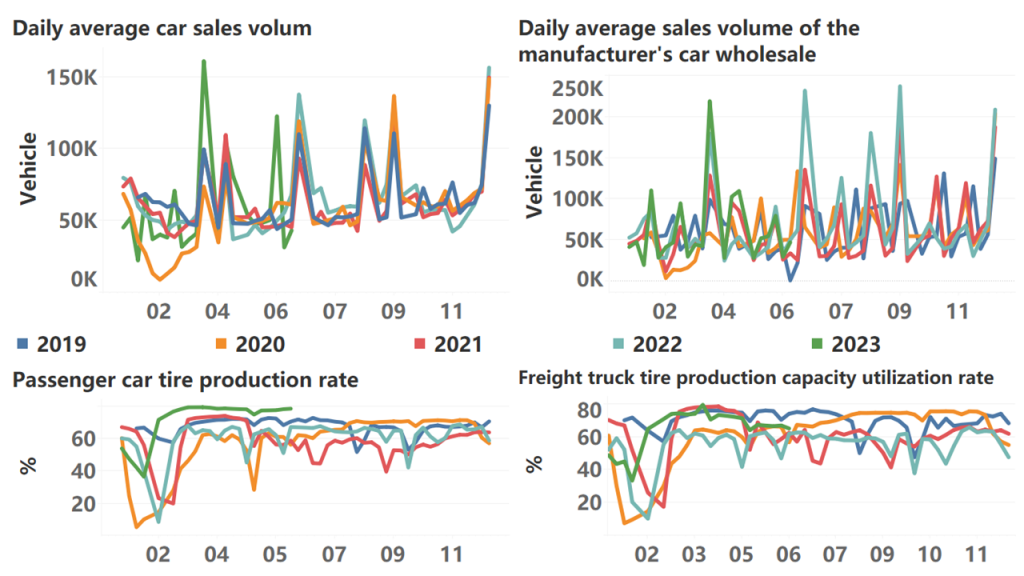

The following are high-frequency data for this week:

*Translated by ChatGPT