Status quo

In April, China’s CPI recorded 0.1%, a drop exceeding expectations, continuing to decline for three months. The PMI also fell below 50 in sync. Against the backdrop of a continued drop in commodity prices, we believe that the severe lack of demand is the biggest challenge currently facing the Chinese economy.

We believe there are issues with short-term debt and a sharp contraction in demand.

In the first quarter of 2023, the national fixed asset investment (excluding rural households) was 10.7282 trillion yuan, a year-on-year increase of 5.1%. Among them, private fixed asset investment was 5.8532 trillion yuan, a year-on-year increase of 0.6%; while the investment growth rate of state-owned sectors reached 10.0%. In the first quarter, private fixed asset investment accounted for 54.2% of the national fixed asset investment, a significant drop from 56.9% in the same period last year. The proportion of private investment in the incremental investment in the first quarter of this year has even dropped to 6.7%.

From the perspective of investment, there are many reasons for the lack of improvement in the growth rate of private investment. We can guess that the balance sheet of private capital is quite bad, that is, the debt part has not been relieved. Despite the overall economic recovery in China from January to April, private capital has not expanded its investment. This indicates that the previous debts have not been cleared, which is highly similar to the “triangular debt” during Zhu Rongji’s era. This has resulted in banks being unable to provide them with financial support, and funds are idling. This should be the main problem in the short term.

Secondly, because private capital cannot expand investment, the reproduction cycle of the national economy has been interrupted, demand cannot expand naturally, which leads to a deterioration in employment and income.

What needs to be specifically supplemented here is that local governments and state-owned enterprises, represented by urban investment, can still obtain investment from the financial sector even if the balance sheet is bad, and stimulate economic growth in the short term, but this stimulus is not sustainable.

We believe there are long-term issues with real estate – population, expectations

In April, the number of second-hand residential transactions in Shanghai was 17,334, a month-on-month decrease of 26.71%; the number of online signed second-hand residential properties in Beijing was 13,997, a month-on-month decrease of 37.3%; the number of second-hand residential transactions in Hangzhou was 5,883, a month-on-month decrease of 32.7%; the number of second-hand residential transactions in Nanjing was 11,318, a month-on-month decrease of 13%; the number of second-hand residential transactions in Hefei was 2,127, a month-on-month sharp drop of 40%.

The sharp decline in commodity housing transactions is somewhat related to the continuous decline in population. The birth rate at the end of 2022 was 6.77 per thousand, a new historical low. In an environment where the population is sharply shrinking, the significant increase in real estate in the past may lead to a market pattern where supply exceeds demand.

From the perspective of young people, long-term expectations should be whether they can have a decent life through a job, even if they lose this job, they can find new work in the labor market in a short period of time. The formation of long-term expectations is based on short-term expectations. Currently, the youth unemployment rate is around 19%, and young people are pessimistic about employment, which weakens expectations and simultaneously reduces consumer spending.

How to Achieve Economic Growth – Strategic Inflation

At the end of the 20th century, resolving the macroeconomic situation through the method of bad debt stripping might be a feasible method currently. This method has two hidden dangers. One is whether it will lead to flooding. The other is whether it will form a large moral hazard and bury hidden dangers for future economic development. We need to distinguish the reform plan at the end of the 20th century from the reform plan of 2008-2010. The end of the 20th century faced an established debt problem. It was necessary to inject liquidity into the economy to solve the crisis. The 2008-2010 reform plan did not face debt, but faced a sharp contraction in external demand. It was necessary to implement countercyclical adjustments at this time. Both of these plans appear as a substantial release of money, but the first one hedges debt and injects liquidity directly into sectors with production capacity. The second one directly participated in the market. From the perspective of later results, the first one did not produce much inflation, and the second one produced some inflation. The current situation is similar to the end of the 20th century. We can strip off bad debts directly, inject liquidity into private capital with production capacity, and help it repair the balance sheet. Even if inflation occurs, it will be a mild inflation, which is not harmful to overall economic development.

If this method is adopted, then the main body of moral hazard will be local governments and state-owned enterprises. Disclosing information and handling bad debts publicly can punish defaulting units. From the perspective of trade-off, this will exchange for long-term economic growth.

Bad debt stripping, as a financial monetary tool, is not subject to the lower limit of zero interest rate and reserve ratio, and it does not conflict with the normal monetary policy space mentioned by our central bank. Will it produce a trap of local governments that are too big to fail? We have various tools to control this risk. It is also different from QE and MMT theory in the general sense, the key is to whom the liquidity is injected.”

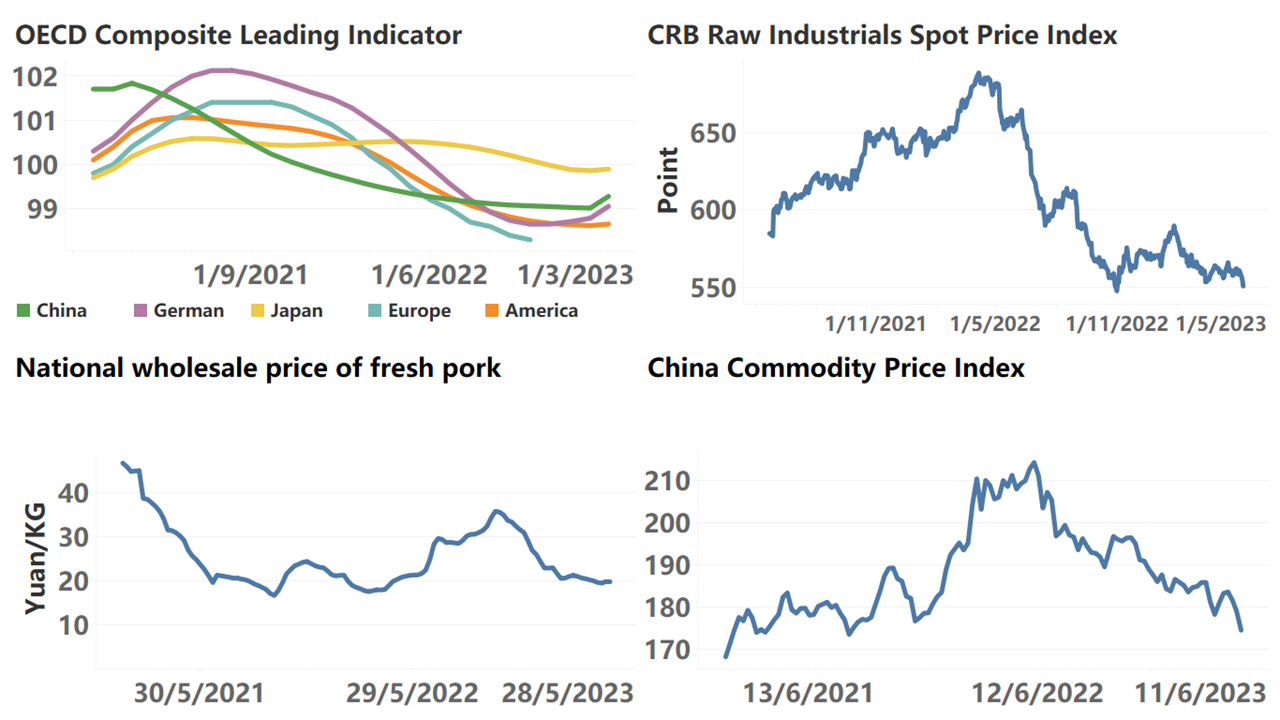

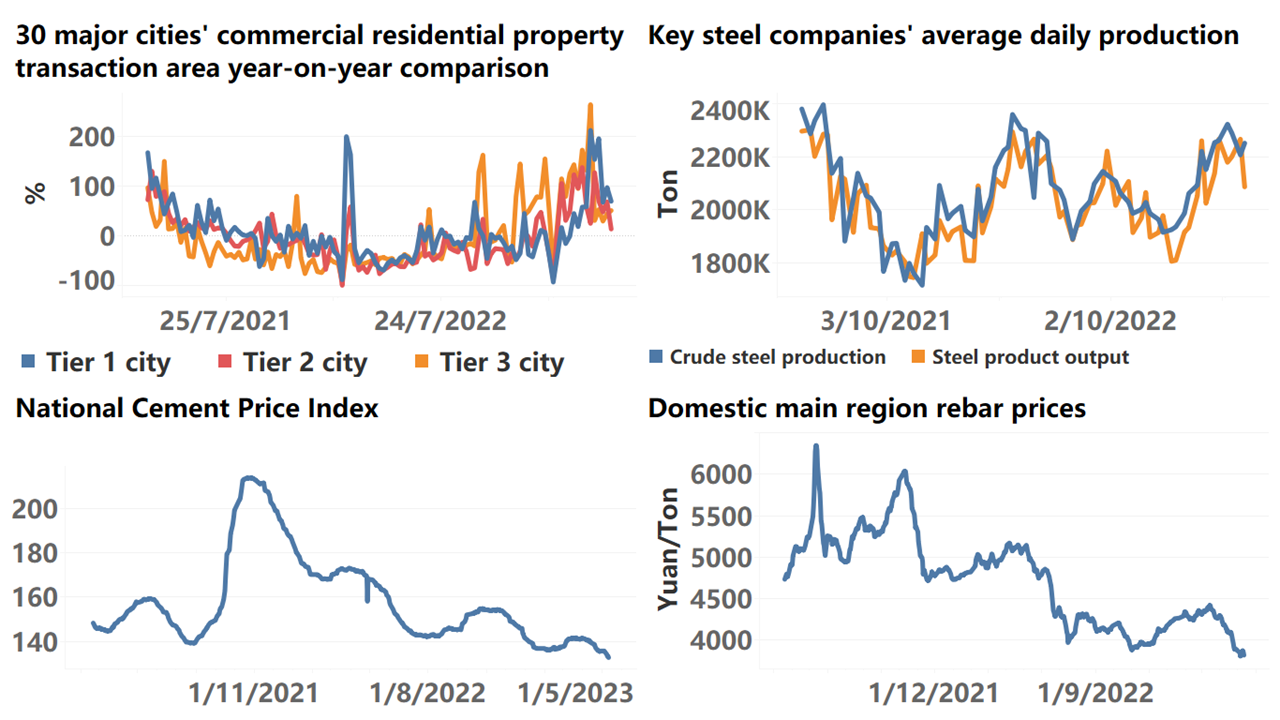

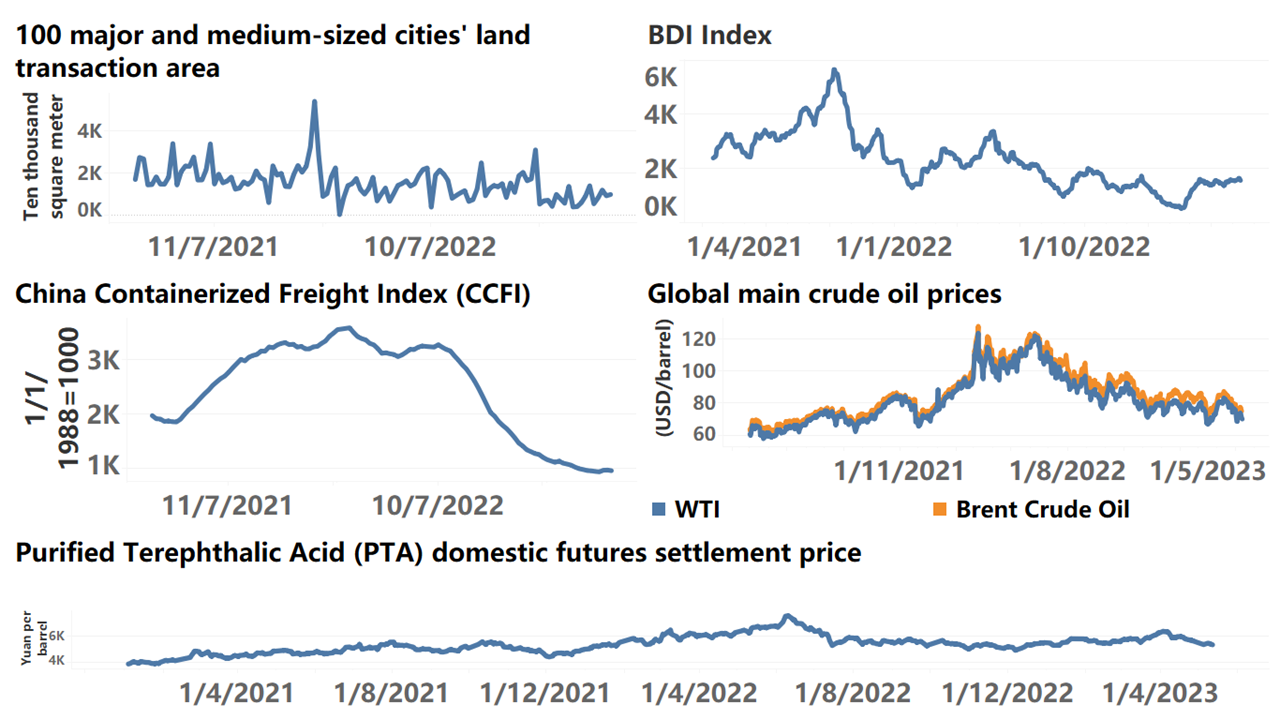

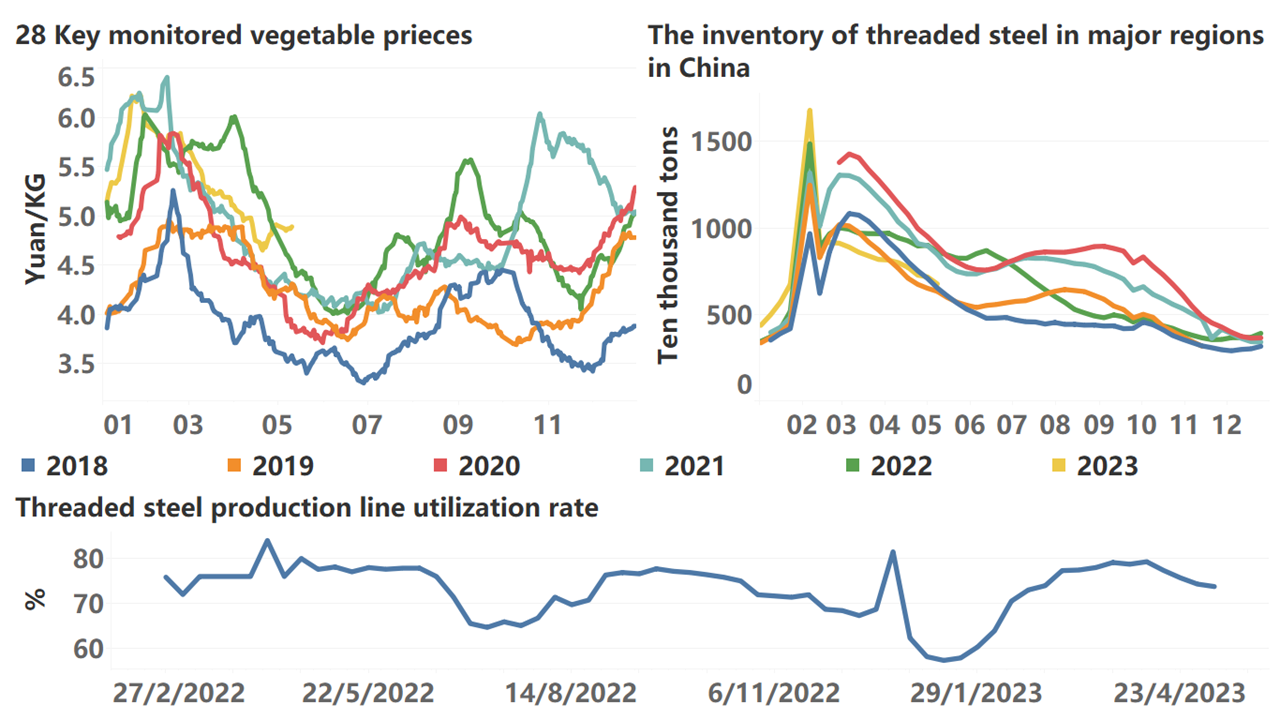

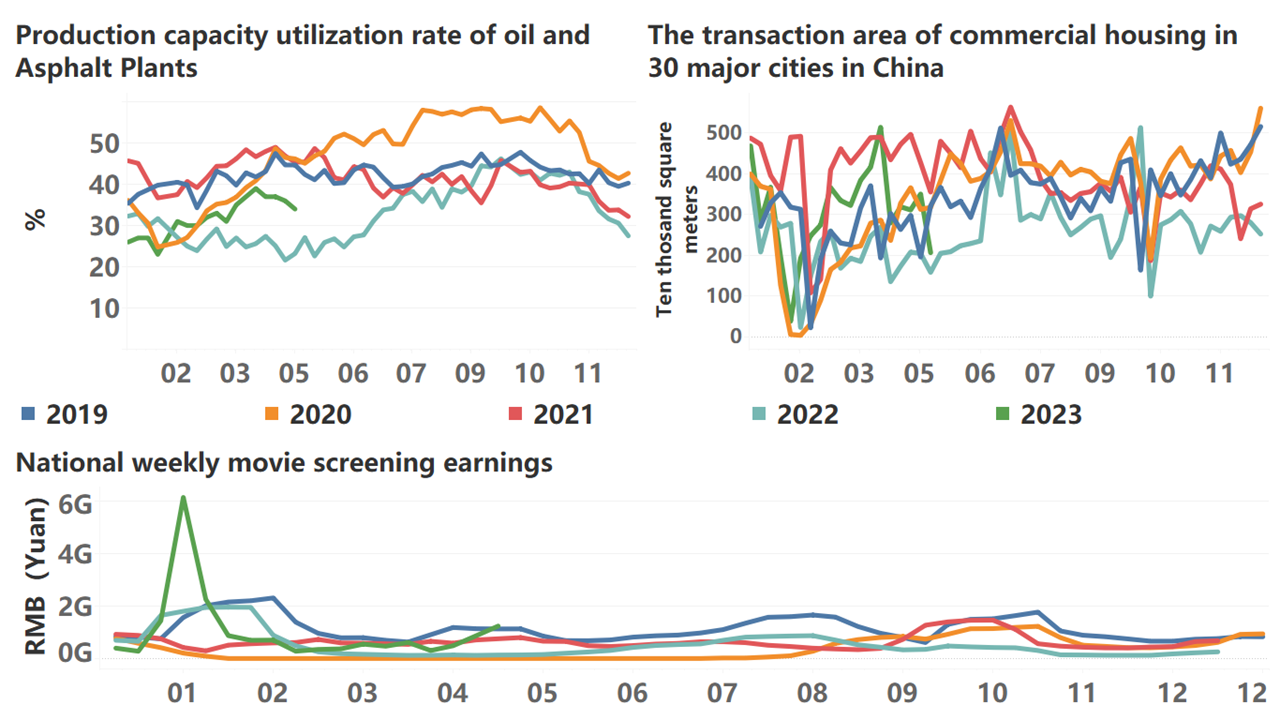

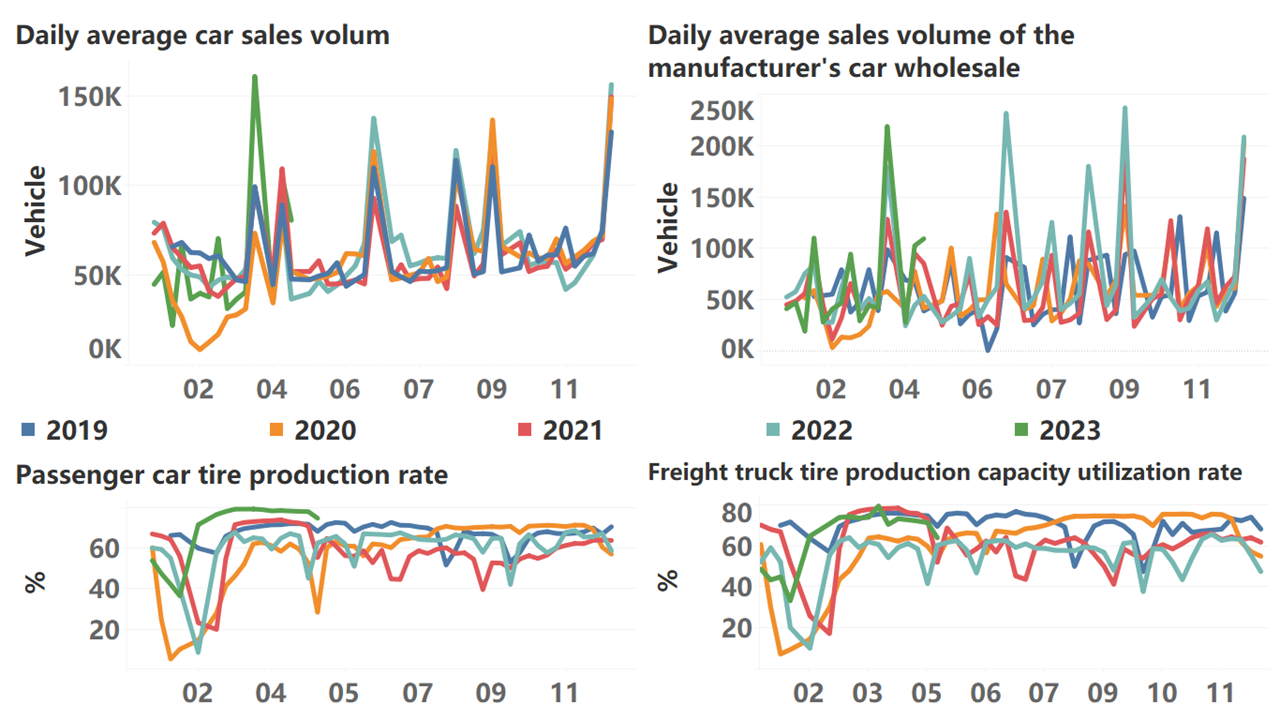

Below are the high-frequency data for this week:

*Translated by ChatGPT