Since April, the U.S. dollar index has gradually fallen, from 102.6 to 101, with some fluctuations but a relatively small overall range, reaching a low of 100.788. As of May 5th, it closed at 101.214, overall remaining weak. The main scenario for a long dollar position is the Federal Reserve disregarding financial stability and aggressively raising interest rates, or maintaining current interest rate levels for an extended period. Short factors include the Federal Reserve possibly entering a rate-cutting cycle in the face of an upcoming economic recession in the fourth quarter. From the current situation, it is necessary to monitor the trend of CPI and regional bank crises. We can compare that after the collapse of the First Republic Bank, there will definitely be new bank failures. We need to continuously observe the impact of bankruptcies on the tightening of financial markets. Secondly, the U.S. core CPI service items are still resilient, and the risk of stagflation remains relatively high. Therefore, the risk of going long is relatively large.

Under the macroeconomic backdrop of the U.S. economy heading towards stagflation risk and the weakening of the dollar index, market participants believe that the Chinese economy is in an upward phase, especially as economic growth will appear high in the second quarter due to a lower base. However, the USD/CNY offshore market has been continuously rising. Since April, the USD/CNY offshore market has gradually increased, from 6.877 to 6.922. This is quite inconsistent with the RMB appreciation cycle from the second half of 2020 to early March 2022, which to some extent reflects that the Chinese economy is not as prosperous as it appears. The Central Politburo meeting on April 28th also pointed out that the current improvement of China’s economic operation is mainly recovery-based, with weak endogenous power, insufficient demand, and new resistance to economic transformation and upgrading. High-quality development still faces many difficulties and challenges.

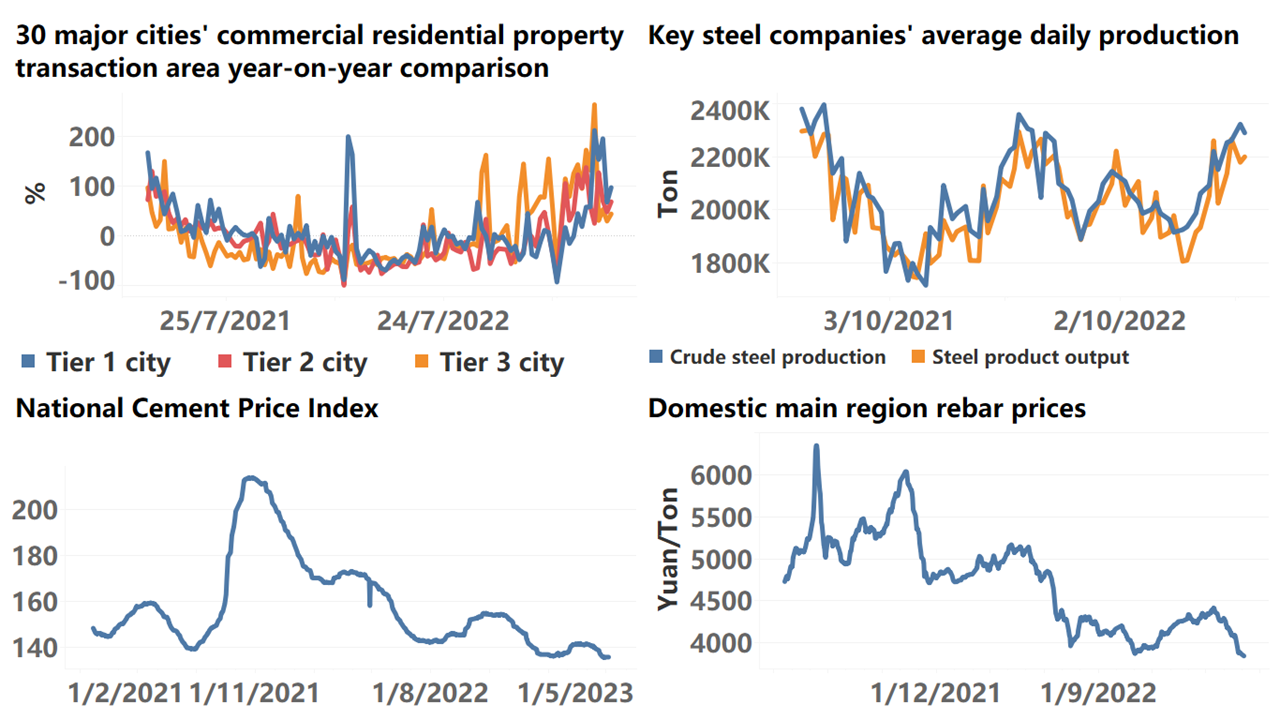

In terms of specific data, the April manufacturing PMI was far below expectations, falling to 49.2. The main rebar contract has slid from 4160 to 3608 since April, experiencing a significant decline. The main coking coal contract has fallen from 1860 to 1325 since April, with a massive decline. The main live pig contract has slightly rebounded since April, rising from 15291 to 15964, but overall prices remain low. From the price data and PMI data, the demand side is very weak, and the inflation issue previously discussed in the market seems to be taking shape. In our previous report discussing the risk of deflation in China, we pointed out that the main source of deflation is local government debt burdens. At present, this debt problem is spreading throughout the economy. Whether we are at the deflationary tipping point and, going forward, the economy falls into a spiral of deflation depends on the following key data:

- New special debt financing for the government;

- Growth rate of fiscal revenue;

- Manufacturing PMI;

- Real estate financing.

For investors, a deflationary outlook is not a favorable economic state. From an external environment perspective, the Federal Reserve maintaining interest rates at restrictive levels and the gradual decline of U.S. CPI are processes of the U.S. economy cooling down. If the risk of domestic deflation in China increases, it will severely suppress the prices of risk assets. Therefore, the profit-taking point should not be set too high and should be adjusted dynamically according to the macroeconomic situation. The judgment of the A-share market should focus on the development of the USD/CNY exchange rate. We can consider the following scenarios:

- If the Federal Reserve stops raising interest rates in June, the U.S. dollar index may remain at current levels. If the People’s Bank of China (PBOC) adopts a loose approach, the USD/CNY will continue to appreciate, which would be a very pessimistic signal for the Chinese stock market.

- If the Federal Reserve continues to raise interest rates in June, the U.S. dollar index may experience a temporary strengthening, while the PBOC adopts a loose approach. The USD/CNY appreciating would also be unfavorable for the Chinese stock market but not to the extent of being extremely pessimistic.

All of this depends on how domestic demand can escape this deflation-like risk, how monetary policy is transmitted, and whether there is a possibility of allowing the government’s non-performing assets to undergo debt collateralization and refinancing.

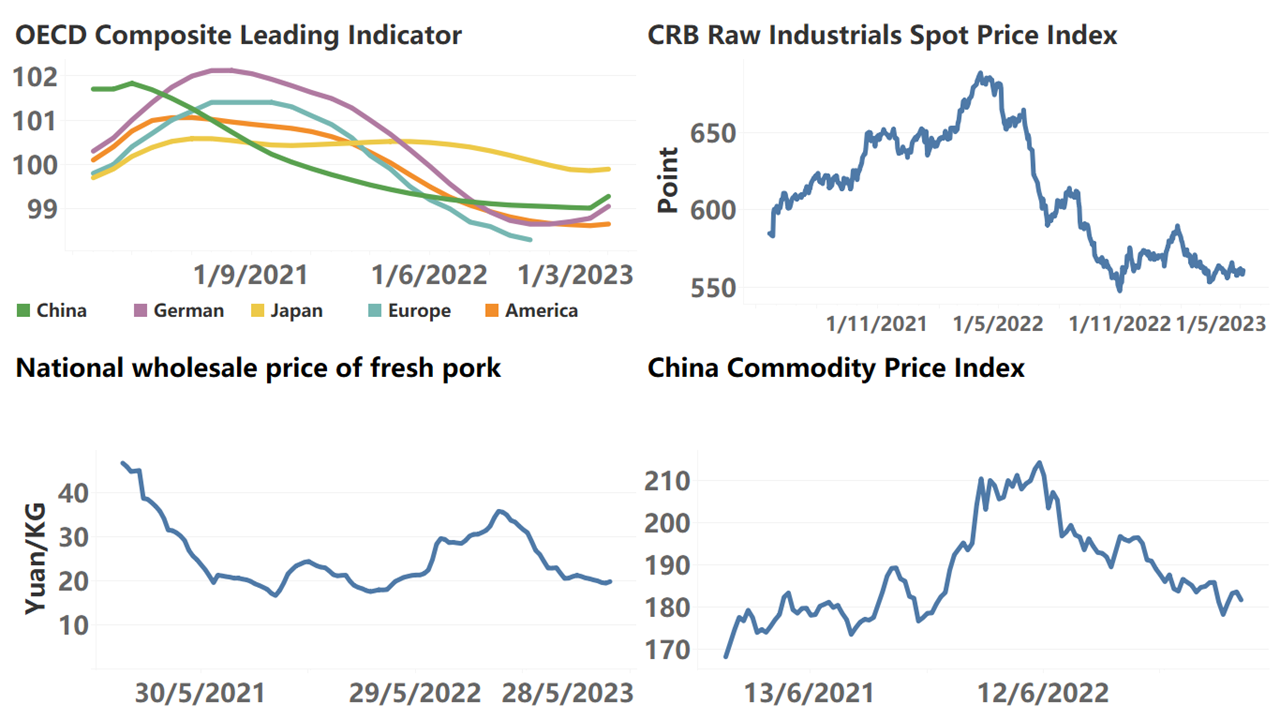

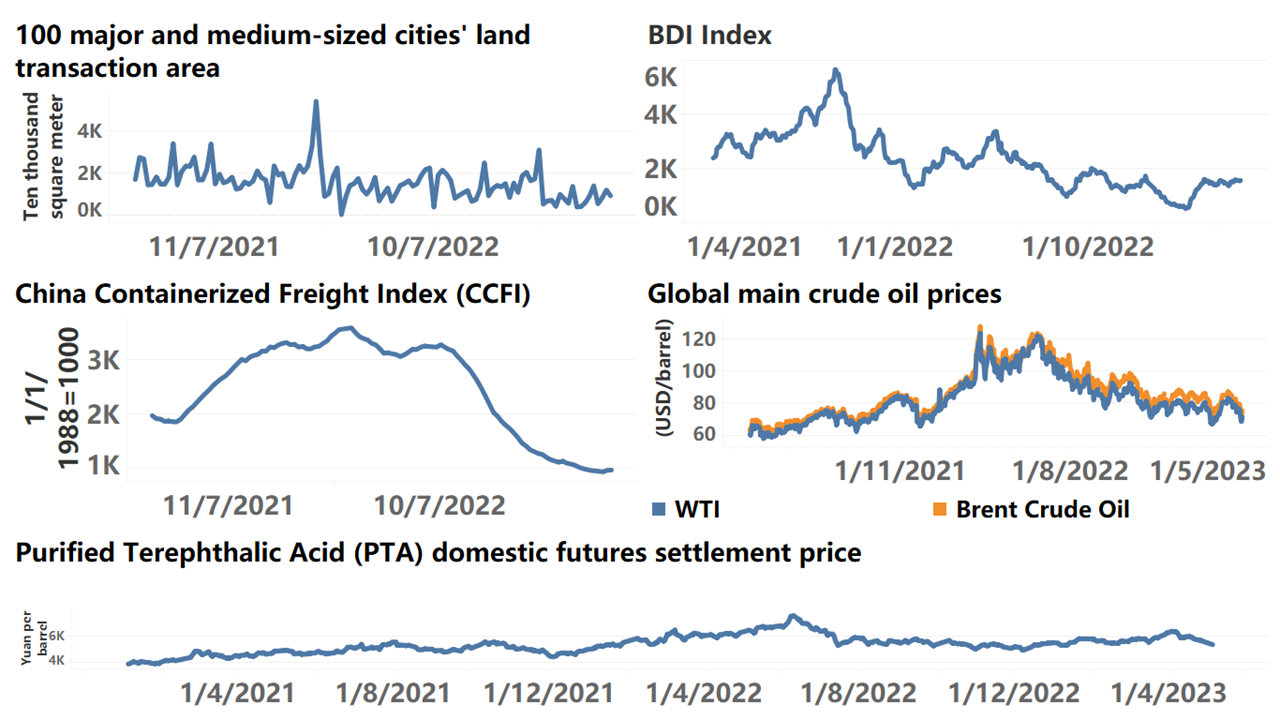

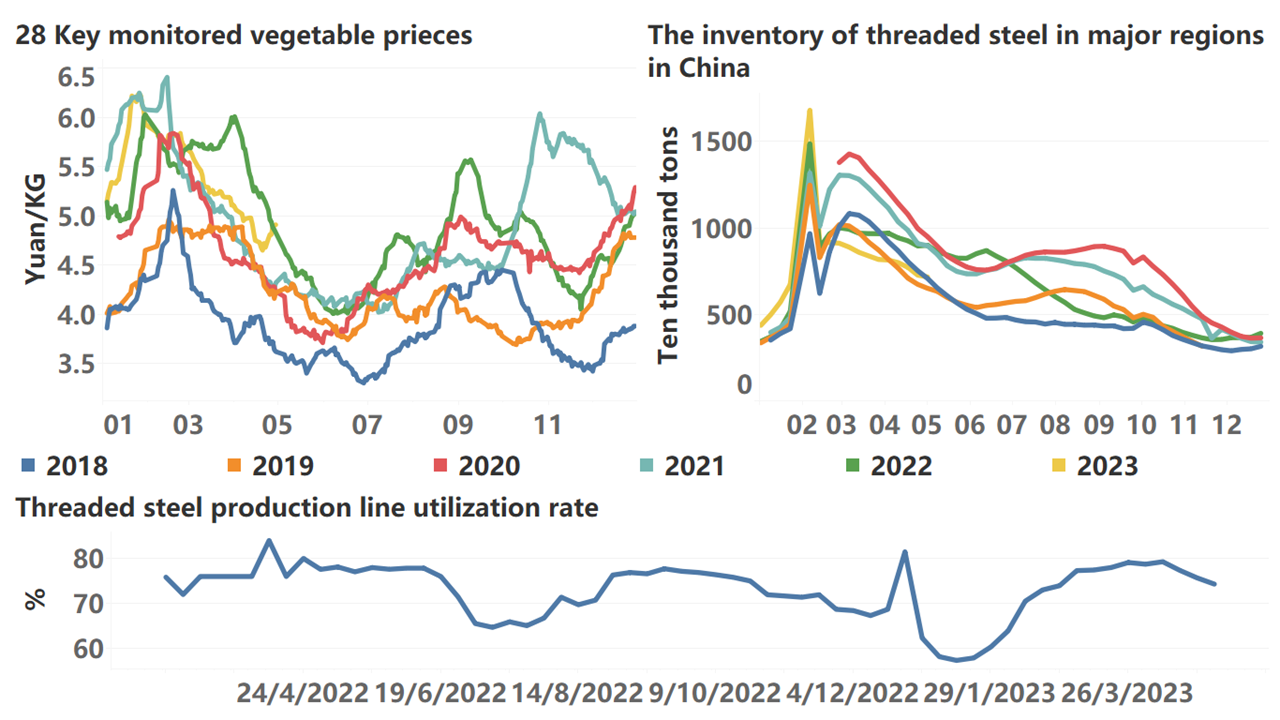

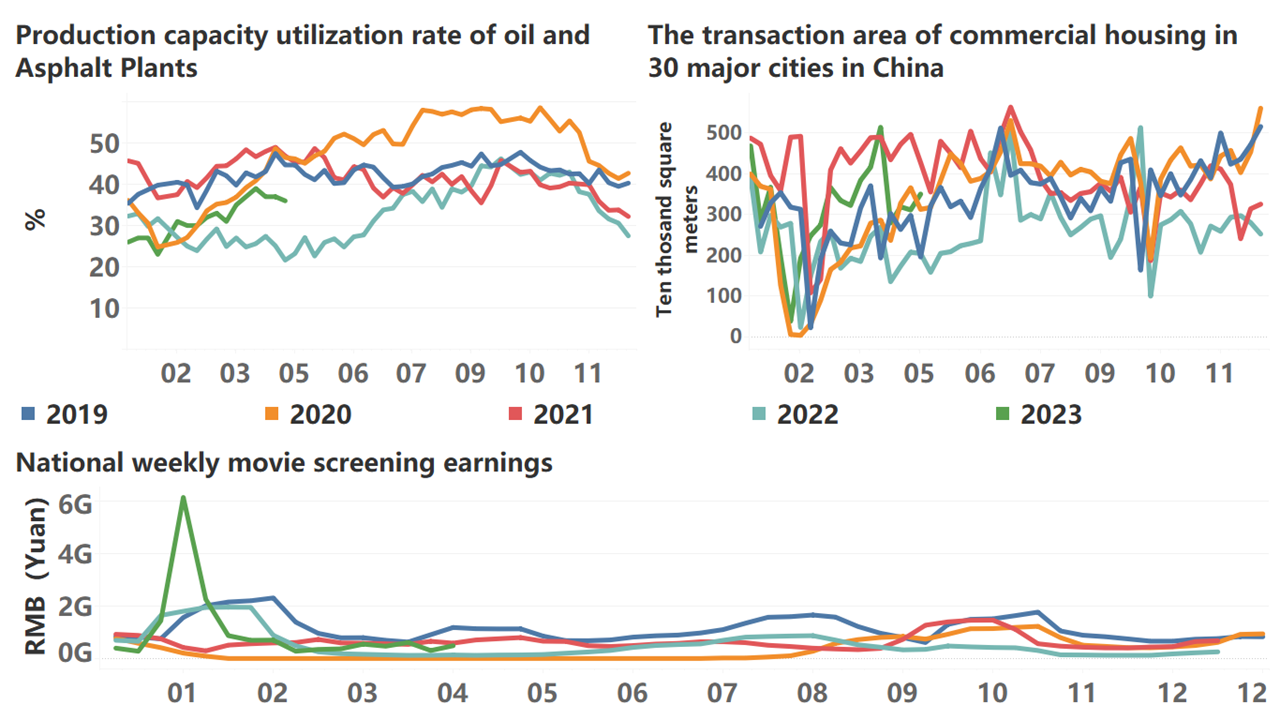

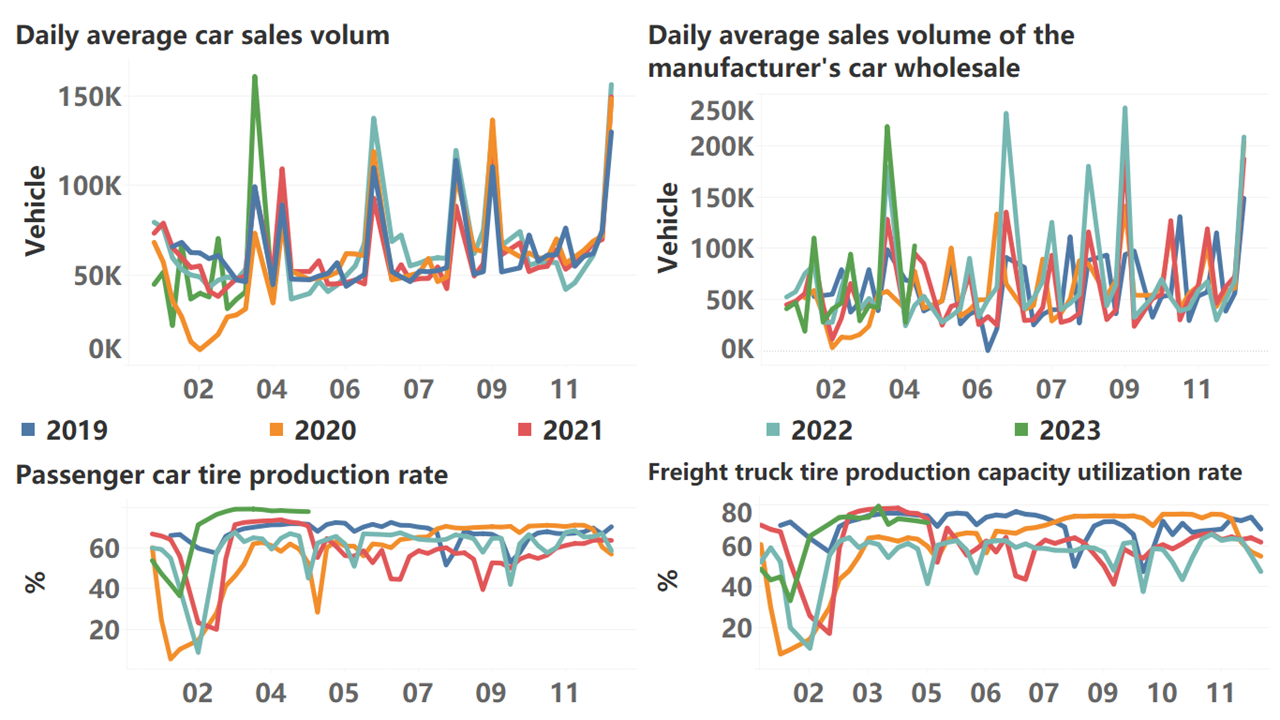

Below are the high-frequency data for this week:

*Translated by ChatGPT