This week, the Chinese capital market experienced a significant surge on Monday, followed by a slight increase on Tuesday, and continued to decline, with a considerable drop on Friday. The Shanghai market fell by 1.95%, with the index closing at 3301.26 points, returning to its position two weeks ago. As of April 21, the overall return of A-shares was quite low, returning to the level of April 3. Last weekend, we released “Comprehensively Bullish,” and A-shares welcomed the biggest increase this month on Monday. From the macro data perspective, the macro data released on Tuesday showed that retail sales in March exceeded expectations with a very impressive growth rate, and consumption is still in the expansion range. Future retail sales growth will continue to rise. The sharp fluctuations in A-shares this week were mostly emotional, with rapid increases on Monday and Tuesday accumulating a lot of profitable funds. In the context of tense emotions, massive profitable funds exited the market.

This week, Hong Kong stocks fluctuated and fell. As of April 21, the monthly return rate for Hong Kong stocks was negative. In Europe, Germany and France adjusted horizontally this week, and as of April 21, the monthly return rate was relatively high. The Dow Jones fluctuated and fell this week, with a return rate higher than the previous high as of April 21. The Nasdaq also fluctuated and fell this week. As of the 21st, the April return rate was relatively low, without significantly surpassing the previous high. Considering the performance of A-shares, Hang Seng, European, and US stock markets, the global stock return rate in April was relatively low as of the 21st, which is closely related to the heightened market emotions amid the global recession outlook. The prospect of a 25 basis point rate hike at the early May Federal Reserve meeting significantly impacted global capital markets. It is worth noting that the direction of the economy under restrictive interest rate policies will determine the overall return rate of global stock markets. However, shorting stocks is not a wise choice, as no central bank can withstand the pressure of a large-scale stock downturn in the face of financial stability.

The price of gold (New York) fluctuated and fell this week, wiping out all gains in April as of the 21st. Brent crude oil fell sharply this week to 81.7, wiping out all gains this month. The US dollar index fluctuated, and as of April 21, it remained stable overall in April, strengthening against other assets due to the Fed’s rate hike expectations. In last week’s research report “Comprehensively Bullish,” our view that gold prices would not rise proved to be correct.

Chinese Macro:

On Tuesday, the data released by the National Bureau of Statistics showed that the GDP growth rate for the first quarter was 4.5% YoY; retail sales growth rate in March was 10.6%, the cumulative YoY growth rate of commercial housing sales area was -1.8%, and the automobile sales growth rate was 11.5% YoY. In terms of foreign trade, imports decreased by 1.4% YoY, while exports exceeded expectations, recording a 14.8% growth rate. The industrial added value growth rate for the month was 3.9% YoY. The fixed-asset investment completed amount growth rate was 5.1% YoY, with real estate growth at -5.8%.

In mid-March, our GDP data forecast ranged between 4.3-4.5%, and the final economic data reached the most optimistic scenario. Retail sales and exports exceeded expectations and were

the main factors. Retail sales growth will continue to strengthen, mainly driven by gold and silver jewelry, catering, clothing, sports and entertainment, and automobiles.

In terms of exports, automobiles and photovoltaics were the main drivers. From a climate change perspective, the growth rate of new energy vehicle sales is still too slow. If China, the United States, and Europe can reach a consensus in the next round of climate negotiations, then the export data for new energy vehicles and photovoltaics will continue to rise.

Real estate sales prices and volumes are both improving, but real estate investment growth remains weak. Overall, the industry is still in the destocking phase. One issue to consider is whether companies engaged in commercial housing development will continue to expand their balance sheets. Even if the industry is in the later stages of destocking, balance sheet expansion for commercial housing development companies remains extremely difficult. Although various data show that the amount of medium and long-term loans for residents has increased and the financing volume of real estate development companies is rising, the debt ratio of real estate companies is very high. For these companies, the current goal is to reduce the debt ratio. Current financing is used to repay debt, not to increase leverage and expand the balance sheet. So where is the turning point? The turning point requires an upward macro environment, especially for the real estate industry, and a clear basic framework for the new order in the real estate industry. Furthermore, real estate tax is the biggest policy uncertainty. Only when this uncertainty gradually settles will investors pursue returns. From these three perspectives, the turning point has not yet appeared.

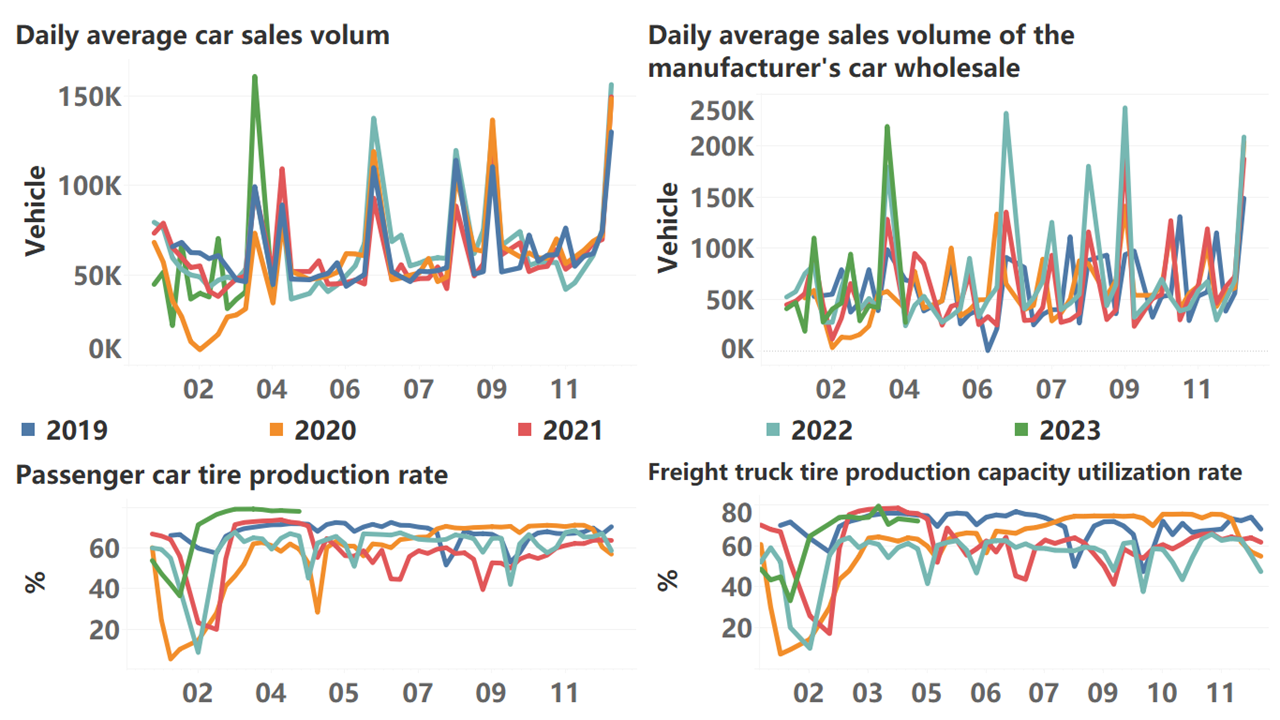

It is worth noting that although automobile exports have increased significantly, the domestic market’s absolute value of automobile sales is not as optimistic as expected. The sharp price cuts since the beginning of March have not had a significant stimulative effect on actual sales. In December 2022, we predicted the path of consumer recovery this year, stating that consumption would continue from service consumption to general merchandise consumption to durable goods consumption (automobiles, commercial housing). Based on the current data, enthusiasm for service consumption remains high, general merchandise consumption is gradually picking up, and in the context of a continuously improving economy, we believe that consumption will transition to general merchandise and durable goods in the next phase.

As investors, we should bear in mind that the development of the real economy is essential, but currency is even more critical. This is why the macro economy is strong, but the overall return rate in April has not been high so far.

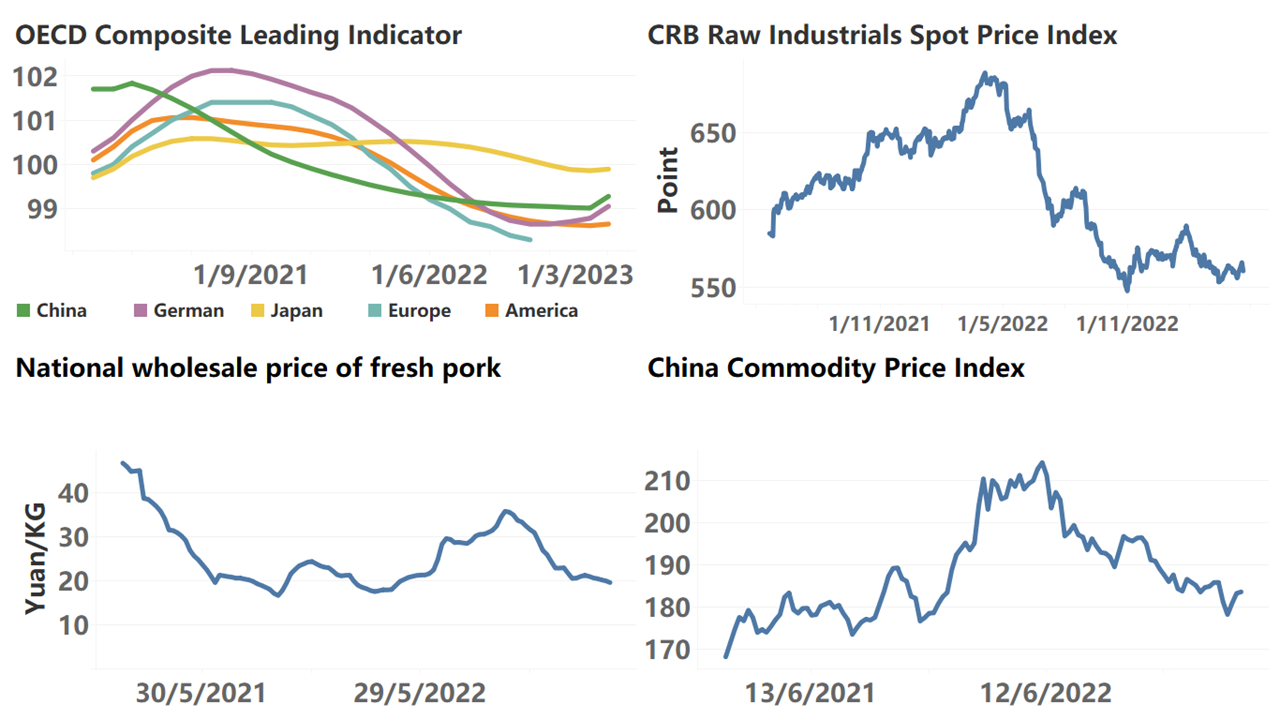

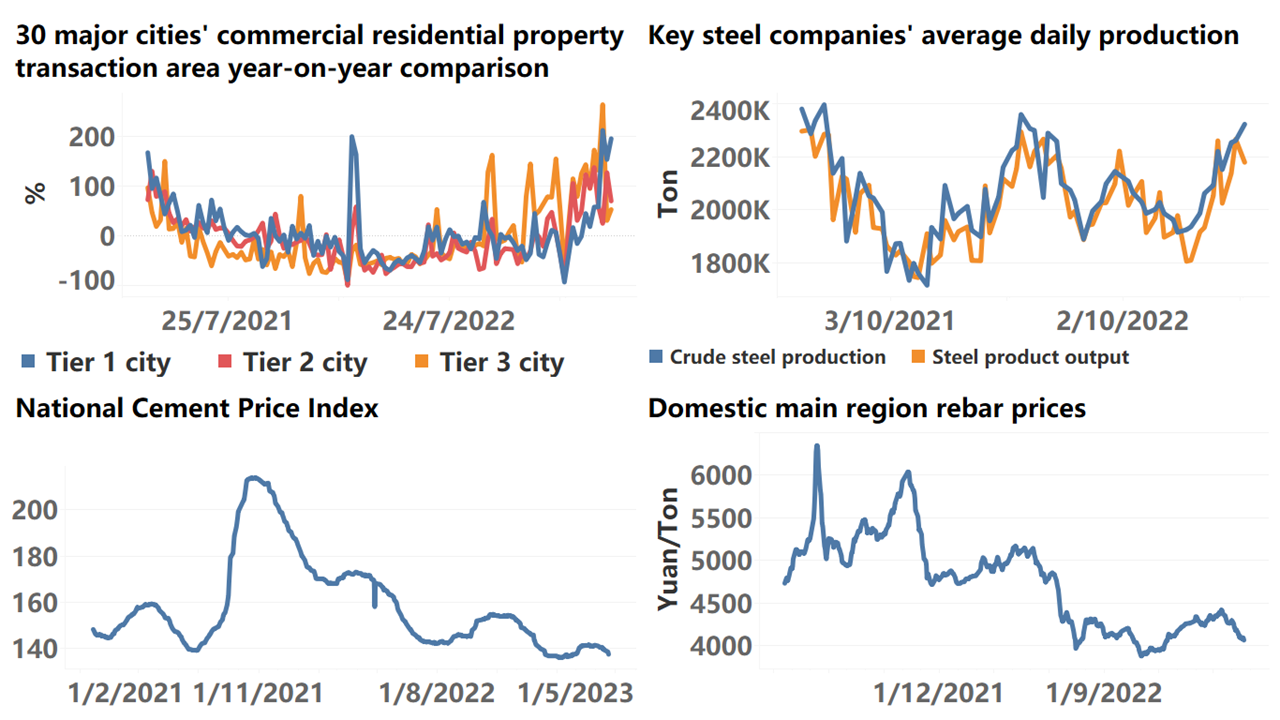

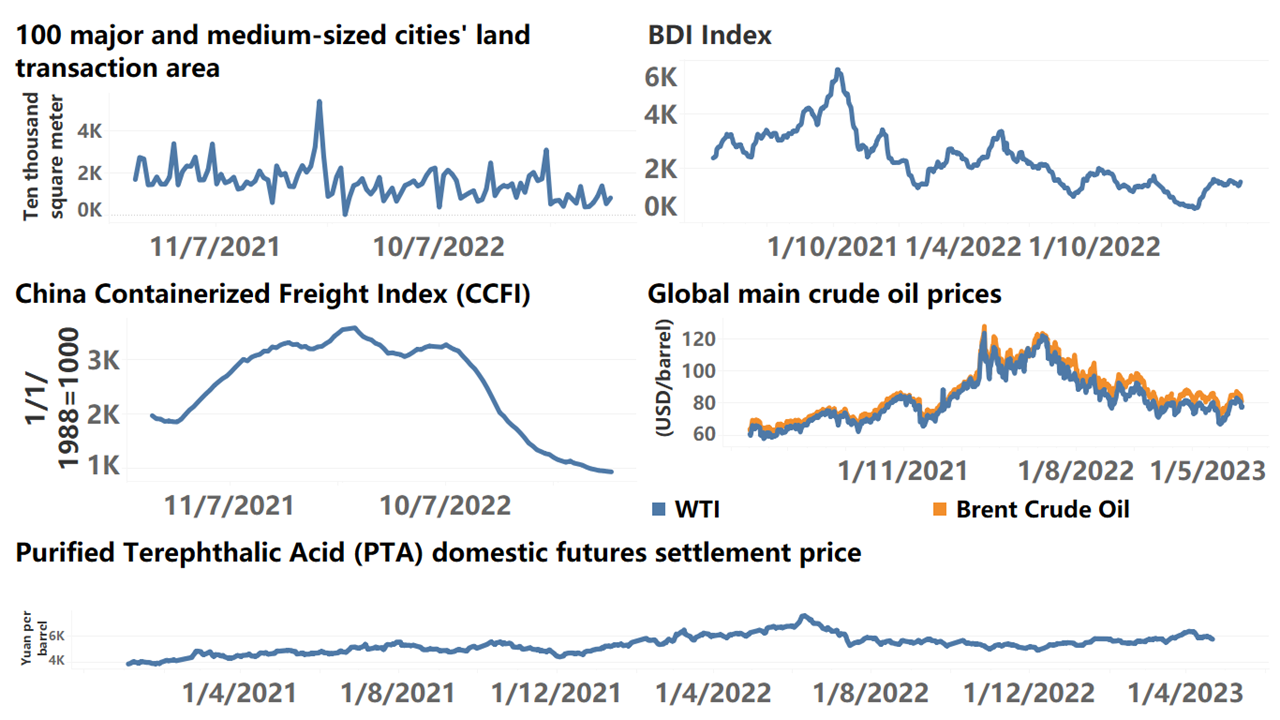

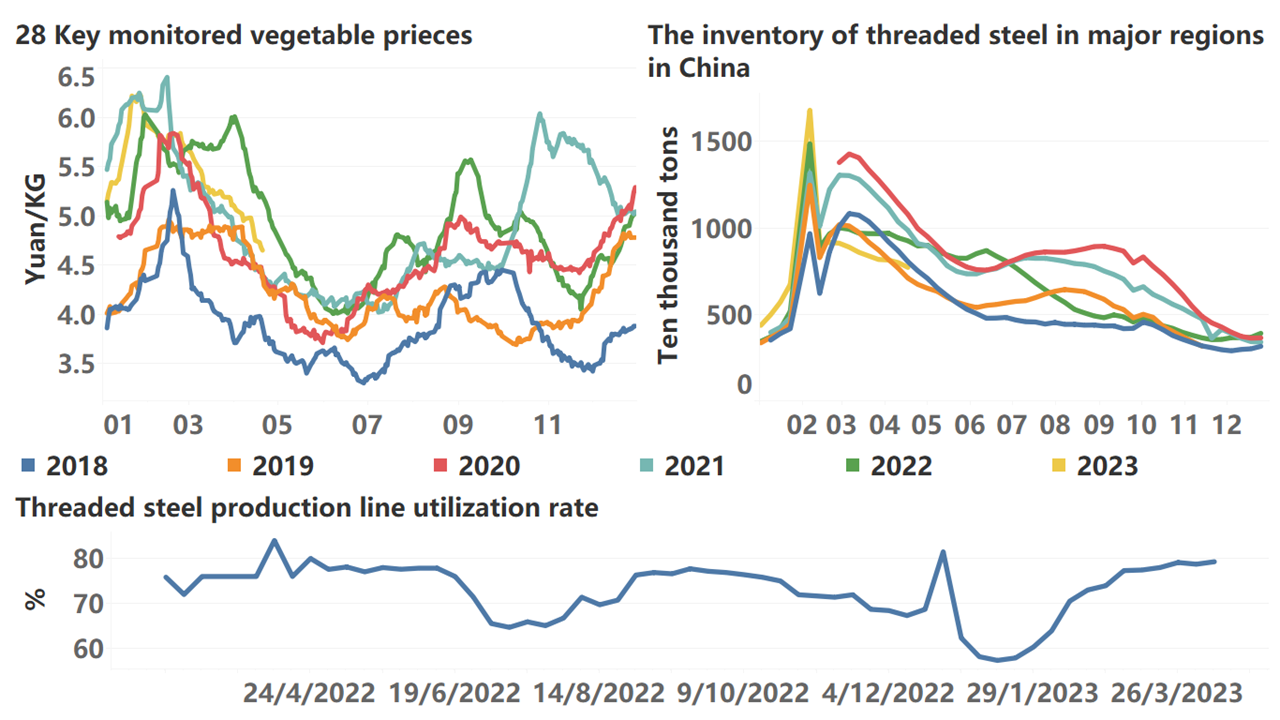

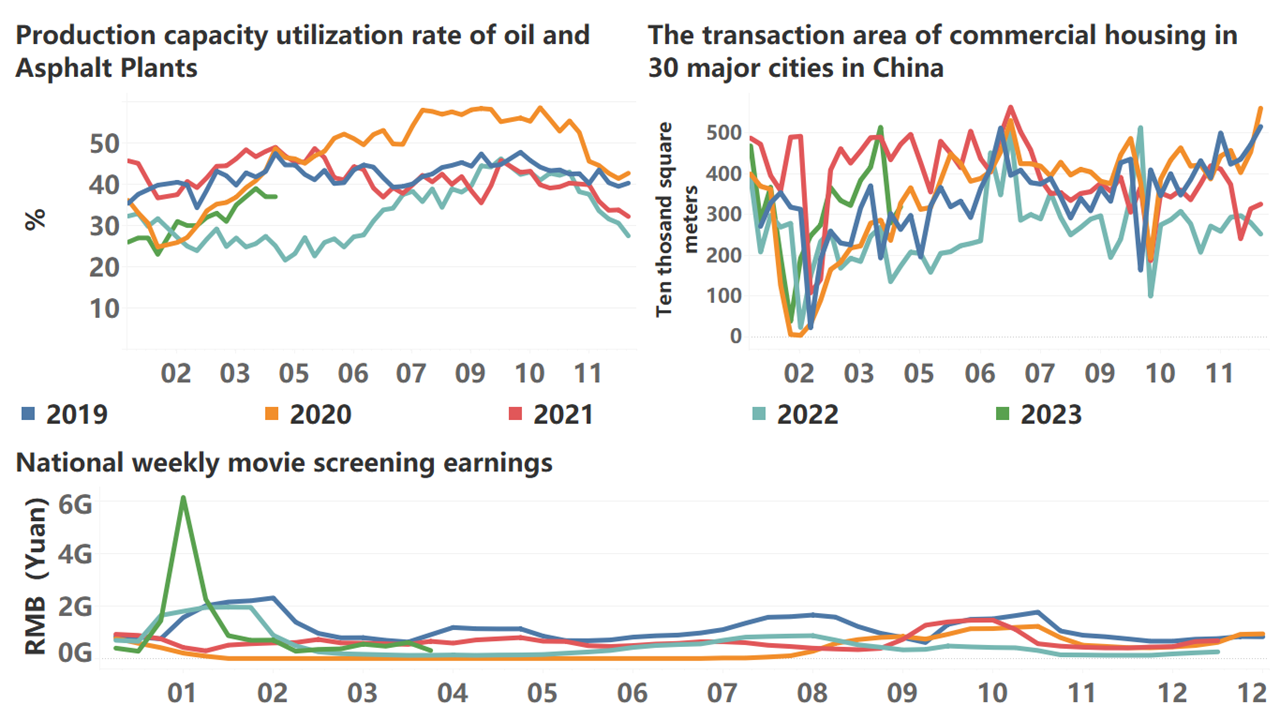

Below are the high-frequency data for this week:

*Translated by ChatGPT