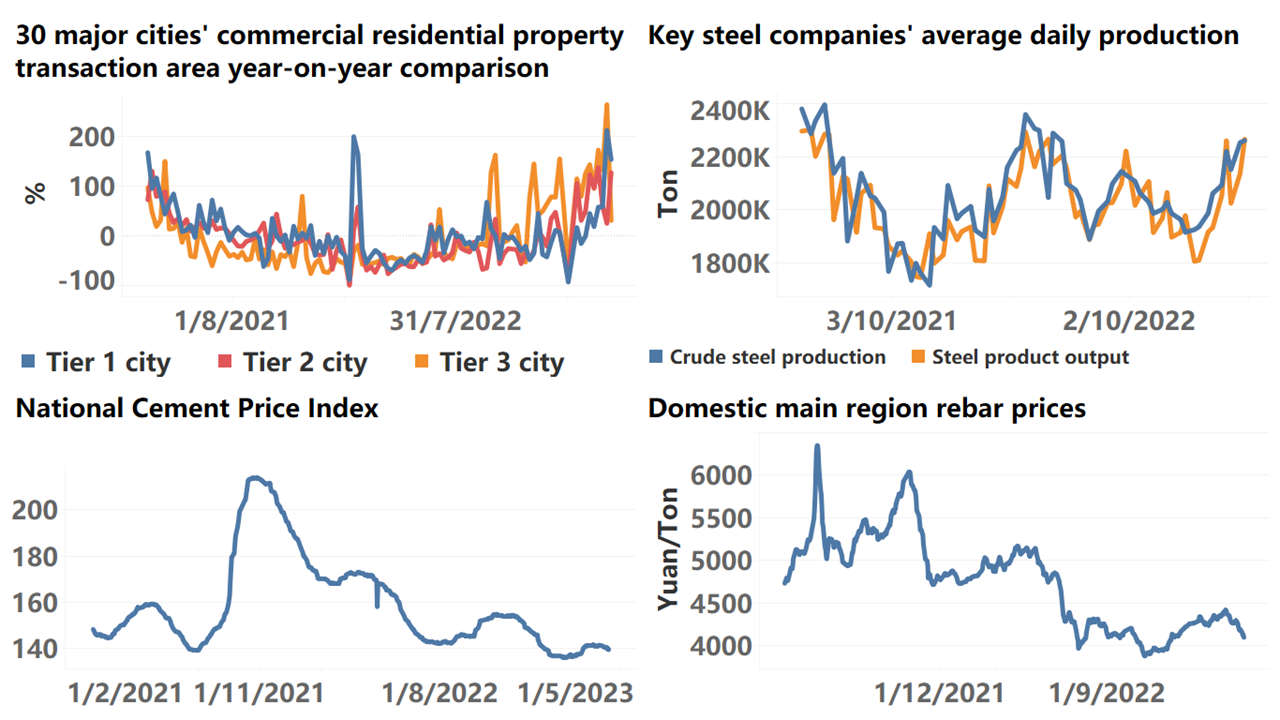

This week, the Chinese capital market was volatile with larger intraday fluctuations. Among them, the Shanghai Composite Index closed at a new high since March 8 on Friday, still a certain distance away from 3400 in early July 2022. In Asia-Pacific, the Hong Kong Hang Seng was volatile with larger intraday fluctuations, basically fluctuating within the range of the previous high point (March 7). The Nikkei 225 surged this week, surpassing its previous high. In Europe, London posted five consecutive gains. Paris also saw five consecutive gains, far exceeding its previous high. Frankfurt in Germany continued to rise, surpassing its previous high. In the United States, the Dow Jones rose during the week, far exceeding its previous high. The Nasdaq underwent a sideways adjustment, with technology and traditional industries showing differentiation. In terms of currency, the US dollar index continued to decline, approaching 100.8, falling below its previous low. The USD/CNY exchange rate gradually declined, with more room to fall compared to the previous low. In terms of commodities, New York gold fell sharply on Friday, with the weekly gain basically erased, remaining in a sideways adjustment position. Brent crude oil gradually rose. Domestically, rebar prices gradually declined, with coking coal also declining, showing a continuous downward trend, currently reaching the price level of April 2021.

The asset prices in the financial markets are generally consistent with the judgment in last week’s report “Recession Outlook and Capital Markets.” Affected by the short-term liquidity injections of the European Central Bank and the Federal Reserve, stock prices have continued to rise, but the real economy continues to contract. The separation between financial markets and the real economy is widening, and shorting stocks based solely on the recession outlook may involve significant policy risks. For the US dollar, euro, and pound sterling, financial stability is a crucial factor for achieving a soft landing for the economy. If asset prices fall sharply, the banking system may collapse. This is something that no monetary authority can afford, and it is difficult for the capital market to fall sharply again. Although a recession lies ahead, asset prices may find it difficult to rise, and the room for price declines is also limited.

The proportion of recession trades in the global commodity markets is increasing. Different from the past, in the context of geopolitical changes in the Middle East, OPEC+ and Russia have more say in oil pricing, and it is possible that the world economy will experience a recession while oil prices remain high. In that case, gold prices may not rise significantly, and the downward trend of the US dollar index should be a trend (interest rate hikes peak, maintaining a restrictive level influenced by the banking crisis).

In China, first and foremost, import and export data far exceeded expectations, especially export data. Looking at the detailed data, services and products related to the green economy were the main supporting factors. In the coming period, the development of the green economy is a major trend globally, so the factors supporting the improvement of exports are sustainable, even in the context of an external economic recession. Investment and consumption of green economy-related products remain at a high growth stage. Under such a broad context, external economic recession will not put pressure on China’s economy through exports. If export data continues to maintain high growth in the next 1-2 months, the capital market will need to revalue Chinese stocks.

Regarding the view on deflation, overall, affected by local governments tightening their belts and facing significant debt repayment pressure this year, the local government demand in the total demand of the economy has indeed contracted, but other demand is in the expansion phase. The weak CPI stage may continue for another 3-4 months.

1. Internationally, it is difficult for food prices to continue to rise against the backdrop of the easing Russia-Ukraine conflict. Although energy prices are high due to the increased market pricing power of OPEC+ and Russia, China has absolute control over energy prices with the rapid development of new energy sources. Therefore, the pressure of imported inflation is continuously decreasing, which is the international environment for China’s weakening prices.

2. After three years of the pandemic, China’s overall supply capacity has not been significantly impacted, and many large enterprises have not exited the market. Although some small and medium-sized enterprises have exited, the recovery speed of supply is fast. China’s total demand has indeed contracted, especially among residents. By February, the growth rate of retail sales was very low. The gap between total supply and total demand determines that the weak price trend will continue for some time.

3. China’s core CPI year-on-year fluctuation is around 1% and does not show a continuous contraction trend.

4. In terms of currency, affected by the previous increase in the household savings rate, M2 growth continues to rise. However, in terms of currency demand, social financing growth is weaker than M2, and a gap indeed exists between currency supply and demand. However, the data for March showed a turning point, with M2 growth declining and social financing growth increasing, narrowing the gap between currency supply and demand. This indicates that the supply of money in the economy is rising, further supporting property prices, stock prices, and CPI in the economy.

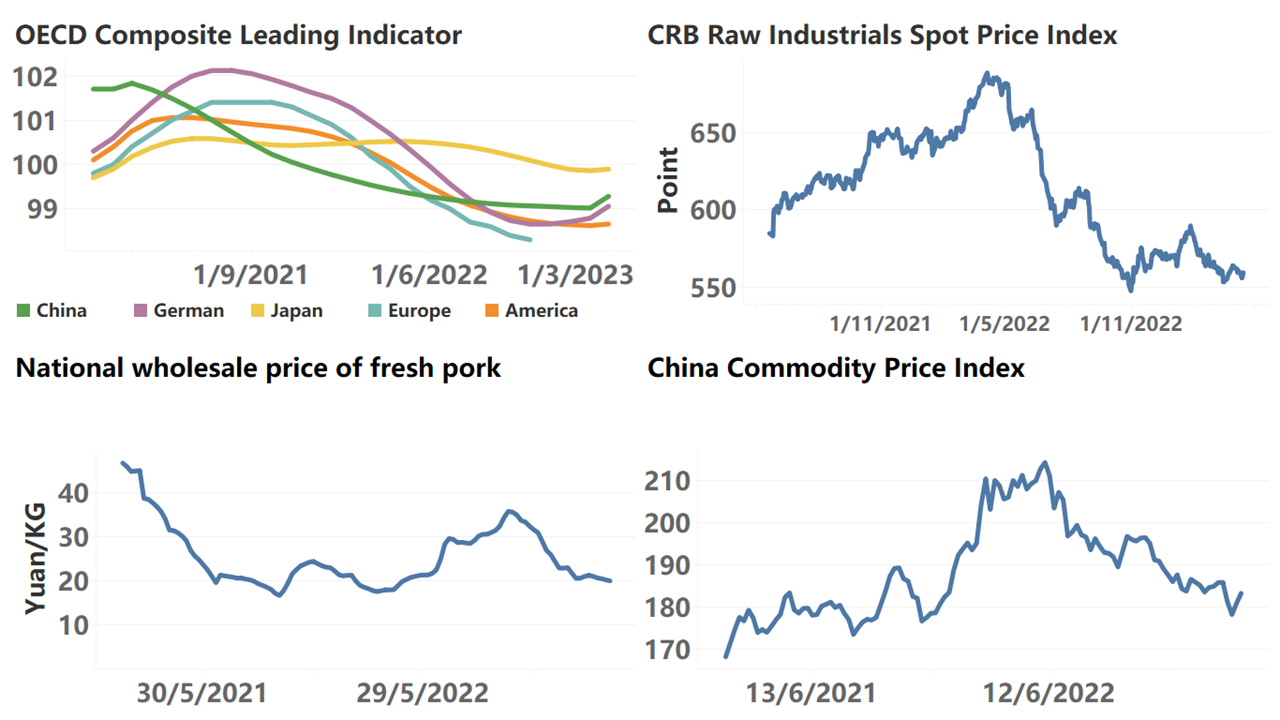

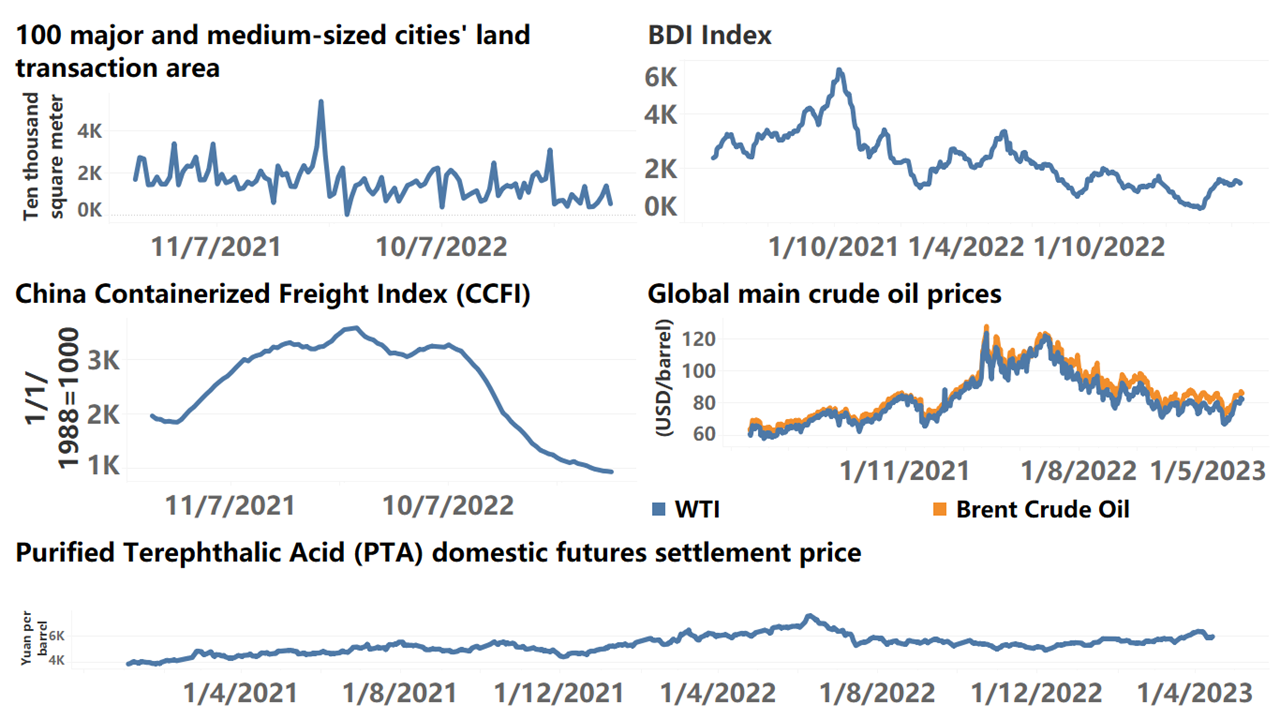

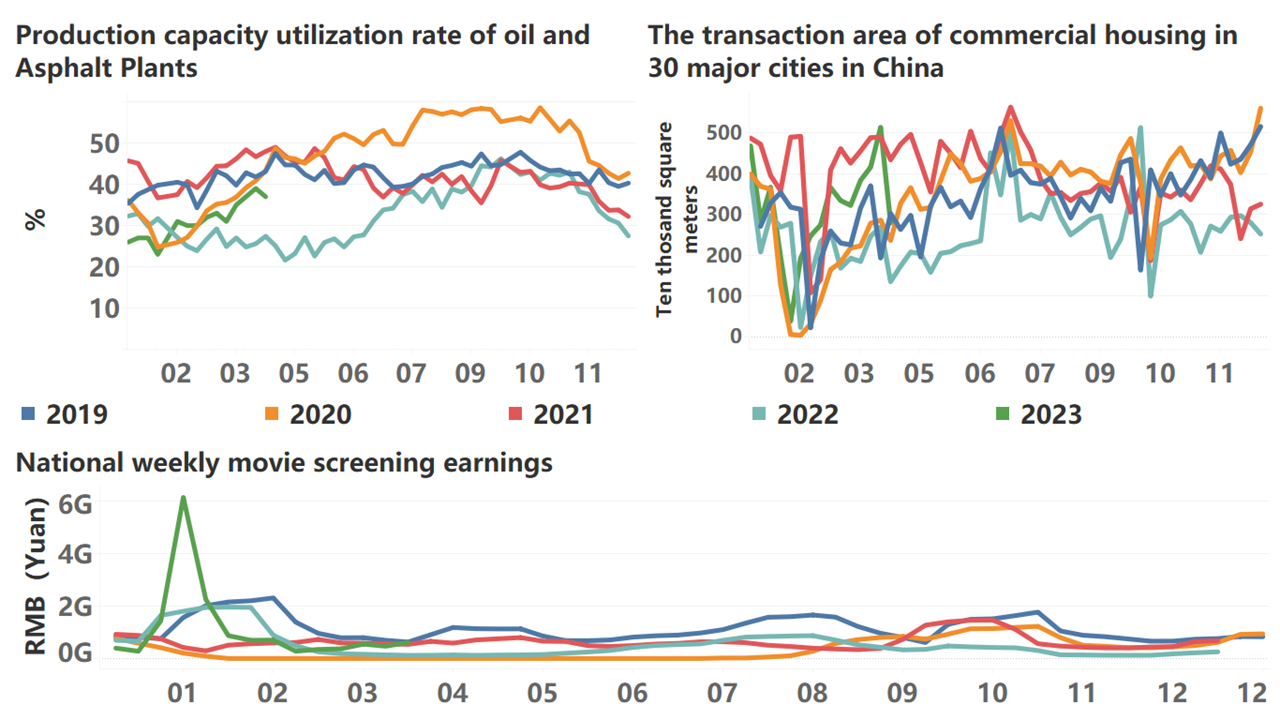

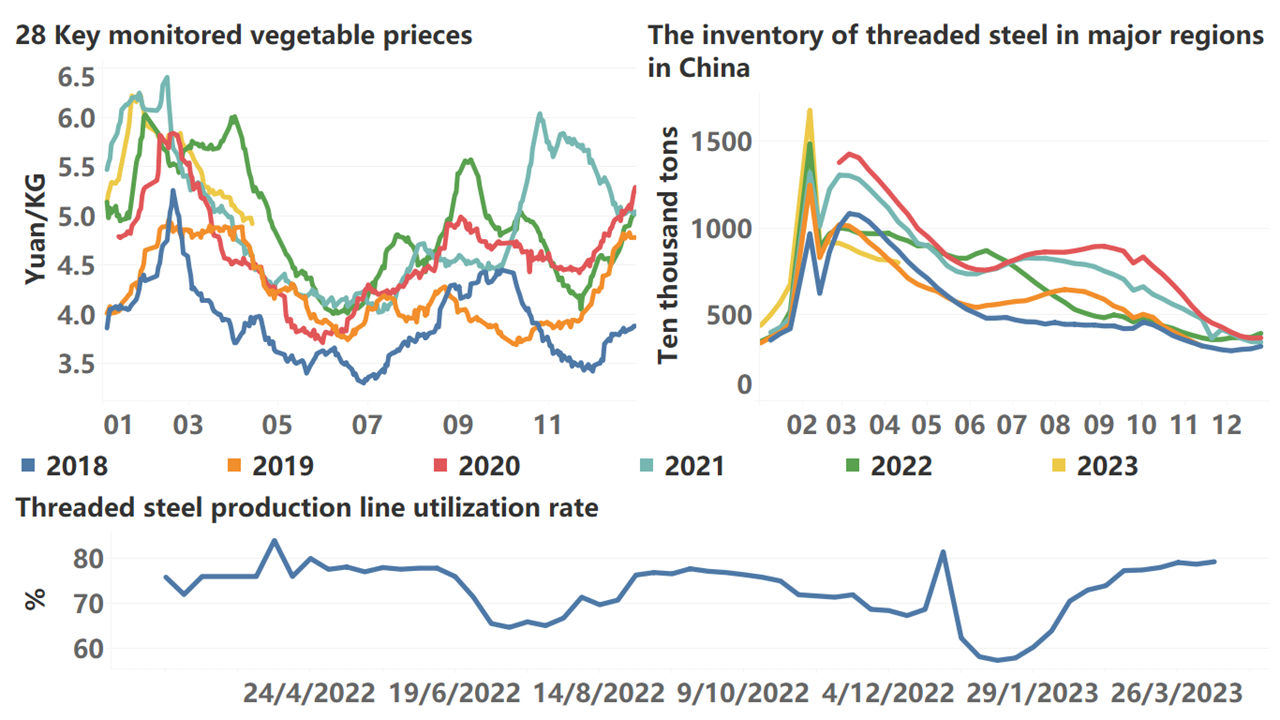

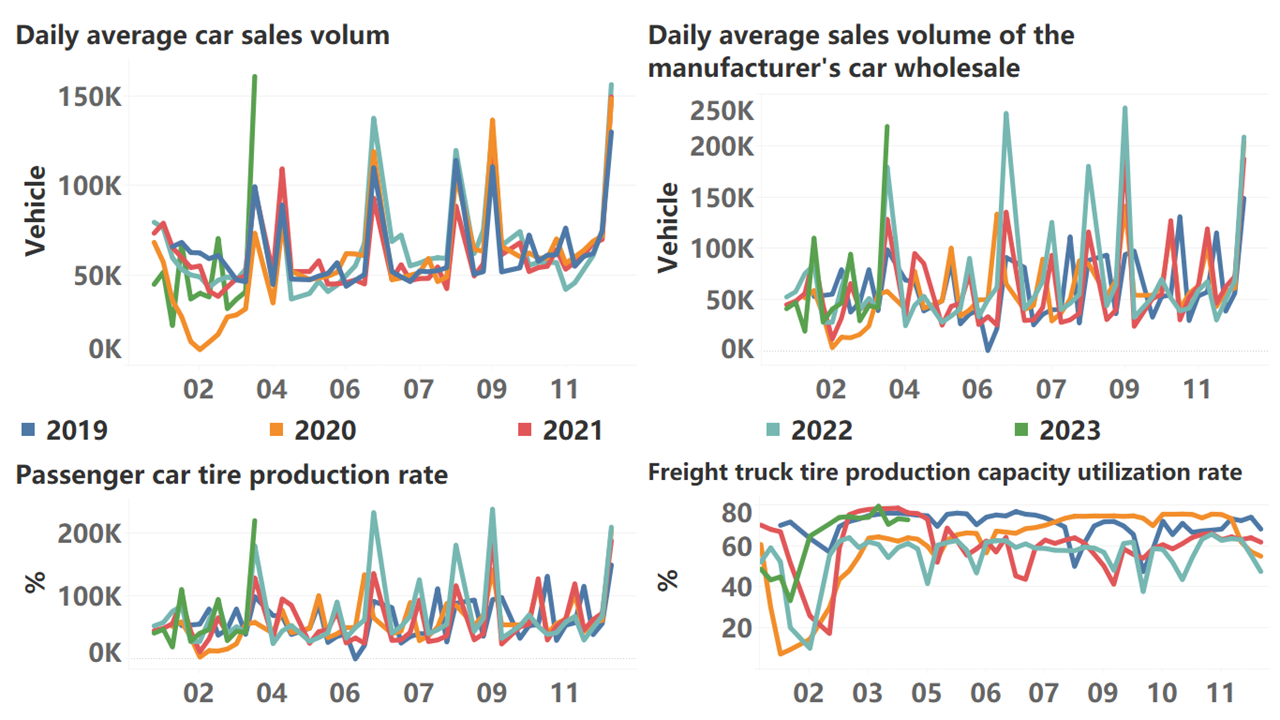

Below are the high-frequency data for this week:

*Translated by ChatGPT