This week, the US labor market slowed down, with data released by the US Department of Labor on Thursday showing that the number of first-time claims for unemployment benefits fell by 18,000 to 228,000 in the week ending April 1. The median estimate of economists surveyed by Bloomberg was 200,000. The previous week’s data was revised up by 48,000 to 246,000. Meanwhile, data released by the US Department of Labor on April 7 showed that nonfarm employment in the US increased by 236,000 in March, significantly lower than the 326,000 in February and the smallest increase since December 2020, slightly higher than the expected 230,000. The interest rate market inverted, with data from the Federal Reserve Bank of St. Louis showing that the 3-month US Treasury yield is now more than 150 basis points higher than the 10-year Treasury yield, the highest level of inversion since 1982. The US debt ceiling has yet to be raised, and due to China and Japan selling US Treasuries, the pressure on the US Treasury to issue new debt continues to grow. In the context of a soaring recession outlook, the probability of the Federal Reserve keeping interest rates unchanged in May is increasing, according to the CME.

In Europe, Germany and France are experiencing economic divergence. German CPI fell from 8.7% in February to 7.4% in March, and some institutions have raised their 2023 German economic growth forecasts by 0.7 percentage points. French CPI fell from 6.3% in February to 5.6% in March, and protests sparked by pension reform could cause a decline in French economic growth in 2023.

This week, the Chinese capital market has risen for four consecutive days, while the Asia-Pacific and European regions have experienced continuous fluctuations. The US stock market has shown mixed results, with the Dow Jones index rising and the Nasdaq index falling. Overall, the stock market is approaching previous high levels, and the risk of a downturn is gradually increasing. Whether the pressure at these high levels can be broken through depends on the development of the Federal Reserve’s monetary policy. For the Chinese market, whether it can achieve an independent trend remains to be seen, with artificial intelligence and consumption (automotive, real estate) being key drivers for breaking through capital market bottlenecks. Improving economic data for the second quarter is an important indicator for supporting overall expectations, and an accelerating global recession will become a bearish factor.

After OPEC member countries voluntarily cut production, Brent crude oil prices jumped from around $78 on March 31 to around $85 on April 8 (today), approaching previous high levels with limited upside potential. Due to changes in oil prices, global recession trades have picked up, and gold prices have risen from $1,998 per ounce on April 4 to $2,050 per ounce on April 8 (today), surpassing previous highs and approaching the March 2022 high of $2,078, reaching a five-year high. The US dollar index has fallen from around 102.6 to around 101.7. Gold prices are near their highs, and the US dollar index is approaching its previous lows, making this stage quite risky as the overall global economic outlook is stagflationary.

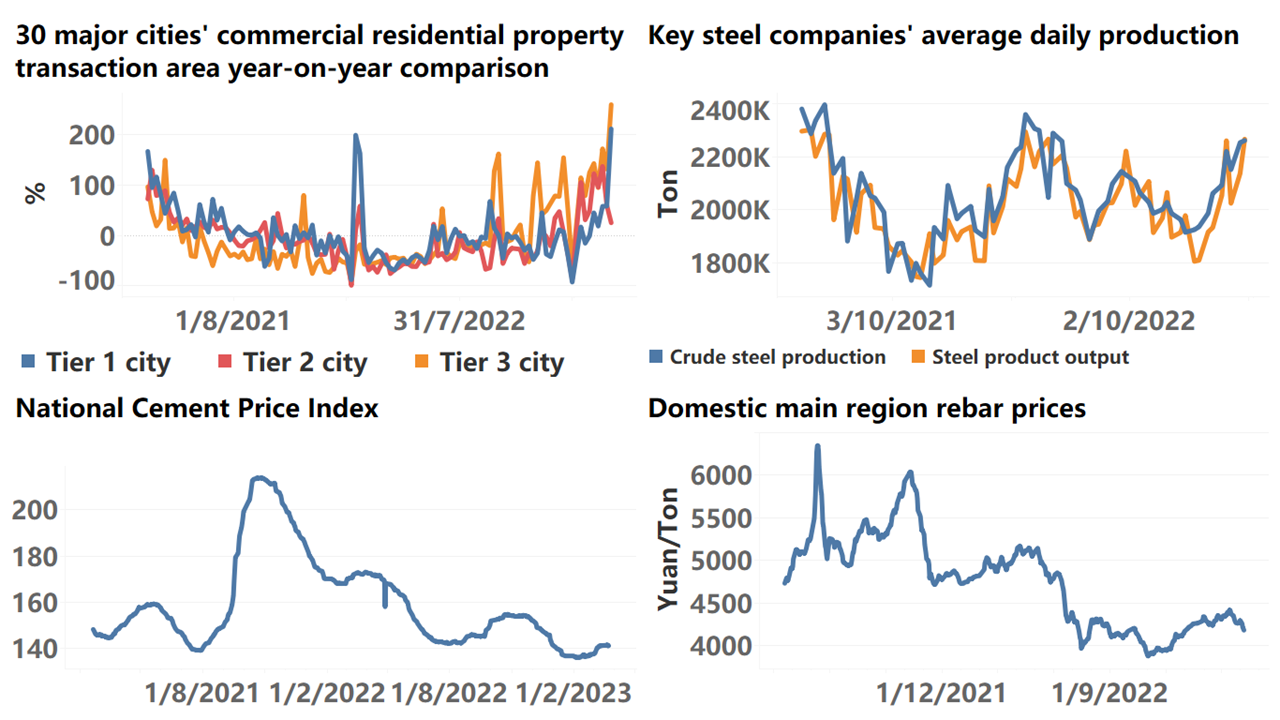

In the black market, rebar prices have fallen from 4,173 on March 31 to 3,996 on April 7, reaching previous lows. Coke prices have fallen from 2,751 on March 31 to 2,543 on April 7, well below previous lows.

The focus is on the impact of the US banking industry on capital markets. The Federal Reserve and the Treasury Department provide short-term loans to the banking system through liquidity measures. This helps reduce the pressure on banks to sell assets, thereby supporting the stock and bond markets. Additionally, these short-term loans flow back into the banking system through depositors, effectively serving as a short-term injection of base money, which is also favorable for asset prices. The recent rise in global capital markets, approaching previous highs, demonstrates that liquidity is indeed supporting asset prices. However, this raises two subsequent issues:

- How to address the impact of this excess liquidity on asset prices? When this extra liquidity is withdrawn upon maturity, it will influence asset prices along with interest rate information. However, while interest rate information is transparent, liquidity is not, making asset pricing more complex.

- The separation of the real economy from the capital markets. The real economy is constrained by high interest rates, while capital markets rise due to liquidity injections. This intensification of financial decoupling may exacerbate panic-induced pressure on the decline of financial asset prices later on.

In summary, the current economic and capital market situation is characterized by a slowing US labor market, concerns about an approaching recession, and fluctuations in various regional markets. The impact of monetary policy, especially liquidity measures, on asset prices and the separation between the real economy and capital markets are significant factors to watch for in the future.

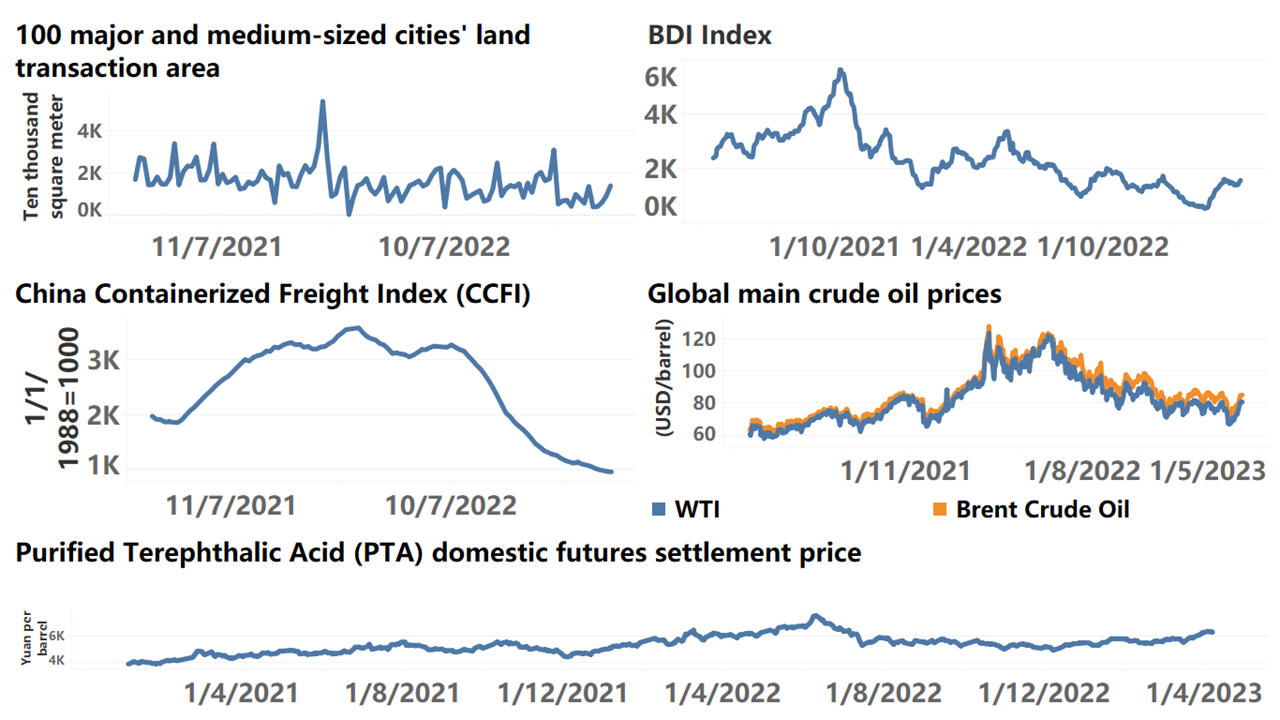

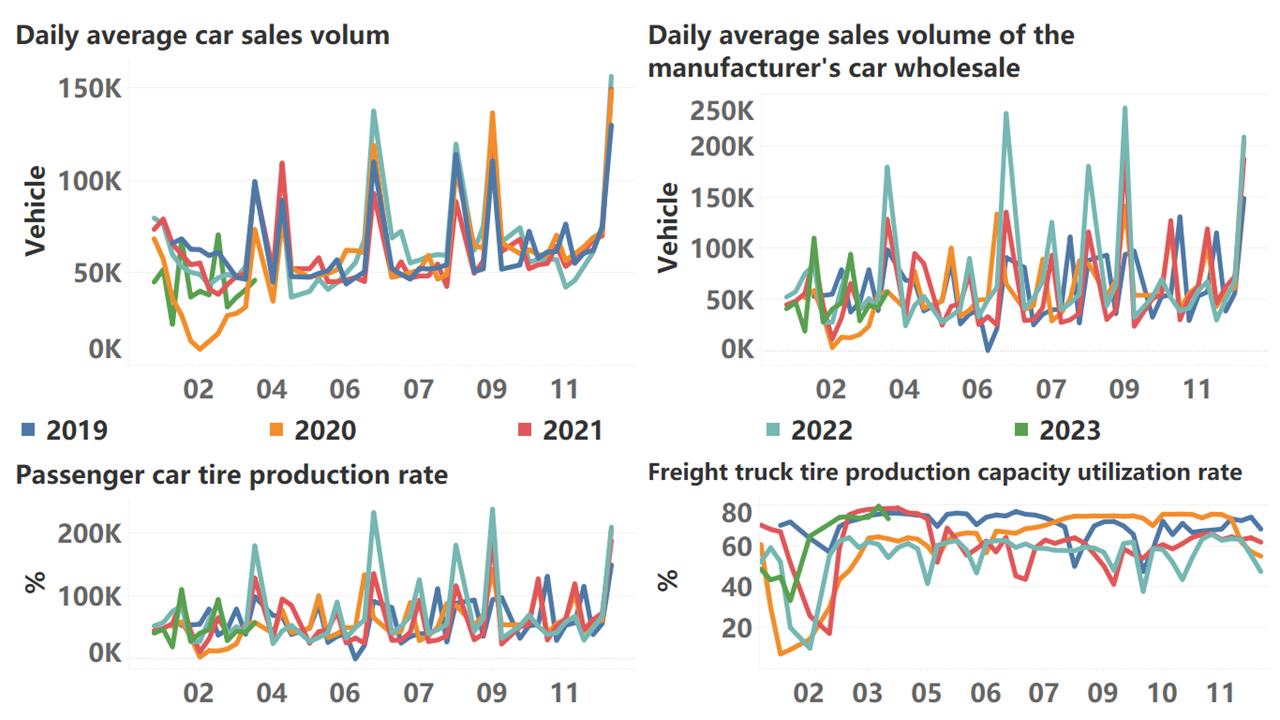

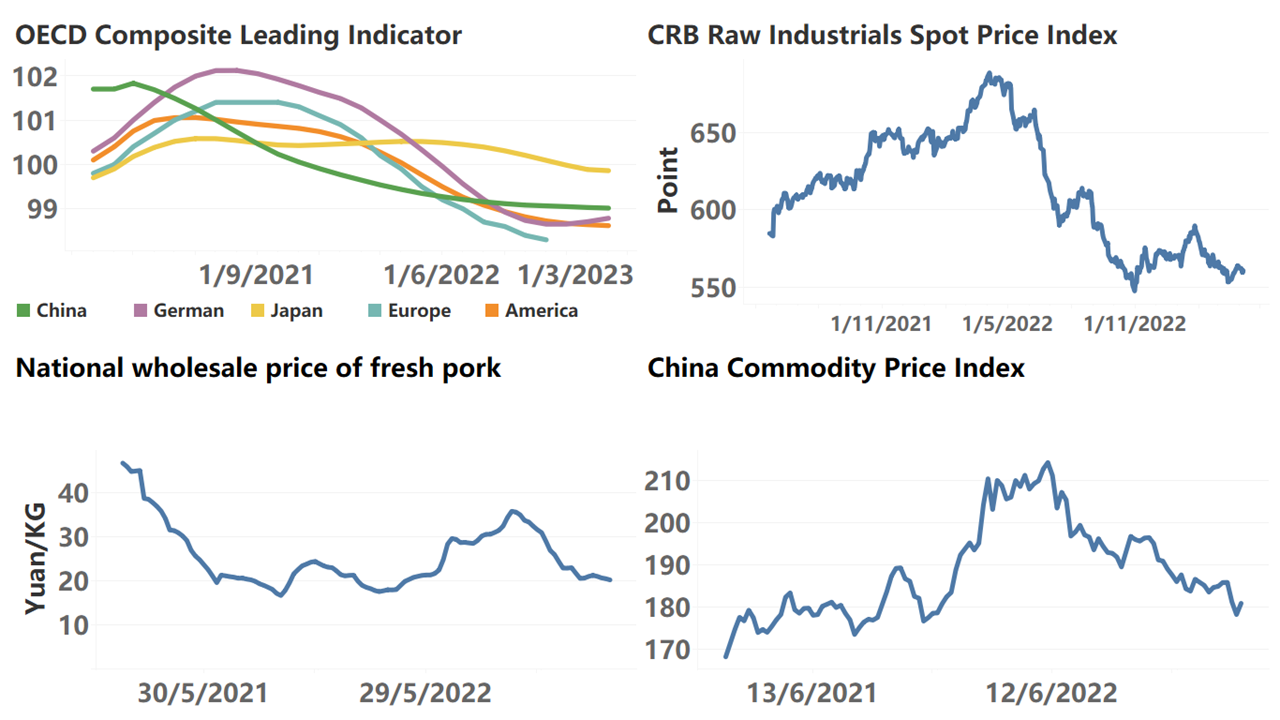

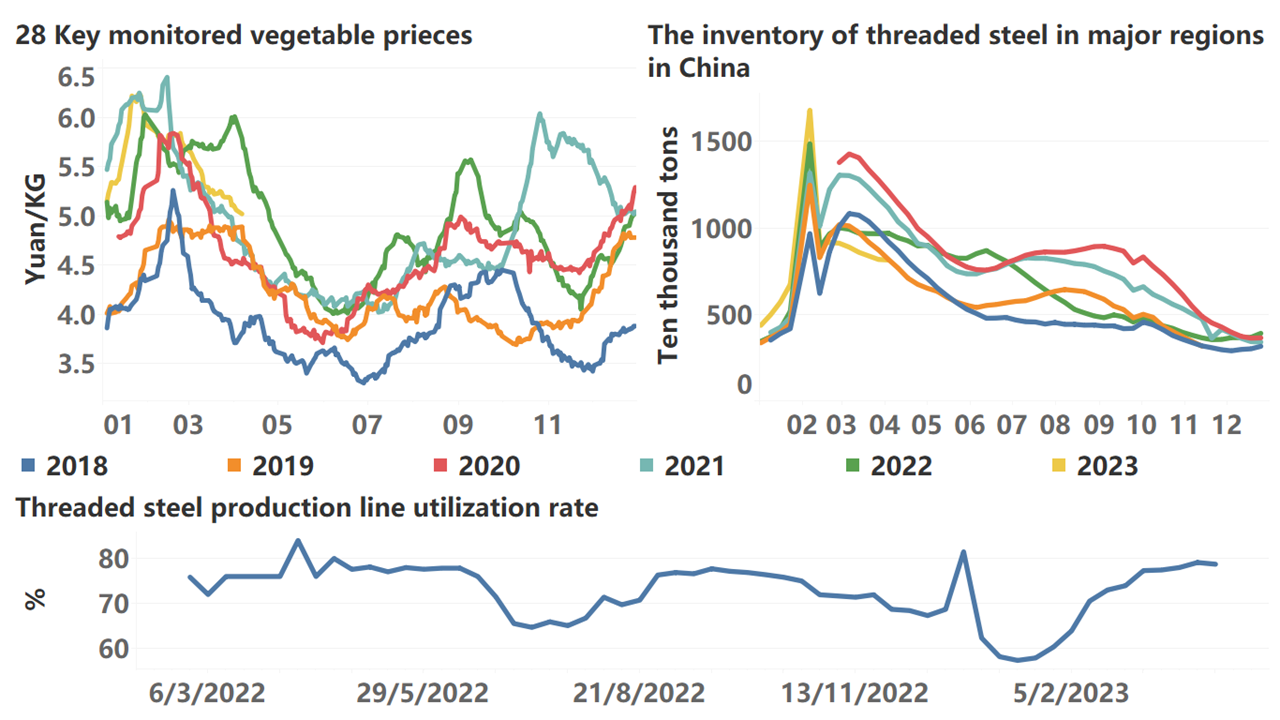

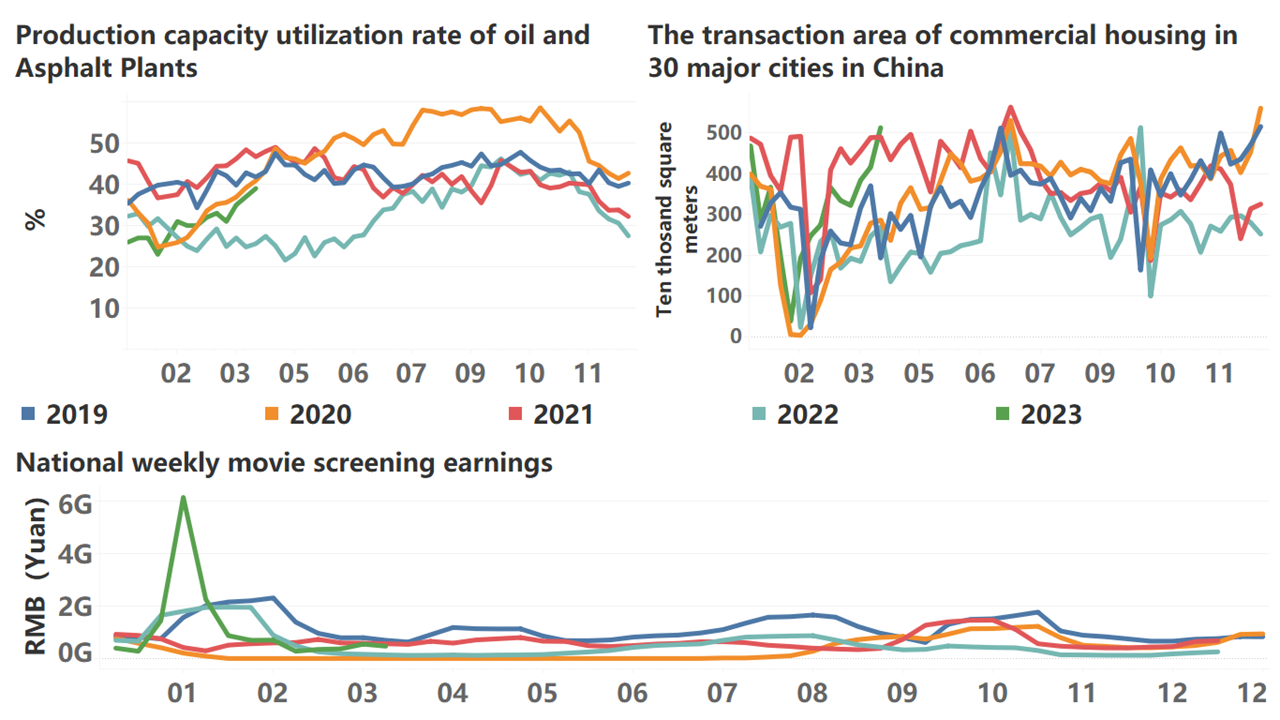

Below are the high-frequency data for this week:

*Translated by ChatGPT