This week, the stock market continued to rise, led by the TMT sector; gold prices also continued to rise, but the growth rate slowed down and basically reached its peak; oil prices remained stable, while steel and coal prices fell; driven by gold, the non-ferrous sector as a whole rose.

Fed rate hike and the attitude of the U.S. Treasury Department

On Wednesday, the Fed raised interest rates by 25 basis points as expected, causing significant fluctuations in the U.S. stock market. Powell said that he would continue to adhere to the inflation target, and then Yellen stated that the U.S. Treasury would not expand the cap on depositor protection. The next day, she said that additional measures would be taken, easing the mood in the U.S. stock market, which ultimately ended higher.

We believe that the essence of finance lies in credit, and the most important way to cure financial panic is to provide predictability for future prospects and to handle financial panic flexibly within the existing policy framework. At present, the unpredictability of the economic outlook mainly comes from two aspects: 1) when core service inflation will turn downward; 2) how high the interest rate peak can the banking industry withstand in terms of interest rate mismatch risk. To answer these two questions, Powell said at the press conference that due to the impact of rent, core service inflation has indeed shown greater resilience, but he also showed great confidence, believing that the long-term inflation expectation of 2% has not changed. At the same time, he expressed that the capital of the U.S. banking industry is very sufficient, and there is enough capital liquidity to cope with the bank run behavior of depositors. This is Powell’s way of enhancing the predictability of the economic outlook through information disclosure, and the credibility of this information disclosure method is supported by the Fed’s credit. However, debt problems are always underwater, and whether financial panic will exacerbate the bank run risk of banks is still something that investors need to pay attention to. The credibility of the Fed does not equal reality.

In addition, Powell reiterated the policy framework for the 2% inflation target. In such a monetary system framework, the interest rate dot plot shows that the interest rate peak is around 5.1%, which means that the interest rate peak has dropped, and there may be another 25 basis point rate hike within the year. This outlook basically takes into account both financial stability and the inflation target. Apart from interest rate tools, the Fed is likely to strengthen the provision of temporary liquidity to help banks through the period of restrictive interest rate levels. We can expect that the time for maintaining restrictive interest rate levels may be shortened, and the interest rate may decline in the fourth quarter.

Yellen’s two speeches on the banking industry are within the existing policy framework, seeking flexible responses to financial panic. Yellen’s ultimate view is to provide some additional tools to protect depositors’ savings, but without specifying what those tools are, reflecting the flexibility of policy and how to ensure the credibility of existing financial policies. By adopting this ambiguous approach, Yellen both appeases market sentiment and maintains a high-pressure stance on financial moral hazards.

European banking crisis still unresolved

UBS’s acquisition of Credit Suisse has severely disrupted the financial market’s order and caused significant damage to the credibility of the Eurozone financial market. In this event, the acquisition did not go through a shareholder meeting voting process, and it forcibly wrote off $17 billion in AT1 debt, challenging the institutional foundation of the financial market. It is unwise not to follow the existing policy framework and look for policy flexibility in the face of such a crisis. This sends a message to the outside world that Credit Suisse has severe potential liquidity risks, forcing it to break the basic order of the financial market. This potential information will spread to other areas of the Eurozone. Currently, UBS’s credit rating has been downgraded, and Deutsche Bank’s share price has been hit, reminiscent of the beginning of the Eurozone financial panic during the European debt crisis.

In a broader context, the U.S. and the Eurozone will maintain consistency in interest rate policies. If the Eurozone cannot withstand the market pressure brought about by financial panic and cuts interest rates ahead of time, the risk of stagflation in the U.S. economy will increase rapidly.

Sectors represented by TMT may undergo revaluation

On the domestic market side, as China is not in a tightening cycle, the interest rate mismatch risk in the banking industry does not have fundamental support in China. The risk we face is the sharp contraction of external demand.

This week, AI terminal products represented by large-scale artificial intelligence language models ignited the market’s enthusiasm for the sector. The TMT-centered sector will undergo revaluation.

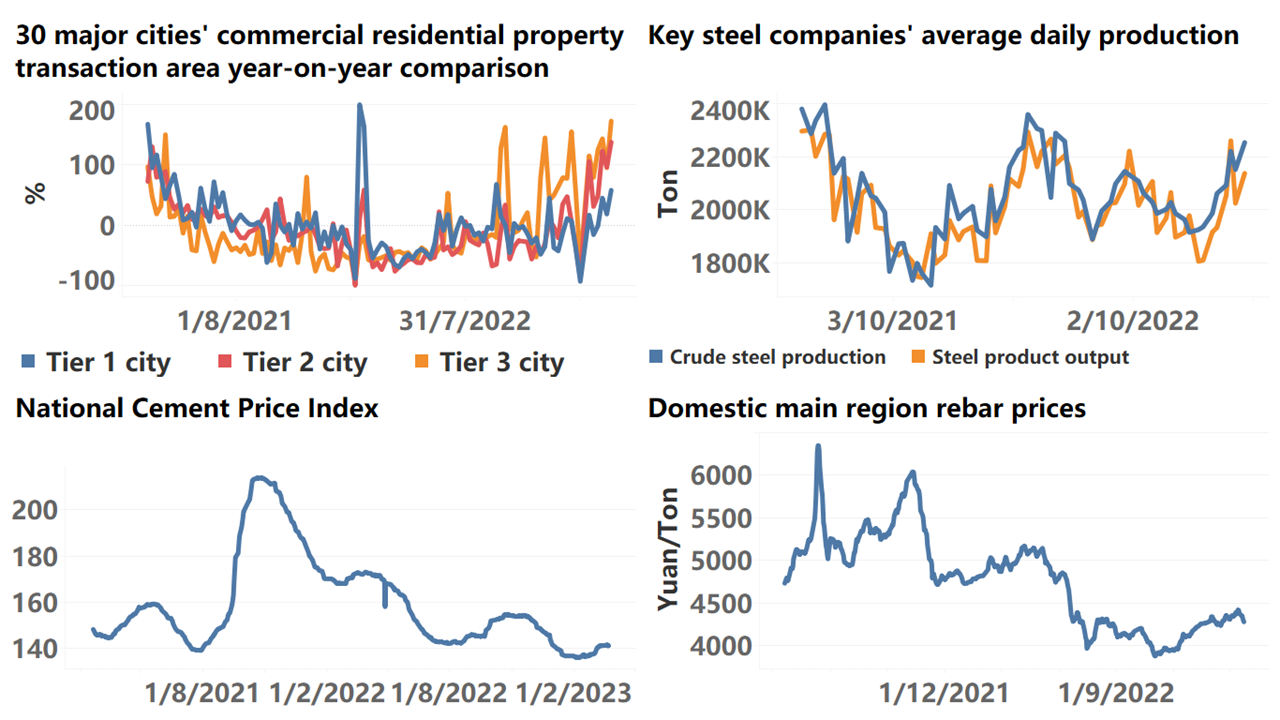

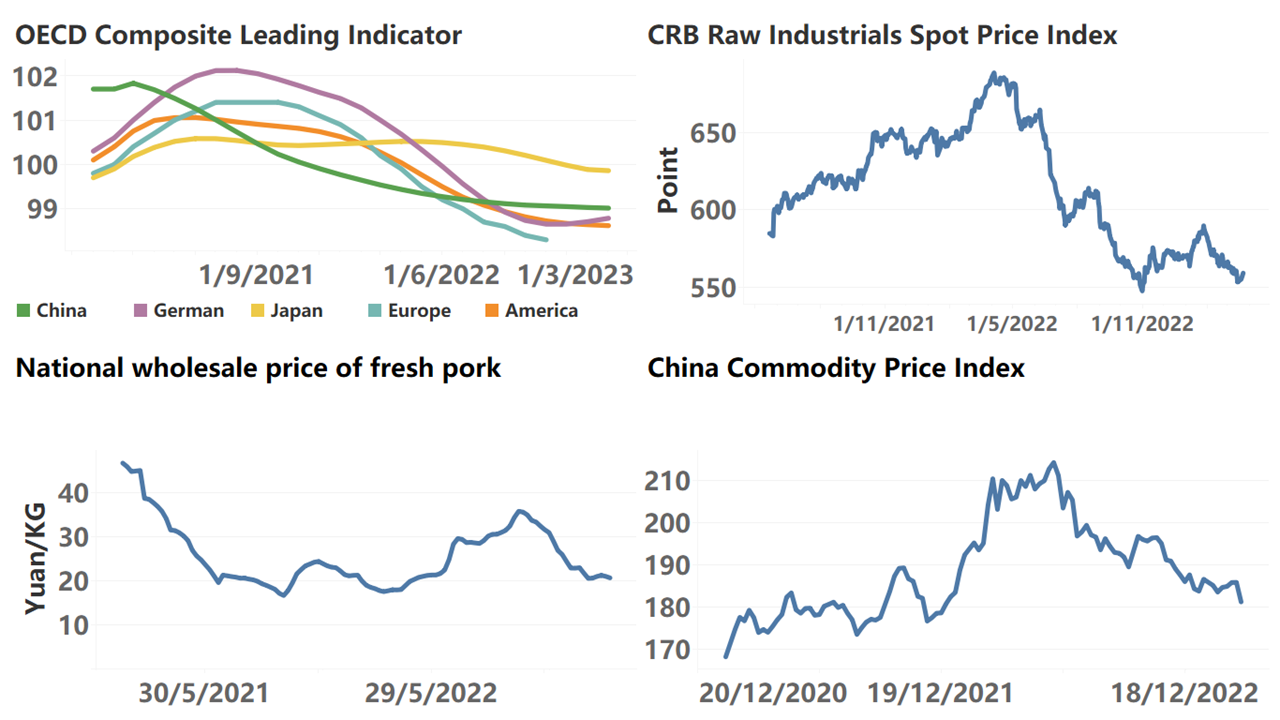

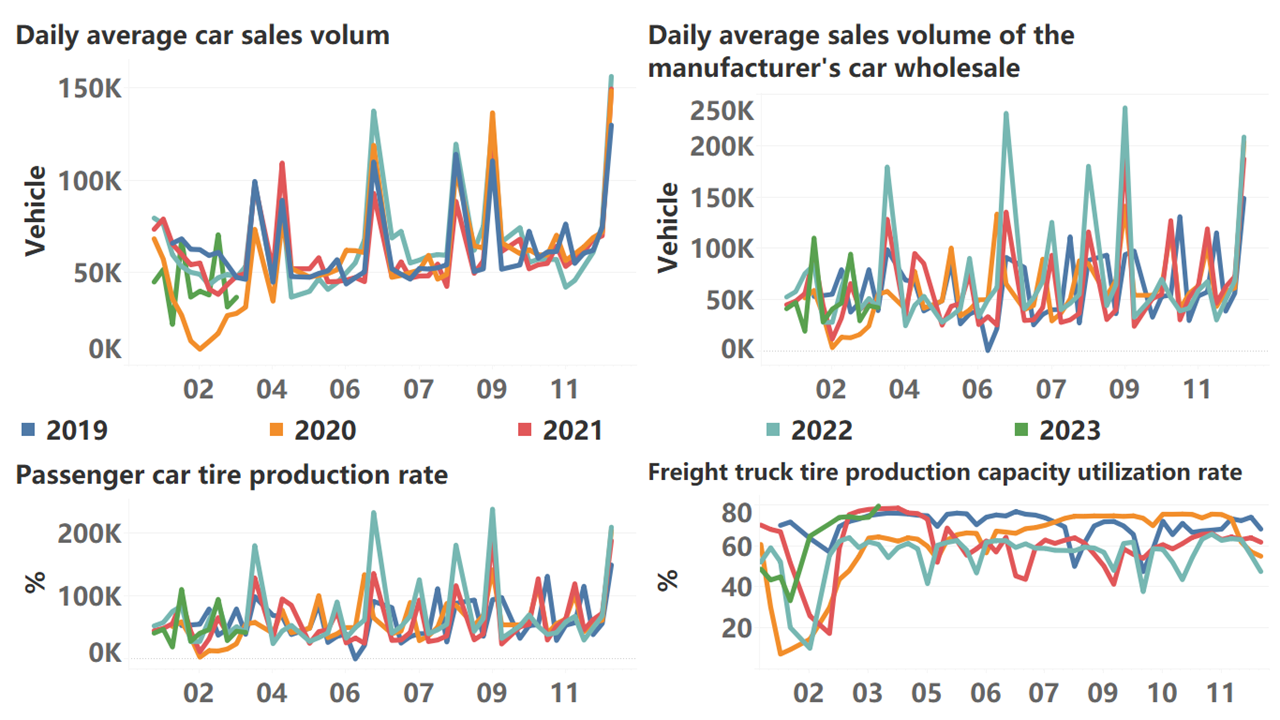

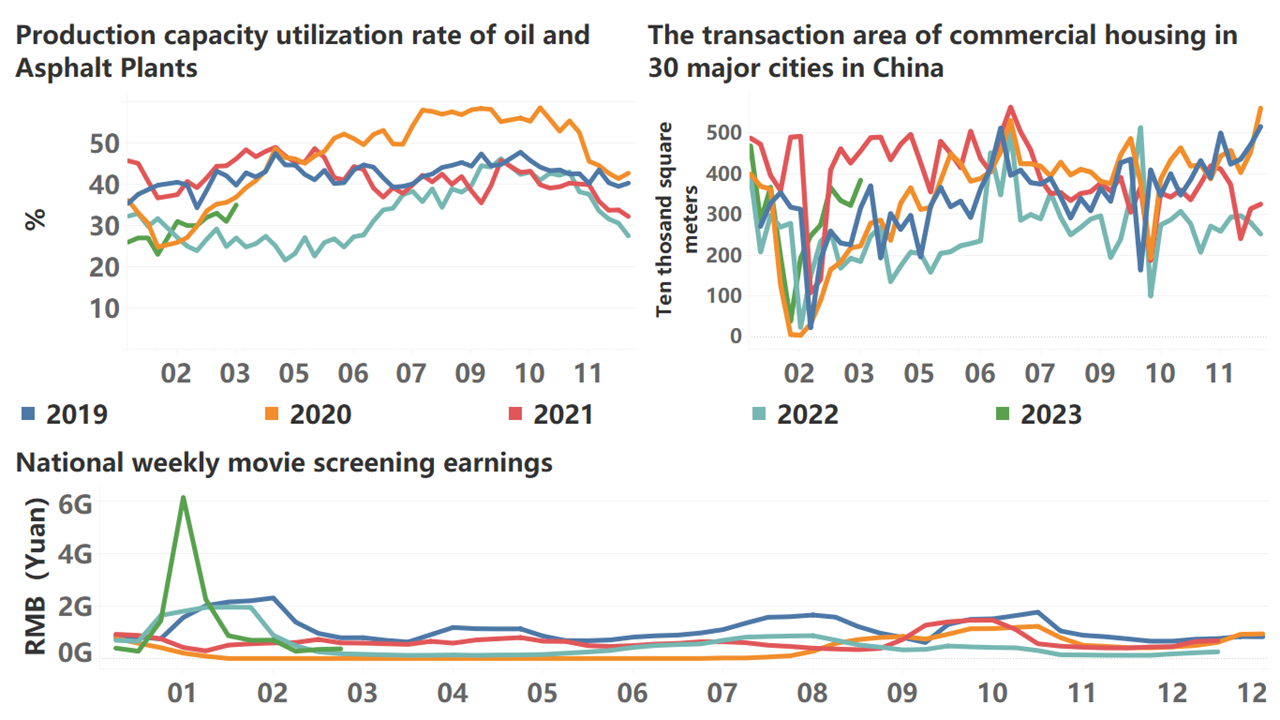

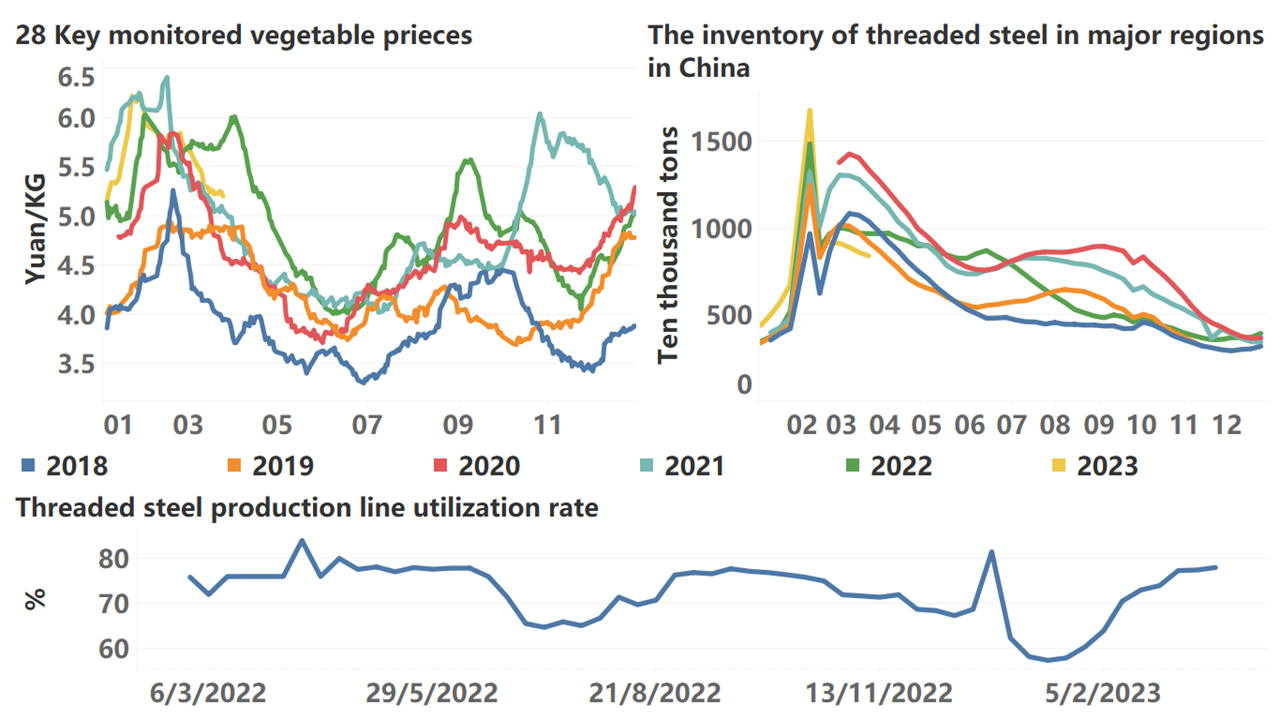

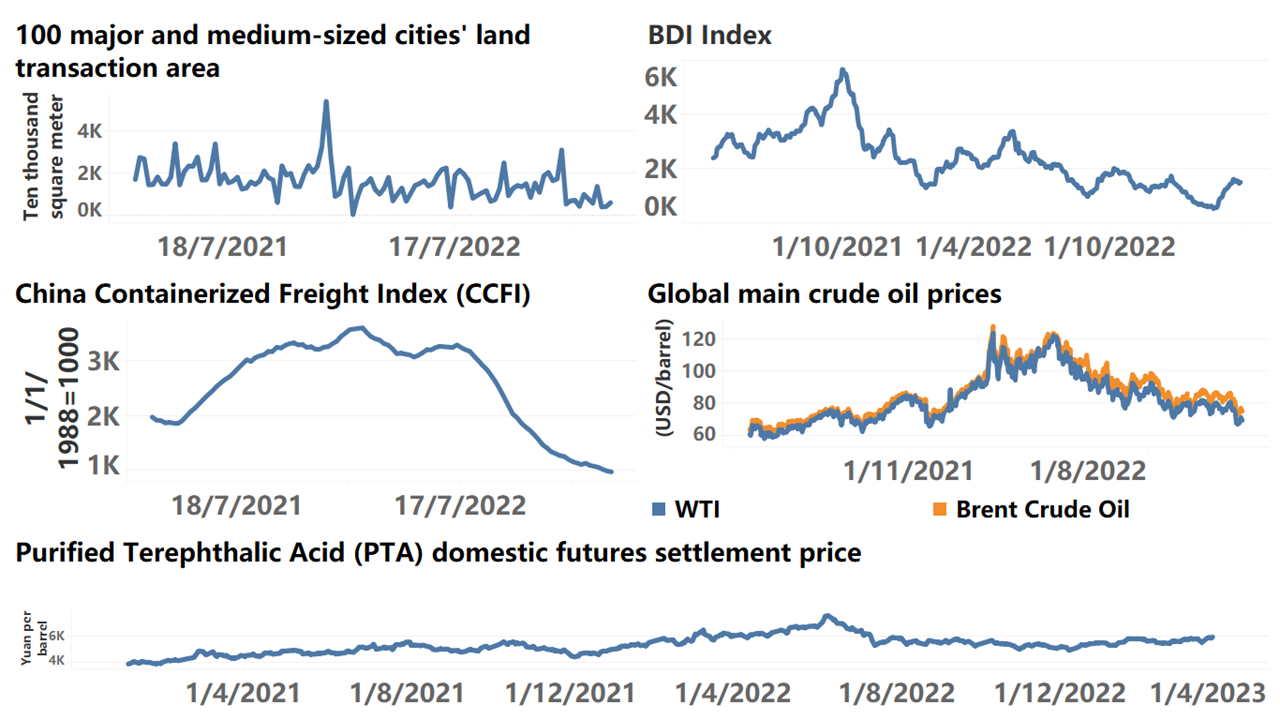

Below are the high-frequency data for this week: